An exchange-traded fund (ETF) is a type of fund that involves a collection of securities, and often tracks an underlying index

ETFs can invest in any number of industry sectors or use various strategies

ETFs trade on both the primary market and on the secondary markets

Primary Market: Creation and Redemption

ETF shares are created or redeemed in kind, in a shares-for-shares swap

ETF shares are created or redeemed on primary market

Authorized participants(APs) are the large brokers/dealers authorized by the ETF issuer to participate in the creation/redemption process

Creation or redemption happens directly between authorized participants(APs) and the ETF issuer on an over-the-counter basis

APs transfer securities to (for creations) or receive securities from(for redemptions) the issuer, in exchange for ETF shares

Creation basket is the list of securities specific to each ETF

Redemption basket is the basket of securities the AP receives when it redeems the ETF shares

Creation units is the size of transaction between the AP and the ETF manager, usually 50,O0O shares of the ETF

Secondary Market: Trading and Settlement

ETF shares trade intraday on exchanges

AP plays a role of either the broker or the market maker

Settlement

US settlement

Cleared and settled centrally

T+2 settlement

European settlement

Fragmented settlement process

Wider spreads and higher trading costs

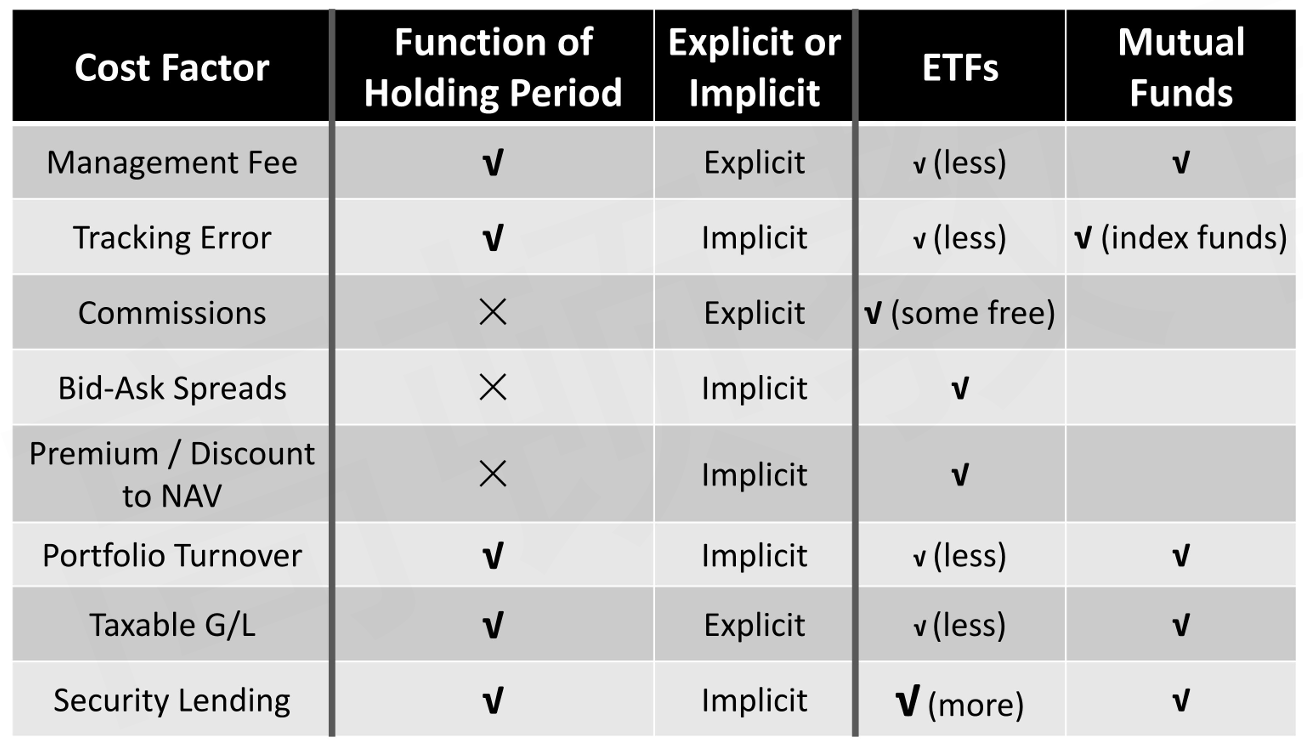

Costs and Risks of ETFs

Trading Costs

Bid-Ask Spreads

Bid-ask spreads represent the market maker's price to take the other side of the ETF transaction

Bid-ask spreads are determined by the following factors:

The market structure

Bid-ask spreads on fixed income relative to equity tend to be wider because the underlying bonds may trade in dealer markets and hedging is more difficult

Different time zones: Spreads on ETFs holding international stocks may be tighter when the underlying security markets are open for trading

Liquidity of the ETFs

More competition among market makers → lower spreads

Higher daily trading volume →lower spreads

Liquidity of the underlying securities

Generally, ETF bid-ask spreads are less than or equal to the combination of the following factors

Creation/redemption fees and other direct trading costs(+, may-)

Such as brokerage and exchange fees

Bid-ask spreads of the underlying securities held in ETFs(+)

Compensation to market maker or liquidity provider(+)

Market makers desired profit spread(+)

Subject to competitive forces

Discount related to receiving an offsetting ETF order (-)

Premiums and Discounts to NAV

ETF premiums and discounts refer to the difference between the exchange price of the ETF and the fund's calculated NAV

iNAV, or "indicated" NAV, are intraday "fair value" estimates of an ETF share based on its creation basket composition

An ETF is said to be trading at a premium when its share price is higher than iNAV or NAV, and at a discount if its price is lower than iNAV or NAV

End-of-day ETF premium or discount (%) = (ETF price - NAV per share) / NAV per share

Intraday ETF premium or discount (%) = (ETF price - iNAVper share) / iNAV per share

Premiums/discounts are driven by a number of factors

Timing differences: NAVs are based on underlying securities' last traded prices, which may be observed at a time lag to the ETFs' price

ETF and the underlying security trade on different exchanges

Some underlying securities trade in dealer market

Stable pricing

ETFs may be more liquid and more reflective of current information

Or, infrequently traded ETFs

Tracking Error

Index Tracking

For index-tracking ETFs,ETF managers attempt to deliver performance that tracks the fund's benchmark as closely as possible

Index-tracking ETFs dominate in the ETF markets

Index tracking is evaluated using the one-day or periodic difference in returns between the fund (as measured by its NAV) and its underlying index

Tracking Error

Tracking error is defined as the standard deviation of differences in performance between the index and the fund tracking the index

Tracking error does not reveal the extent to which the fund is under or over performing its index or anything about the distribution of errors

Sources of Tracking Error

Fees and expenses

Index calculation generally assumes that trading is frictionless and occurs at the closing price

A fund's operating fees and expenses reduce the fund's return relative to the index

Representative sampling and optimization

For funds tracking index exposure to small or illiquid markets,owning every index constituent can be difficult and costly

Depositary receipts and other ETFs

When local market shares are illiquid, ETF managers may choose to hold depositary receipts instead of local constituent shares

Although the economic exposure is equivalent, differences in trading hours and security prices create discrepancies between portfolio and index values, such as American depositary receipts (ADRs),global depositary receipts(GDRs)

Index changes

The more volatile the market, the wider the bid-offer spreads and range of traded prices

Fund accounting practices

Differences in valuation practices between the fund and its index can create discrepancies that magnify daily tracking differences

Regulatory and tax requirements

Asset manager operations Security lending or foreign dividend recapture income is not accounted for in the index calculation

Tax Issues

Tax Fairness

Mutual funds

When an investor sells, the fund must sell portfolio securities to raise cash to pay the investor

Any securities sold at a profit incur a capital gains charge, which is distributed to remaining shareholders

ETFs

An investor sells ETF shares to another investor in the secondary market do not require the fund to trade out of its underlying positions

If an AP redeems ETF shares, this redemption occurs in kind and is not a taxable event

Tax Efficiency

Tax lot management allows portfolio managers to limit the unrealized gains in a portfolio

When an authorized participant submits shares of an ETF for redemption, the ETF manager can choose which underlying share lots to deliver in the redemption basket

By choosing shares with the largest unrealized capital gains (those acquired at the lowest cost basis), ETF managers can use the in-kind redemption process to reduce potential capital gains in the fund

Other Distributions

Other events, such as security dividend distributions, can trigger tax liabilities for investors

In most markets,ETFs distribute their accumulated dividends

In some jurisdictions (eg. Europe), ETFs may have share classes that accumulate and automatically reinvest dividends into the fund

Other Costs and Risks Of Owning ETFS

Expense Ratios

ETFs generally charge lower fees than mutual funds

Do not have to keep track of individual investor accounts

Do not bear the costs of communicating directly with individual investors

Do not require the security and macroeconomic research carried out by active managers

The actual costs to manage an ETF vary

Portfolio complexity

Issuer size

Competitive landscape

Settlement risk

Some ETFs may use over-the-counter (OTC) derivatives, such as swaps, to gain market exposure has settlement risk

Security lending

ETF issuers lend their underlying securities to short sellers,earning additional income for the fund's investors

Securities lent are generally overcollateralized, so that the risk from counterparty default is low

Fund closures

Regulation/Competition /Corporate actions

Soft closures: Creation halts / Change in investment strategy

Investor related risk

Investors do not fully understand the underlying exposure

Leveraged and inverse ETFs

ETFs in Portfolio Management

Advantages

Portfolio liquidity management

ETFs can be used to invest excess cash balances quickly(known as cash equitization), thereby minimizing potential cash drag

Managers may also use ETFs to transact small cash flows originating from dividends, income, or shareholder activity

Transacting the ETF may incur lower trading costs and be easier operationally than liquidating underlying securities or requesting funds from an external manager

Portfolio rebalancing

Using liquid ETFs allows the portfolio remains fully invested according to its target weights

Portfolio completion strategies

If external managers are collectively underweighting or overweighting an industry or segment, ETFs can be used to adjust exposure up or down to the desired level

Transition management

Transition management refers to the process of hiring and firing managers, or making changes to allocations with existing managers,while trying to keep target allocations in place

Asset owners can use ETFs to maintain desired market or asset class exposure in the absence of having an external manager in place

Asset class exposure management

Core exposure to an asset class or sub-asset class

Tactical strategies

Active and factor investing

Factor(smart beta) ETFs

Risk management

Alternatively weighted ETFs

Discretionary active ETFs

Dynamic asset allocation and multi-asset strategies

Drawbacks

For very large asset owners, there are potential drawbacks to using ETFs for portfolio management

Given the asset owner size, they may be able to negotiate lower fees for a dedicated separately managed account(SMA) or find lower-cost commingled trust accounts that offer lower fees for large investors

An SMA can be customized to the investment goals and needs of the investor

Many regulators require large ETF holdings to be disclosed to the public

This can detract from the flexibility in managing the ETF position and increase the cost of shifting investment holdings

Multifactor Models

Arbitrage Pricing Theory

Arbitrage Pricing Model

APT introduced a framework that explains the expected return of a portfolio in equilibrium as a linear function of the risk of the portfolio with respect to a set of factors capturing systematic risk

E(R_P)=R_f+\sum\beta_{P,i}\lambda_i

\beta_{P,i} is the sensitivity of the portfolio to factor i

\lambda_i is the expected risk premium for risk factor i, also called factor risk premium

Pure Factor Portfolio

Pure factor portfolio is a portfolio with sensitivity of 1 to factor i and sensitivity of 0 to all other factors

\lambda_i from APT model is also the risk premium for a pure factor portfolio for factor i

Assumptions of APT

A factor model describes asset returns

There are many assets, so investors can form well-diversified portfolios that eliminate asset-specific risk

No arbitrage opportunities exist among well-diversified portfolios

The parameters of the APT equation are the risk-free rate and the factor risk-premiums

The factor sensitivities are specific to individual investments

APT model provides an expression for the expected return of asset assuming that financial markets are in equilibrium

APT model makes less assumptions than CAPM and does not identify the specific risk factors as well as the number of risk factors

CAPM can be regarded as a special case of APT model with only one risk factor (market risk factor)

Arbitrage Opportunity

An opportunity to conduct an arbitrage: earn an expected positive net profit without risk and with no net investment of money

If two portfolios with identical risk factors and factor sensitivities have different return, there is an arbitrage opportunity

Multifactor Models

Structure of Multifactor Models

Macroeconomic Factor Model R_i=E(R_i)+\beta_{i,1}F_1+\cdots+\beta_{i,k}F_k+\varepsilon_i

R_i is the return to asset i, and e(R_i) is the expected return to asset i

F_k is the surprise in in macroeconomic variables, like GDP, interest rate,inflation, credit spreads, etc.

Surprise is the difference between realized value and predicted value

\beta_{i,k} is the sensitivity of the return on asset i to a surprise in factor k

If we have adequately represented the sources of common risk (the factors),then ε; must represent an asset-specific risk

For a stock, it might represent the return from an unanticipated company-specific event

Fundamental Factor Model R_i=a_i+\beta_{i,1}F_1+\cdots+\beta_{i,k}F_k+\varepsilon_i

R_i is the return to asset i

F_k is the return associated with the factor k, which are asset attributes that are important in explaining cross-sectional differences in stock prices, like P/B ratio, P/E ratio, earning growth rate, etc.

\beta_{i,k} is the standardized beta of attributes k of the asset i

Statistical Factor Model

In a statistical factor model, statistical methods are applied to historical returns of a group of securities to extract factors that can explain the observed returns of securities in the group

Major weakness: In contrast to macroeconomic models and fundamental models, factors from statistical factor models are difficult to interpret economically

Major advantage: Statistical factor models make minimal assumptions

Two major types of statistical factor models are factor analysis models and principal components models

In factor analysis models, the factors are the portfolios of securities that best explain (reproduce) historical return covariances

In principal components models, the factors are portfolios of securities that best explain (reproduce) the historical return variances

Comparison between Models

Interpretation of intercept term

Macroeconomic factor model: the asset's expected return based on market expectations(e. g.APT)

Fundamental factor model: regression intercept

Interpretation of factors

Macroeconomic factor model: surprises in the macroeconomic variables

Fundamental factor model: return associated with asset attributes

Return from factor tilts is earned by taking different factor exposures compared to the benchmark, by overweight or underweight relative to the benchmark factor sensitivities

Security Selection Return

Return form security selection is earned by allocating different weights to securities compared to the benchmark

It reflects the ability to overweight securities that outperform the benchmark or underweight securities that underperform the benchmark

Risk Attribution

Active risk is the standard deviation of active returns

The active risk of a portfolio can be separated to two parts

Active risk squared = Active factor risk + Active specific risk

Active factor risk is the contribution to active risk squared resulting from the portfolios different than benchmark exposures relative to factors specified in the risk model

Active specific risk or security selection risk is the contribution to active risk squared resulting from the portfolios active weights on individual assets as those weights interact with assets' residual risk

Portfolio Construction and Decisions

Portfolio Construction

Multifactor models permit the portfolio manager to make focused bets or to control portfolio risk relative to the benchmark's risk

In evaluating portfolios, analysts use multifactor models to understand the sources of managers' returns and assess the risks assumed relative to the manager's benchmark

Passive management: Analysts can use multifactor models to match an index fund's factor exposures to the factor exposures of the index tracked

Active management: Analysts can use multifactor models in predicting excess risk adjusted return or relative return (the return on one asset or asset class relative to that of another) as part of a variety of active investment strategies

Strategic Portfolio Decisions

By introducing more risk factors, multifactor models enable investor gain from taking more or less exposures to risks that they have a comparative advantage / disadvantage

By considering multiple sources of systematic risk, multifactor models allow investors to achieve better diversified and possibly more efficient portfolios

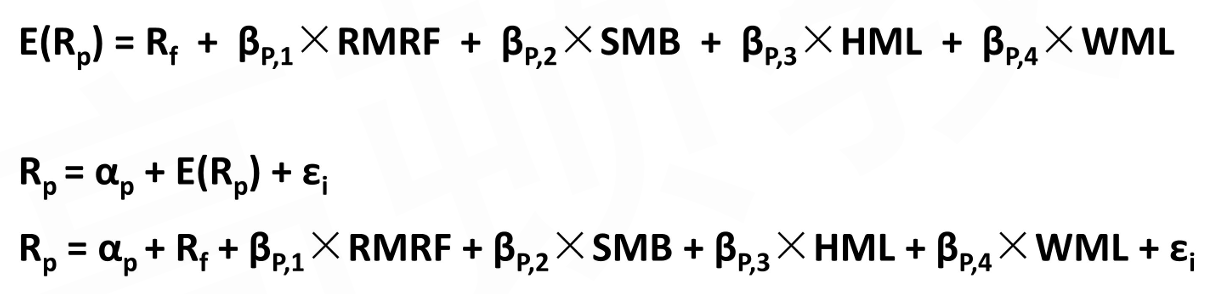

Carhart Model

The Carhart four-factor model can be viewed as an extension of CAPM,and also is an extension of the three-factor model developed by Fama and French

R_P and R_f are the return on the portfolio and the risk-free rate of return, respectively

\alpha_P is the return in excess of that expected given the portfolio's level of systematic risk (assuming the four factors capture all systematic risk)

\beta_P is the sensitivity of the portfolio to the given factor

\varepsilon_i is an error term that represents the portion of the return to the portfolio not explained by the model

RMRF is the return on a value-weighted equity index in excess of the one-monthT-bill rate

SMB represents "small minus big", a size factor,is the average return on small-cap portfolios minus the average return on large-cap portfolios

HML represents "high minus low", a value factor,is the average return on high book-to-market portfolios minus the average return on low book-to-market portfolios

WML represents "winners minus losers", a momentum factor,is the return on a portfolio of the prior winners minus the return on a portfolio of the prior losers

Measuring and Managing Market Risk

Value at Risk

Definition of VaR

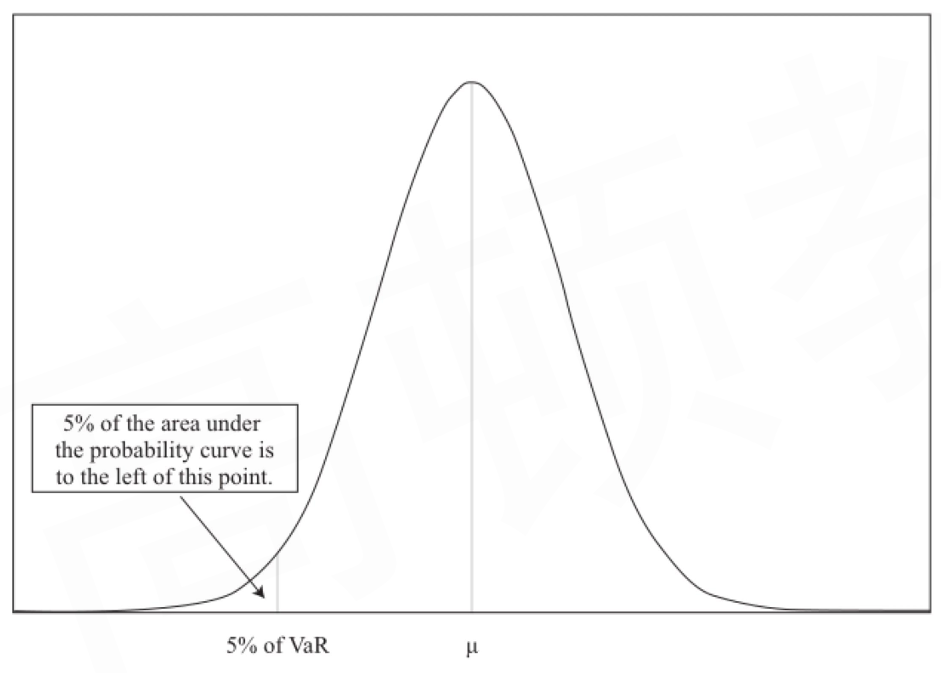

Value at risk is an estimate of the maximum (or minimum) expected loss at a specified level of probability over a specified time period

It associated with a given probability

It has a time element and cannot be compared directly unless they share the same time interval

VaR is usually expressed either as a percentage(% VaR) or in units of currency($ VaR)

In practical, it is more common to state VaR using a confidence level

A 1% VaR would be expected to show greater risk than a 5% VaR

The VaR time period should relate to the nature of the situation

A traditional stock and bond portfolio would likely focus on a longer monthly or quarterly VaR, while a highly leveraged derivatives portfolio might focus on a shorter daily VaR

The left-tail should be examined

The left side of a traditional probability distribution displays the low or negative returns, which is what VaR measures at some probability

Methods to Estimate VaR

Parametric Method

Assume that asset returns conform to a normal distribution

VaR for a portfolio, which contains asset A and asset B(E(R_A)=E(R_B)=0)

\begin{align}

&VaR_{\%}=\sqrt{w_A^2VaR_{A,\%}^2+w_B^2VaR_{B,\%}^2+2\rho_{A,B}w_Aw_BVaR_{A,\%}VaR_{B,\%}}

\\

&VaR_{\$}=\sqrt{VaR_{A,\$}^2+VaR_{B,\$}^2+2\rho_{A,B}VaR_{A,\$}VaR_{B,\$}}

\end{align}

Square Root Rule(E(R)=0) VaR_{\text{T day}}=VaR_{\text{1 day}}\times\sqrt T

Advantage

Simple and straightforward

Disadvantage

Its estimates will only be as good as the estimate of the parameter (mean, variance, covariance)

The usefulness is limited when normality assumption is not reasonable

E.g. when the investment portfolio contains options

Many assets exhibit leptokurtosis

Historical Simulation Method

Given the historical returns and sort the results from largest loss to greatest gain, find out VaR

Imagine that the returns from a portfolio over the past 300 days have been computed and ranked in order from best to worst

We can say that on only 5% of the days was the return worse than or equal to the return placed in the 286th position

Hence the one-day VAR estimate will be the return placed 286th in the list (multiplied by the current portfolio value, if we want the absolute $ VaR)

Advantage

No normality or any other distribution assumption

Available to estimate the VaR for portfolio with options Based on what actually happened, so it cannot be dismissed as introducing impossible outcomes

Based on what actually happened, so it cannot be dismissed as introducing impossible outcomes

Disadvantage

No certainty that a historical event will re-occur, or that it would occur in the same manner or with the same likelihood as represented by the historical data

If data in the lookback period is more volatile, VaR will be over-estimate

If data in the lookback period is less volatile, VaR will be under-estimate

Both parametric and historical simulation methods has a shortage that all observations are weighted equally

Improvement: giving more weight to more recent observations and less weight to more distant observations

Monte Carlo Simulation Method

The user develops his own assumptions about the statistical characteristics of the distribution and uses those characteristics to generate random outcomes that represent hypothetical returns to a portfolio

A computer program simulates the changes in value of the portfolio through time and run repeatedly to produce a set of possible end-of-horizon values

This modelled distribution of portfolio values can then be used to estimate the VaR

Advantage

It can accommodate virtually any distribution

It can accurately incorporating the effects of option positions or bond positions with embedded options

More flexible than the other two methodologies

Disadvantage

Assumptions of inputs are critical for accuracy of estimates

Complex: great deal of computer time and calculations

Extensions of VaR

Advantages of VaR

Simple concept

Easily communicated concept

Provides a basis for risk comparison

Facilitates capital allocation decisions

Can be used for performance evaluation

Reliability can be verified

Widely accepted by regulators

Disadvantages of VaR

It dose not tell us what happened below the VaR and may underestimate the frequency of extreme events

Subjectivity that various methods can generate different values

Oversimplification that it is a single measure that gives limited information

Accuracy of VaR can only be determined after the fact (back testing)

It can underestimate size and frequency of the worst losses if assumptions and models are incorrect

Sensitivity to correlation risk

VaR for individual positions does not easily sum up to a portfolio VaR

Disregard of right-tail events

Failure to take into account liquidity

Misunderstanding the meaning of VaR

Vulnerability to trending or volatility regimes

Conditional VaR(CVaR)

The average loss that would be incurred if the VaR cutoff is exceeded

Also named "expected tail loss"or "expected shortfall"

Incremental VaR(IVaR)

The difference in VaR between the "before" and "after" VaR if a position size is changed relative to the remaining positions

Marginal VaR(MVaR)

The change in VaR for a small change in a given portfolio holding

MVaR is the slope of VaR-weight curve for a security in the portfolio

Approximately, MVaR is the change in VaR for a $1 or 1% change in the position for a security in the portfolio

Relative VaR

A measure of the degree to which the performance of a given investment portfolio might deviate from its benchmark

Also named ex ante tracking error

Other Risk Measures

Sensitivity Risk Measures

Examine how portfolio value responds to a small change in a single risk factor

Equity exposure measures: Beta

Fixed-income exposure measures: duration and convexity

Options risk measures: Delta, Gamma, Vega, etc.

Advantages

Sensitivity risk measures can inform a portfolio manager about a portfolio's exposure to various risk factors to facilitate risk management

If too much/less risk exposure to a risk factor, the manager can modify the exposure accordingly

Limitations

Sensitivity risk measures can only be used to estimate the effects of small changes in risk factors

Even combination of first-order and second-order effects only provide approximation for large changes in risk factors

Two portfolios with same sensitivity risk measures can have different risk due to different volatility of risk factors

Two fixed income portfolios with same duration but different yield volatilities.

Scenario Risk Measures

Hypothetical scenario approach uses a set of hypothetical change in risk factors, not just those that have happened in the past

Stress tests examine the impact on portfolio of a scenario of extreme changes of risk factors

Stress tests can determine the size of change on a certain risk factor that could compromise the sustainability of the investment

Scenario analysis can be regarded as the final step in the risk management process, after performing sensitivity analysis

Scenario analysis can provide additional information on a portfolio's vulnerability to changes of risk factors or the correlations between risk factors.

Advantages

Scenario risk measures can focus on extreme outcomes, but not bound by either recent historical events or assumptions about parameters or probability distributions

Allowing liquidity to be taken into consideration

Scenario analysis is an open-ended exercise that could look at positive or negative events, although its most common application is to assess the negative outcomes

Stress tests intentionally focus on extreme negative events

Limitations

Sensitivity risk measures can only be used to estimate the effects of small changes in risk factors

Even combination of first-order and second-order effects only provide approximation for large changes in risk factors

Two portfolios with same sensitivity risk measures can have different risk due to different volatility of risk factors

Two fixed income portfolios with same duration but different yield volatilities.

Choices of Risk Measures

The choices of risk measures by an organization is mainly decided by

Types of risks it faces

Regulation that govern it

Whether it uses leverage

Banks

Banks need to balance a number of competing aspects of risk to manage their business and meet the expectations of equity investors/analysts,bond investors, credit rating agencies, depositors, and regulatory entities

The typical risk measures used by banks

Liquidity gap

Economic capital

VaR

Sensitivity measures

Scenario analysis and stress tests

Leverage risk measures

Asset Managers

Traditional asset managers focus on relative risk measures

The typical risk measures used by traditional asset managers

Position limits

Sensitivity measures

Scenario analysis

Active share

VaR

Liquidity

Redemption risk

Tracking error VaR

Hedge funds managers focus on absolute return

The typical risk measures used by hedge asset managers

Sensitivity measures

Leverage

VaR

Scenario analysis

Drawdown

Pension Funds

The risk management goal for defined benefit pension funds is to be sufficiently funded to make future payments to pensioners

The typical risk measures used by pension funds

Sensitivity measures

Surplus at risk

Interest rate and curve risk

Insurers

The typical risk measures used by property and casualty insurers

sensitivities and exposures

Economic capital

VaR

Scenario analysis

The typical risk measures used by life Insurers

Sensitivities

asset and liability matching

scenario analysis

Managing Market Risk

Risk budgeting: determining the overall risk appetite, and then allocated to sub-activities or business units

Capital allocation is the practice of placing limits on each of a company's activities in order to ensure that the areas in which it expects the greatest reward and has the greatest expertise are given the resources needed to accomplish their goals

Risk measures must be introduced when limit the overall risk and allocate risk across the activities or business units by risk budgeting

Position limits

The maximum currency amount or percentage of portfolio value allowed for specific asset or asset class

Scenario limits

Limits on expected loss for a given scenario

Stop-loss limits

Require an investment position to be reduced or closed out when losses exceed a given amount over a specified time period

Backtesting and Simulation

Objectives and Steps in Backtesting an Investment Strategy

Backtesting approximates the real-life investment process by using historical data to assess whether a strategy would have produced desirable results

Backtesting can be employed as a rejection or acceptance criterion for a strategy

Steps in backtesting an investment strategy

Strategy design

Specify investment hypothesis and goal(s)

Determine investment rules, process and key parameters

Historicalinvestment simulation

Form and rebalance investment portfolios for each period according to the rules

Analysis of backtesting output

Calculate portfolio performance statistics

Reported Metrics and Visuals

Metrics

Average return

Volatility

Downside risk(e.g.VaR, CVaR, and maximum drawdown)

Sharpe ratio, Sortino ratio

Visuals

An intuitive way of summarizing many data points

Although backtesting fits quantitative and systematic investment styles more naturally, it has also been heavily used by fundamental managers

Problems in Backtesting an Investment Strategy

Survivorship bias refers to deriving conclusions from data that reflects only those entities that have survived to that date

Point-in-time data allows analysts to use the most complete data for any given prior time period

Look-ahead bias is created by using information that was unknown or unavailable during the historical periods over which the backtest is conducted

Survivorship bias is actually a type of look-ahead bias

Data snooping is a type of selection bias, and it occurs when an analyst selects data or performs analyses until a significant result is found

Otherwise known as "p-hacking"

Historical Scenario Analysis

Rather than simply acknowledging or even ignoring structural breaks evident in backtesting results, an analyst should pay careful attention to different structural regimes and impacts to a strategy during regime changes

Historical scenario analysis is a type of backtesting that explores the performance and risk of an investment strategy in different structural regimes and at structural breaks

Two common examples of regime changes are from economic expansions to recessions and from low-volatility to high-volatility environments

Historical Simulation

Historical simulation constructs results by selecting returns at random from many different historical periods without regard to time-ordering

Historical simulation assumes that past asset returns provide sufficient guidance about future asset returns

Historical simulation assumes the data are stationary

Sampling from the historical returns can be with replacement or without replacement

Sampling with replacement, also known as bootstrapping, is more common, because the number of simulations needed is often larger than the size of the historical dataset

Monte Carlo Simulation

Each key variable is assigned a statistical distribution, and observations are drawn at random from the distribution

The distribution should reasonably describe the key empirical patterns of the underlying data

The correlations between multiple key decision variables should be accounted for, and it is necessary to specify a multivariate distribution rather than modeling each factor or asset on a standalone basis

Flexible, but complex

Sensitivity Analysis

Sensitivity analysis is a technique for exploring how a target variable and risk profiles are affected by changes in input variables

It can be implemented to help managers further understand the potential risks and returns of their investment strategies

Economics and Investment Markets

Framework for Analysis

Discounted Cash Flow Model

The value of any asset can be calculated as the present value of its expected cash flows

If a economic factor affects an asset's market value, it must affect one or more of the following

The timing and/or amount of the expected cash flows

One or more of the discount rate components

Default-free interest rate

Expected inflation

Risk premiums

Role of Expectation

Asset values depend on the expectation of future cash flows,which is based on current information that may be relevant to forecasting future cash flows

Asset values may need to be adjusted due to the fact that the unanticipated information arise, as the current asset values only reflect the expected information

Discount Rate

Real Default-Free Rate of Return

The choice to invest today involves the opportunity cost of not consuming today

The tradeoff is measured by the marginal utility of consumption in the future relative to the marginal utility of consumption today

The marginal utility of consumption of investors diminishes as their wealth increases because they have already satisfied fundamental needs

Inter-Temporal Rate of Substitution(ITRS)

Inter-temporal rate of substitution is the ratio of the marginal utility of consuming 1 unit in the future (U_t) to the marginal utility of consuming 1 unit today (U_0), denoted by m_t=U_t/U_0

m_t is always less than 1 because investor always prefer current consumption over future consumption

The inter-temporal rate of substitution is lower at good state of the economy

Discount Rate on Real Default-Free Bond

Assuming a zero coupon, inflation-indexed, risk-free bond with par value of $1, its price today (P_0) should be m_t

If the investment horizon for TIPs is one year, and the payoff then is $1, then the return this bond is R_{real}=\frac{1-P_0}{P_0}=\frac{1}{m_1}-1

The one-period real risk-free rate is inversely related to the inter-temporal rate of substitution

Real risk free rate is positively related to GDP growth rate

Real risk free rate is also positively with the volatility of the growth rate due to higher "risk premium"

Inflation Premium

Short-Term Nominal Interest Rate

Treasury bills (T-bills) are very short-dated nominal zero-coupon government bonds

The yield is short-term nominal default-free interest rate, which s influenced by

The inflation environment and inflation expectations over time. It will also vary with the level of real economic growth and with the expected volatility of that growth Real economic activity, which is influenced by the saving and investment decisions of households

The central bank's policy rate, which should fluctuate around neutral policy

Taylor Rule

Taylor rule provides the targeted short-term rate to balance the risks of inflation and recession

Used as a prescriptive tool to show what target rate will achieve the desired growth

As a forecasting tool to predict actions of the central bank

R=R_{\text{netural}}+\theta+\frac{1}{2}\times(\theta-\theta^\ast)+\frac{1}{2}\times(Y-Y^\ast) R is the central bank policy rate implied by the Taylor rule R_{\text{netural}} is the neutral real policy interest rate \theta is the current inflation rate and \theta^\ast is the target inflation rate Y is the growth of actual real GDP and Y^\ast is the growth of target real GDP

Short-Term vs. Long-Term

Unless the investment horizon is very short, investors are unlikely to be very confident in their ability to forecast inflation accurately

Because we generally assume that investors are risk averse and thus need to be compensated for taking on risk as well as seeking compensation for expected inflation, they will also seek compensation for taking on the uncertainty related to future inflation

For long-term nominal risk-free interest rate, the following effects of inflation should be considered

Premium for expected inflation(\theta)

Risk premium for uncertainty about actual inflation (\pi)

Break-Even Inflation Rate

Break-even inflation rate (BEI) is the yield difference between a non-inflation-indexed risk-free bond and the inflation-indexed risk-free bond with the same maturity

The BEI captures the effects of inflation on yield

BEI=\theta+\pi

Slope of Yield Curve

During the recession, the slope of yield curve will increase

Central bank tends to lower the policy rate

Investors expect higher future GDP growth and higher long-term rates as economic growth recovers

During the recession, short-term bonds generally perform better than long-term bonds Later stages of expansion often have negatively sloped (inverted) yield curve

Typically, high inflation and high short-term interest rate

Low long-term rates due to expectations of decreasing inflation and GDP growth

During the expansion, long-term bonds generally perform better than short-term bonds

Credit Premium

Credit spread(\gamma) is the yield difference between a credit risky bond and a default-free bond with same maturity

It reflects the risk premium for credit risk

Credit spreads tends to narrow in times of robust economic growth, when defaults are less common

Credit risky (lower-rated) bonds will perform better than default-free (higher-rated) bonds

Credit spreads tend to rise in times of economic weakness, as the probability of default rises

Default-free (higher-rated) bonds will perform better than credit risky (lower-rated) bonds

Industry Sector and Company Specific Factors

Some industrial sectors are more sensitive to the business cycle than others

During economic downturn, the credit spread on the consumer cyclical sector rises more dramatically than it do for corporate bonds in the consumer non-cyclical sector

Issuers that are profitable, have low debt interest payments, and that are not heavily reliant on debt financing will tend to have a high credit rating

Sovereign Credit Risk

The credit risk embodied in bonds issued by governments in emerging markets is normally expressed by comparing the yields on these bonds with the yields on bonds with comparable maturity issued by the US

The basic reason for the increase in the credit risk premium was a reassessment by investors of these sovereign issuers ability to pay and the likelihood that they might default

Equity Risk Premium

Yield for equity: \iota +\pi+\theta+\lambda

\lambda is the equity risk premium

The equity risk premium is typically higher than credit risk premium because equity is more risky than debt (\lambda\gt\gamma)

\kappa is essentially the equity risk premium relative to credit risky bonds

Consumption-Hedging Property

Consumption-hedging property describe the feature that may provide high payoff during economic downturns

Assets with more consumption-hedging property will be more highly valued and have less risk premium

The consumption-hedging properties for equities are poor

Sharp falls in equity prices are associated with recessions

Equities are with "bad" consumption hedge, and we would thus expect the equity risk premium to be positive and investors will demand a higher equity risk premium

Valuation Multiples

Valuation multiples are positively related to expected earning growth rate, and negatively related to required rate of return

Booming (recession) economy tends to lead to a rise (decline) of the earning growth expectations

Earning growth rate tend to be relatively stable throughout the business cycle for defensive or non-cyclical industries

Investment Strategy

A value strategy performs well during recession, while growth strategy performs well during expansion

Growth stocks

Strong earnings growth

High P/E and low dividend yield

Have low (or no) positive earnings

Value stocks

Operates in more mature markets with a lower earnings growth

Low P/E and high dividend yield

Capitalization

Small-cap stocks tend to underperform large-cap stocks in difficult economic conditions.

Small-cap companies will tend to have less diversified businesses

Small-cap companies have more difficulty in raising financing particularly during recessions, and will thus be less able to weather an economic storm

Higher risk premium demanded by investors to invest in small-cap stocks relative to large-cap stock due to higher volatility

Rotation Strategies During economic expansion

Rotating into growth stocks when they are expected to outperform value stocks

Rotating into small-cap stocks when they are expected to outperform large-cap stocks

Rotating into cyclical stocks when they are expected to outperform countercyclical stocks

liquidity Premium

Commercial real estate investment have the following characteristics

Bond-like characteristics: steady rental income stream, like cash flows of bonds

Equity-like characteristics: uncertain value of the property at the end of the lease term

Iliquidity

Liquidity Premium

Most of the asset classes are liquid relative to an investment in commercial property

Investors will demand a high risk premium for commercial real estate investment due to weak consumption-hedging properties

Investors will demand a liquidity risk premium \phi

Commercial property value tend to decline in bad times

Active Portfolio Management

Value Added by Active Management

Definition of Value Added

The value added or active return is defined as the difference between the return on the manager's portfolio and the return on a benchmark portfolio

R_A=R_P-R_B

Active Weights

R_A=R_P-R_B=\sum\Delta w_iR_i=\sum\Delta w_iR_{A,i}

\Delta w_i=w_{P,i}-w_{B,i} represents active weights

R_{A,i}=R_i-R_B represents active security return

Individual assets can be overweighed (have positive active weights'or underweighted (have negative active weights), but the complete set of active weights sums to zero

Decomposition of Value Added

For portfolio with multiple asset classes, active return can be decomposed to two sources

R_A=\sum(w_i^P-w_i^B)R_i^B+\sum w_i^P(R_i^P-R_i^B)

Active asset allocation: active weights of asset classes against benchmark portfolio

Security selection: active weights of security within asset classes

Information Ratio

Sharpe Ratio and Information Ratio

Sharpe Ratio

SR_P=\frac{R_P-r_f}{\sigma_P}

Sharpe ratio measures the total risk-adjusted value added, and calculated as excess return per unit of risk

Sharpe ratio is unaffected by the addition of cash or leverage,because excess return and risk will change proportionally

Sharpe ratio is affected by the change of aggressive active weight

Information Ratio

IR_p=\frac{R_P-R_B}{\sigma_{(R_P-R_B)}}

Information ratio measure the relative risk-adjusted value added,and calculated as active returns per unit of active risk

Ex-anti IR is based on expected return

Ex-post IR is based on realized return

Key Conclusions about Information Ratio

Information ratio is unaffected by taking positions in benchmark portfolio

Information ratio is unaffected by the aggressiveness active weight

Information ratio is affected by the addition of cash or use of leverage

Construct Optimal Portfolio

SR and IR

The optimal portfolio will be constructed if SR_P^2=SR_B^2+IR^2

For any given asset class, an investor should choose the manager with the highest expected skill as measured by the information ratio

Because investing with the highest IR manager will produce the highest SR for the investor's portfolio

Optimal Amount of Active Risk

\sigma_{(R_P-R_B)}^\ast=\frac{IR}{SR_B}\times\sigma_{R_B}

For unconstrained portfolios, the level of active risk that leads to the optimal result

The Fundamental Law

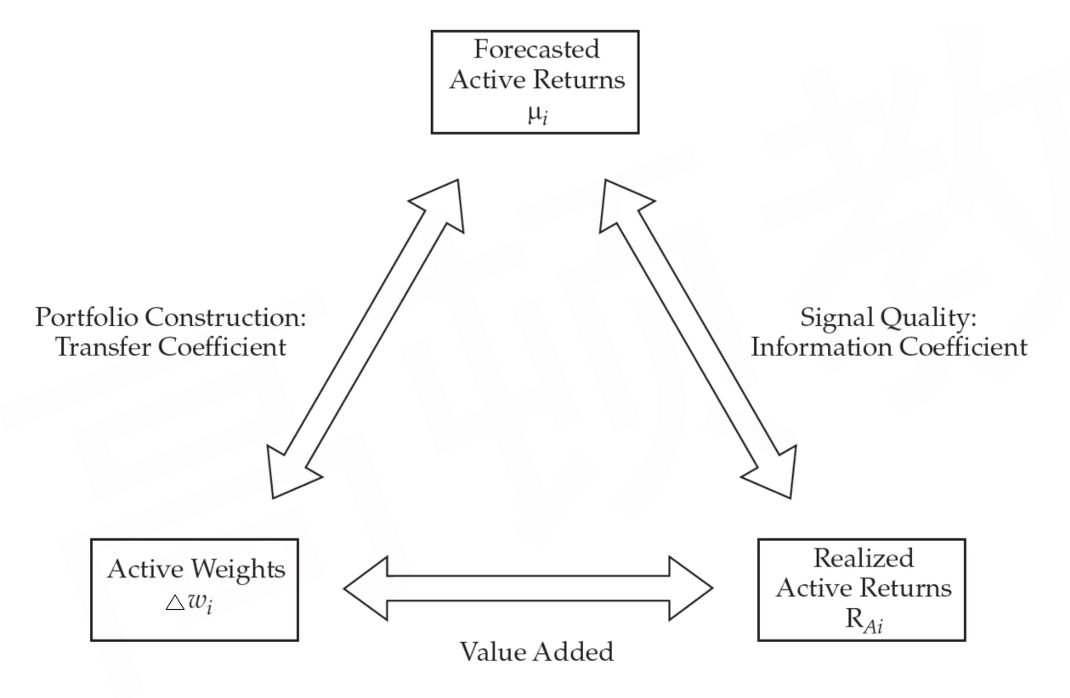

The Correlation Triangle

Information Coefficient

Signal quality is measured by the correlation between the forecasted active returns (\mu_i) at the top of the triangle and the realized active returns (R_{A,i}) at the right corner, commonly called the information coefficient(IC)

IC is a risk-weighted correlation between the active returns and the realized active returns

IC=\rho\left(\frac{R_{A,i}}{\sigma_i},\frac{\mu_i}{\sigma_i}\right)

Ex-ante IC usually be positive

Ex-post IC may be positive or negative

Transfer Coefficient

The correlation between any set of active weights (\Delta w_i) in the left corner, and forecasted active returns (\mu_i) at the top of the triangle,measures the degree to which the investor's forecasts are translated into active weights, called the transfer coefficient (TC)

TC is a correlation between the forecasted active security returns and actual active weights

TC=\rho\left(\frac{\mu_i}{\sigma_i},\Delta w_i\sigma_i\right)

The degree to which the investor's forecasts are translated into active weights

The extent to which constraints reduce the expected value added of the investor's forecasting ability

For portfolios without any constraints → TC = 1

For portfolios with constraints → TC < 1

Basic and Full Fundamental Law

Breadth

Breadth(BR) measures the number of independent active decisions make per year by the manager in constructing the portfolio, which is an indicator of how much efforts the manager has put into

"Independent" means that the active decisions should not be based on highly correlated (or identical) information sets

A practical measure of breadth: BR=\frac{N}{1+(N-1)\rho}

when using derivatives or other forms of hedging strategies (\rho\lt 0),BR may be larger than N

The Fundamental Law

The basic fundamental law IR=IC\times\sqrt{BR} E(R_A)=IR\times\sigma_A=IC\times\sqrt{BR}\times\sigma_A

The full fundamental law IR=TC\times IC\times\sqrt{BR} E(R_A)=IR\times\sigma_A=Tc\times IC\times\sqrt{BR}\times\sigma_A

When take"TC" into consideration: \sigma_A^\ast=\sigma_{(R_P-R_B)}^\ast=\frac{TC\times IR}{SR_B}\times\sigma_{R_B} SR_P^2=SR_B^2+(TC\times IR)^2

Application of the Fundamental Law

Market Timing

Market timing simply bets on the market direction

Information coefficient can be used for inferring market timing

IC = 2 × (% correct)-1

If the manager is correct 50% of the time, then IC = O

This formula is also applicable to evaluate IC of active sector rotation strategies

Most of the fundamental law perspectives discussed up to this point relate to the expected value added through active portfolio management

Expected value added conditional on the realized information coefficient:

Actual performance in any given period will vary from its expected value E(R_A)=TC\times IC\times\sqrt{BR}\times\sigma_A E(R_A\mid IC_{\text{realized}})=TC\times IC_{\text{realized}}\times\sqrt{BR}\times\sigma_A R_A=E(R_A\mid IC_{\text{realized}})+\text{Noise}

An ex-post (i.e. realized) decomposition of the portfolios active return variance into two parts

Variation due to the realized information coefficient (TC^2)

Variation due to constraint-induced noise(1-TC^2)

Limitations of the Fundamental Law

Poor input estimates lead to incorrect evaluation

Uncertainty in ex-ante measurement of skill

IC is difficult to justify due to existence of the bias, various asset segments, or different time periods

Assumption of independence of active decisions

The number of individual assets is not an adequate measure of strategy breadth (BR) when the active returns between individual assets are correlated