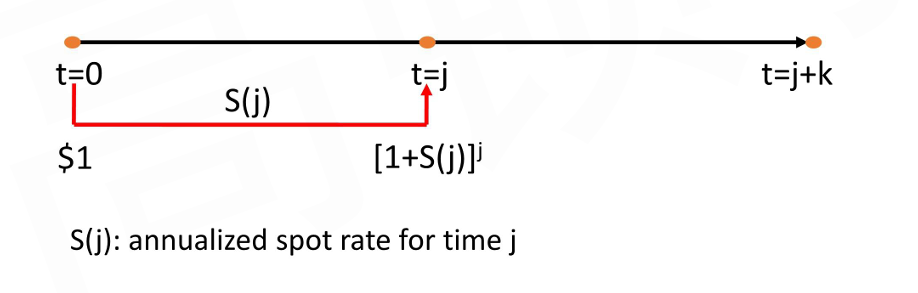

Spot rate is the rate of interest on a security that makes a single payment at a future point in time

The annualized return (also can be interpreted as the yield to maturity) on an option-free and default-risk-free zero-coupon bond

Also known as zero-coupon rate or zero rate

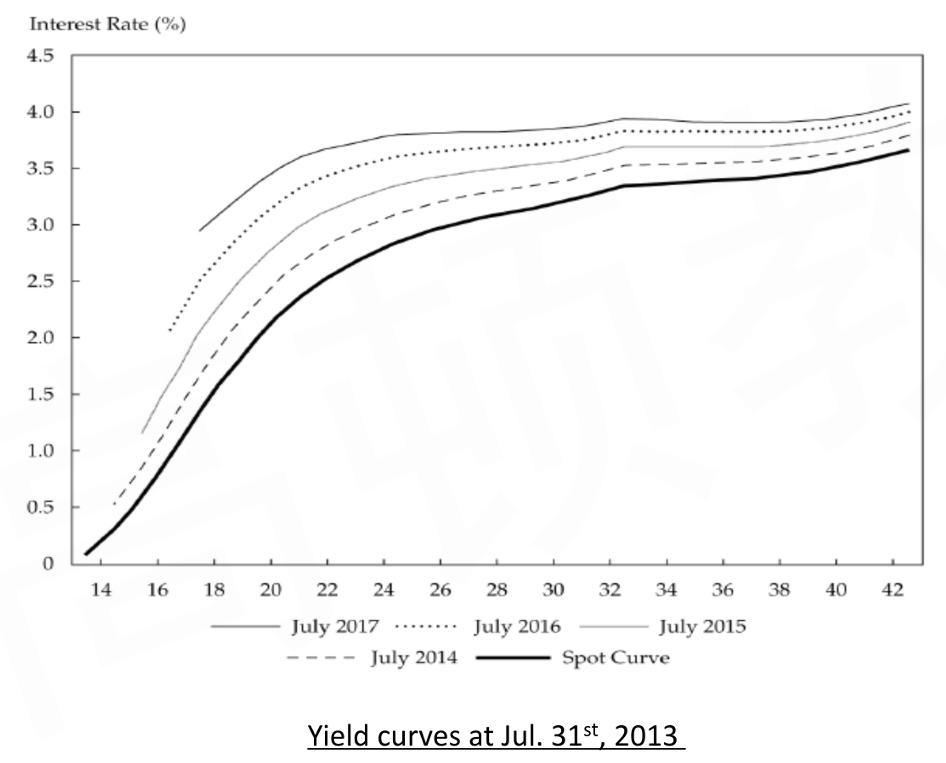

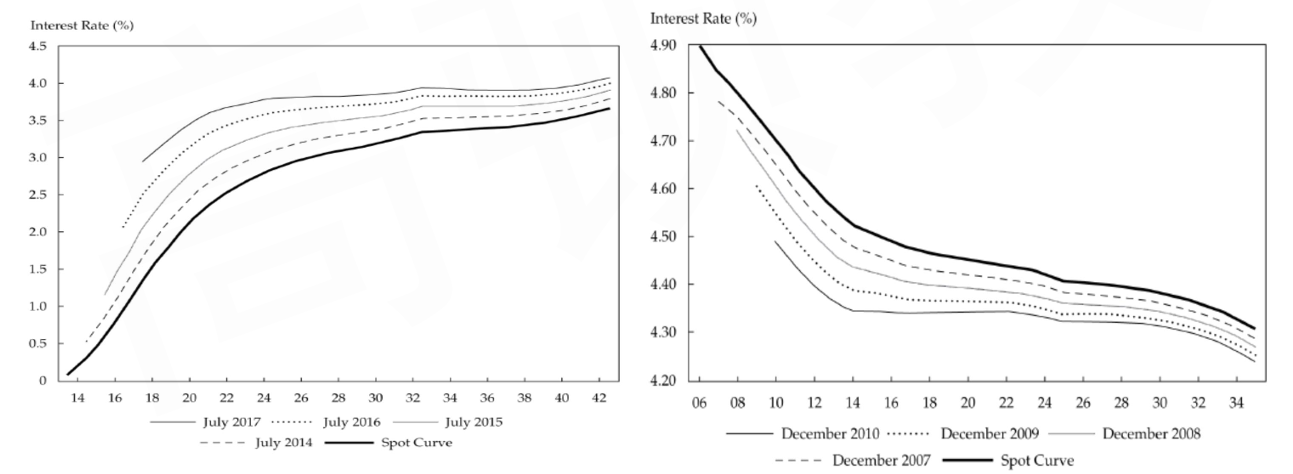

Spot Curve

Spot curve: the term structure of spot rates, the graph of the spot rate versus maturity

The shape and level of the spot yield curve are dynamic

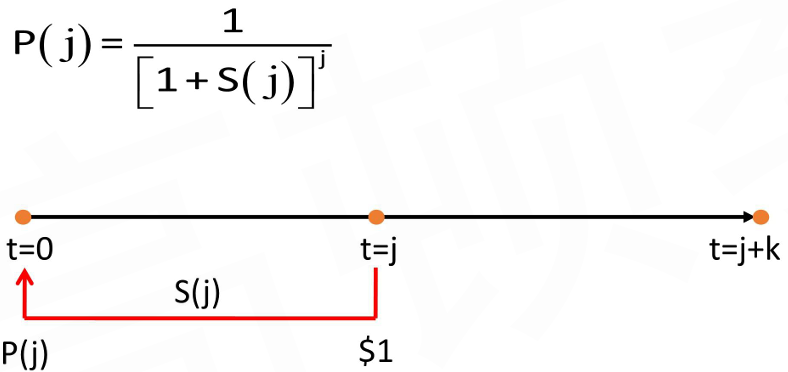

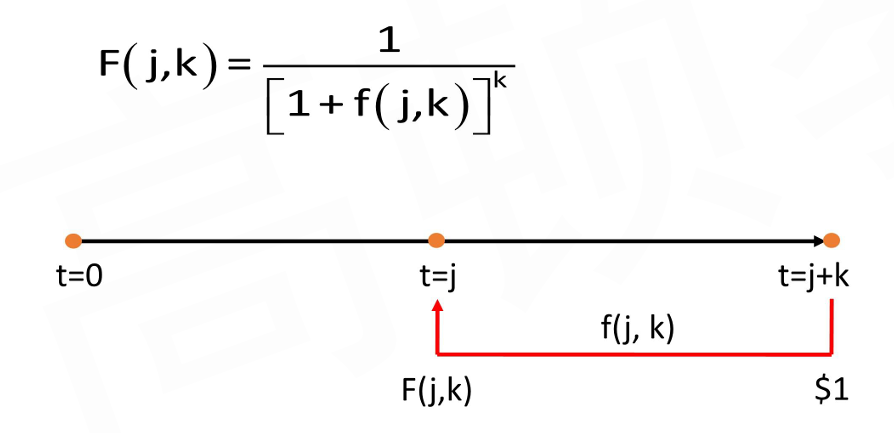

Discount Factor

It is the price of a risk-free single-unit payment at time j

Forward Rate

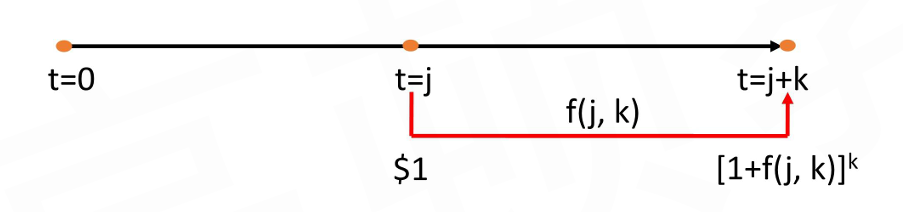

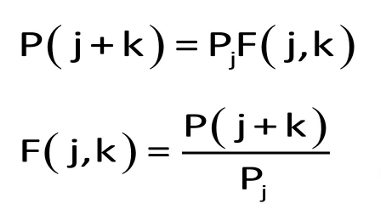

Forward rate is the rate of interest set today for a single-payment security to be issued at a future date

f(j, k): annualized k-year forward rate starting at time j

Discount Factor

The price at time j years from today for a zero-coupon bond with maturity (j+k) years and unit principal

Forward Rate Curve

The term structure of forward rates, the graph of the forward rate versus maturity

It represents the term structure of forward rates for a loan made on a specific initiation date

Forward Rate Models

Forward rate models show how forward rates can be extrapolated from spot rates

Forward Pricing Model

The forward pricing model describes the valuation of forward contracts

Spot Curve vs. Forward Curve

If the spot curve is upward sloping, forward curves lie above the spot curve

The later the initiation date, the higher the forward curve

If the spot curve is downward sloping, forward curves lie below the spot curve

The later the initiation date, the lower the forward curves

Yield Curve Shapes

In developed markets, yield curves are most commonly upward sloping with diminishing marginal increases in yield for identical changes in maturity

An inverted yield curve is uncommon and such term structure may reflect a market expectation of declining future inflation rates

A flat yield curve typically occurs briefly in the transition from an upward-sloping to a downward-sloping yield curve, or vice versa.

A humped驼峰 yield curve, which is relatively rare, occurs when intermediate-term interest rates are higher than short- and long-term rates

Par Rate

Par Rate and Par Curve

Par rate is the coupon rate for bond that would result in bond price equals to its par value

Par curve represents the yields to maturity/coupon rate/par rate on coupon-paying government bonds, priced at par, over a range of maturities

Recently issued("on the run") bonds are typically used to create the par curve because new issues are typically priced at or close to par

Bootstrapping

Spot rates may be obtained from the par curve by bootstrapping

YTM

YTM is the internal rate of return of on the cash flow, it reflects the implied single market discount rate

For coupon bonds, if the spot curve is not flat, the YTM will not be the same as the spot rate

YTM is the same as the spot rate for zero-coupon bonds

YTM is some weighted average of spot rates

Expected Return vs. Realized Return

Expected return is the ex-ante return that a bondholder expects to earn

The YTM is the expected return and will be realized only if all the three critical assumptions for YTM are met

Realized return is the actual return on the bond during the time an investor holds the bond

It is based on actual reinvestment rates and the yield curve at the end of the holding period

The YTM can provide a poor estimate of expected return if:

interest rates are volatile

the yield curve is steeply sloped, either upward or downward

there is significant risk of default

the bond has one or more embedded options (e.g., put, call, or conversion)

Implicit in the determination of the yield to maturity as a potentially realistic estimate of expected return is a flat yield curve

Swap Rate

Swap rate is the interest rate for the fixed-rate leg of an interest rate swap

Determining swap rate

The right side is the value of the floating leg, which is 1 at origination

The swap rate is determined by equating the value of the fixed leg, on the left-hand side to the value of the floating rate

Swap Curve

The yield curve of swap rates is called the swap rate curve (swap curve)

Because it is based on so-called par swaps, the swap curve is a type of par curve

Swap Curves vs Government Spot Curves

The swap market has more maturities

Many countries do not have a liquid government bond market with maturities longer than one year

The swap market is a highly liquid market

Unlike bonds, a swap does not have multiple borrowers or lenders, only counterparties who exchange cash flows

Swaps provide one of the most efficient ways to hedge interest rate risk

Swap rates reflect the credit risk of commercial banks rather than governments

Swap market is unregulated (not controlled by governments),so swap rates are more comparable across different countries

Spread

Swap Spread

Swap spread is the amount by which the swap rate exceeds the rate of the "on-the-run" government security with the same maturity

Swap spread = swap rate - government security rate

Swap spread shows the Treasury rate can differ from the swap rate for the same term

Unlike the cash flows from US Treasury bonds, the cash flows from swaps are subject to much higher default risk

Market liquidity for any specific maturity may differ: some parts of the term structure of interest rates may be more actively treaded with swaps than with Treasury bonds

I- Spread

I-spreads are the bond rates net of the swap rates of the same maturities

I-spread = bond rate - swap rate

I-spread reflects compensation for credit and liquidity risks

TED Spread

The TED spread is calculated as the difference between Libor and the yield on a T-bill of matching maturity

TED = LIBOR - T-bill rate

TED spread is an indicator of perceived credit risk in the general economy

TED spread can also be thought of as a measure of counterparty risk

TED spread more accurately reflects risk in the banking system

An increase in the TED spread is a sign that lenders believe the risk of default on interbank loans is increasing

Libor-OIS Spread

Libor-OIS spread is the difference between Libor and the overnight indexed swap(OIS) rate

OIS is an interest rate swap in which the periodic floating rate is equal to the geometric average of an overnight index rate over every day of the payment period

The Libor-OlS spread is considered an indicator of the risk and liquidity of money market securities

Z-Spread

Z-spread is the constant spread that would need to be added to the implied spot curve so that the discounted cash flows of a bond are equal to its current market price

Implied assumption: the yield curve makes a parallel shift

Under the assumption of zero interest rate volatility, it is not appropriate for bonds with embedded options

Term Structure Theories

Pure Expectation Theory/Unbiased Expectation Theory

Pure expectation theory suggests that the forward rate is an unbiased predictor of the future spot rate

If yield curve is upward sloping, short-term rates are expected to rise

If yield curve is downward sloping, short-term rates are expected to fall

If yield curve is flat, short-term rates are expected to remain constant

Its interpretation is that bonds of any maturity are perfect substitutes for one another

The predictions of the unbiased expectations theory are consistent with the assumption of risk neutrality

This assumption is a significant shortcoming because investors are risk averse

Local Expectation Theory

Local expectation theory assumes risk-neutrality only in the short term while incorporate uncertainty in the long term

Under this theory, the expected return for every bond over short time periods is the same

But it is often observed that short-holding-period returns on long-dated bonds do exceed those on short-dated bonds

The need for liquidity and the ability to hedge risk essentially ensure that the demand for short-term securities will exceed that for long-term securities

Liquidity Preference Theory

Liquidity preference theory asserts that liquidity premiums exist to compensate investors for the added interest rate risk they face when lending long term Forward rate = expected from spot rates + liquidity premium

Liquidity premium increase with maturity

Segmented Markets Theory

Under segmented markets theory, each maturity sector can be thought of as a segmented market in which yield is determined by supply of and demand for loan, and independent from the yields in other maturity segments

Consistent with a world where there are asset-liability management constraints

Yields are not a reflection of expected spot rates or liquidity premiums

Preferred Habitat Theory

Preferred habitat theory contends that if the premium is large enough, investor will deviate from their preferred maturities or habitats

Premium is not directly related to maturity

Based on the realistic notion that investors will accept additional risk in return for additional expected returns

Yield Curve Factor Models

Yield Curve Movement

The yield curve movements can be decomposed into

parallel movement (\Delta X_L)

steepness movement (\Delta X_S)

curvature movements (\Delta X_C)

Parallel shift(level) → effective duration

Changes in Level rates 77%

Non-parallel shift → key rate duration

Steepness: Slope changes 17%

Curvature: Curvature changes 3%

Yield Curve Risk

Yield curve risk (Shaping risk) is the risk to portfolio value arising from unanticipated changes in the yield curve

Effective duration: measures the sensitivity of a bond's price to a small parallel shift in a benchmark yield curve Address risk associated with parallel yield curve changes

key rate duration: measures a bond's sensitivity to a small change in a benchmark yield curve at a specific maturity segment Allows identification and management of "shaping risk"

Decompose the Risk

The proportional change in portfolio value resulted from yield curve movement can be modeled as:

\frac{\Delta P}{P} \approx-D_L \Delta X_L-D_S \Delta X_S-D_C \Delta X_C

D_L, D_S, and D_C as the sensitivities of portfolio value to small changes in the level, steepness, and curvature, respectively

Key Rate Duration

Key rate duration measures the bond price sensitivity to a small change in a benchmark yield curve at a specific maturity segment

Effective duration is an adequate measure of bond price risk only for small paralleled shifts in the yield curve

For the portfolio that is composed by zero-coupon bonds:

A representation of the yield volatility of a zero-coupon bond for every maturity of security

The volatility term structure typically shows that short-term rates are more volatile than long-term rates Short-term volatility is most strongly linked to uncertainty regarding monetary policy Long-term volatility is most strongly linked to uncertainty regarding the real economy and inflation

On the basis of the typical assumption of a lognormal model, the uncertainty of an interest rate is measured by the annualized standard deviation of the proportional change in a bond yield over a specified time interval

Active Bond Portfolio Management

Strategy of Forward Contract

Forward contract's price is settled today

Forward contract's value remains unchanged as long as future spot rates evolve as predicted by today's forward rate

A change in the forward contract's value reflects a deviation of the future spot rates from that predicted by today's forward rate

An active portfolio manager may outperform the overall market if the manager can predict how future spot rates will differ from the current implied forward rates

If a trader expects that the future spot rate will be lower than what is predicted by the prevailing forward rate

The forward contract value is expected to increase

The trader would long the forward contract

If a trader expects the future spot rate to be higher than what is predicted by the existing forward rate

The forward contract value is expected to decrease

The trader would short the forward contract

Riding the Yield Curve

When a yield curve is upward sloping and the trader believes that the yield curve will not change its level and shape, then buying bonds with a maturity longer than the investment horizon would provide a total return greater than the return on a maturity-matching strategy

When the yield curve slopes upward, as a bond approaches maturity or "rolls down the yield curve", it is valued at successively lower yields and higher prices

Macroeconomic Variables

Bond Risk Premium

Interest rate dynamics are influenced by key economic variables and market events

The bond risk premium (a.k.a. term (or duration) premium) refers to the expected excess return of a default-free long-term bond less that of an equivalent short-term bond or the one-period risk-free rate

Unlike ex post observed historical returns, the bond risk premium is a forward-looking expectation and must be estimated

Macroeconomic Factors Influence

Several macroeconomic factors influence bond pricing and required returns

Research shows that inflation explains about two-thirds of long-term bond yield variation,with the remaining third roughly equally attributable to economic growth and factors including monetary policy

Monetary policy explains nearly two-thirds of short-and intermediate-term yield variation, and the remaining third is largely attributable to inflation

Monetary policy

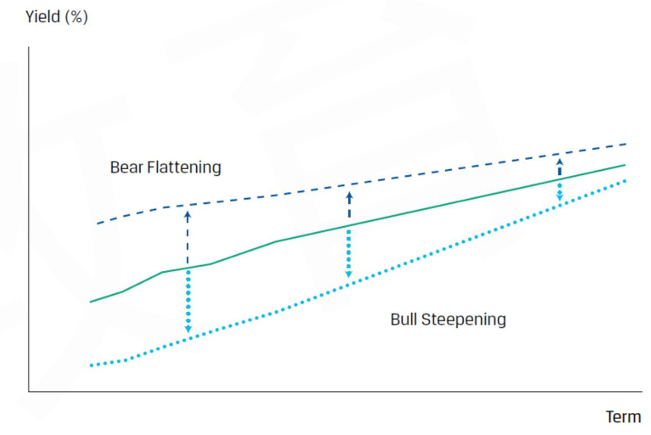

During economic expansions, monetary authorities raise benchmark rates to help control inflation, and this action is often consistent with bearish flattening,or short-term bond yields rising more than long-term bond yields, resulting in a flatter yield curve

During economic recessions or anticipated recessions,the monetary authority cuts benchmark rates to help stimulate economic activity, and the lowering of interest rates is associated with bullish steepening, in which short-term rates fall by more than long-term yields, resulting in a steeper term structure

Fiscal policy

Fiscal supply-side effects affect bond prices and yields by increasing(decreasing) yields when budget deficits rise(fall)

Longer government debt maturity structures predict greater excess bond returns

This is effectively a segmented market factor, wherein the greater supply of bonds of long-term maturity increases the yield in that market segment

Investor Demand

Domestic investor demand is a key driver of bond prices

Greater domestic investor demand increases prices and reduces the bond risk premium

Non-domestic investor demand influences government bond prices and may result either from holding reserves or from actions associated with currency exchange rate management

Non-domestic flows significantly influence bond prices because inflows (outflows) bid up (down) bond prices, lowering (raising) the bond risk premium

Investor Strategies

During highly uncertain market periods, investors flock to government bonds in what is termed a flight to quality

A flight to quality is often associated with bullish flattening, in which the yield curve flattens as long-term rates fall by more than short-term rates

An investor may seek to capitalize on an expected bullish flattening of the yield curve by shifting from a bullet to a barbell position

Investors expecting interest rates to fall will generally extend portfolio duration

To capitalize on a steeper curve, an arbitrager will short long-term bonds and purchase short-term bonds

The position may be designed as duration neutral in order to insulate from changes in the level of the term structure

Arbitrage-Free Valuation Framework

Arbitrage-Free Valuation

Arbitrage Opportunities

Arbitrage opportunities are opportunities for trades that earn riskless profits without any net investment of money

Arbitrage opportunities arise as a result of violations of the law of one price

Two goods that are perfect substitutes must sell for the same current price in the absence of transaction costs

Otherwise, buying the lower and selling the higher will earn riskless profit, and make the two prices converge

Two types of arbitrage opportunities:

Value additivity: the value of the whole must equal the sum of the values of the parts Stripping: separate the bond's individual cash flows and trade them as zero-coupon securities Reconstitution: recombine the individual zero coupon securities and reproduce the underlying coupon bond

Dominance: a financial asset with a risk-free payoff in the future must have a positive price today

Arbitrage-Free Valuation

Arbitrage-free valuation is an approach to security valuation that determines security values that are consistent with the absence of an arbitrage opportunity(value additivity) through stripping and reconstitution

For option-free bonds

P=\sum_{t=1}^n \frac{P M T_t}{\left(1+Z_t\right)^t}+\frac{F}{\left(1+Z_n\right)^n}

Using spot rates that correspond to the maturities of the zero-coupon bonds to calculate the bond price

If market price is different with the calculated price, there is an arbitrage opportunity of "value additivity"

For bonds that have embedded options

The challenge one faces when developing a framework for valuing bonds with embedded options is that their expected future cash flows are depend on the change of interest rate

Changes in future interest rates impact the likelihood the option will be exercised and impact the cash flows

In order to develop a framework that values both bonds without and with embedded options, we must allow interest rates to take on different potential values in the future based on some assumed level of volatility

Term Structure Models

Modern Term Structure Models

Term structure models provide quantitatively precise descriptions of how interest rates evolve

Equilibrium term structure models: describe the dynamics of the term structure using fundamental economic variables that are assumed to affect interest rates

Cox-Ingersoll-Ross(CIR) model

Vasicek model

Arbitrage free models: assume bonds trading in the market are correctly priced (arbitrage free)

Ho-Lee model

Kalotay-Williams-Fabozzi (KWF) model

CIR Model

Higher interest rate → more investing → more capital supply → lower interest rate; and vice versa

Ultimately, interest rates will reach a market equilibrium rate at which no one needs to borrow or lend

Cox-Ingersoll-Ross (CIR) model is based on the idea that individuals must determine his optimal trade-off between consumption today and investing and consuming at a later time

\mathrm d {r}_{{t}}={k}\left(\theta-{r}_{{t}}\right) {\mathrm d t}+{\sigma} \sqrt{{r}_{{t}}} {\mathrm d Z}

\mathrm dr_t: a infinitely small change in short-term interest rate \mathrm dt: a infinitely small increase in time \theta: long-run value of the short-term interest rate r_t: the short-term interest rate k: a positive parameter for speed of mean reversion adjustment and the higher/lower, the quicker/slower \sigma: interest rate volatility \mathrm dZ: an infinitely small movement in a "random walk"

Drift term: {k}\left(\theta-{r}_{{t}}\right) {\mathrm d t}, which means the interest rate is mean-revert to long term value "0" with speed presented by parameter "k", also named deterministic term

Stochastic term: {\sigma} \sqrt{{r}_{{t}}} {\mathrm d Z}, also named volatility term. \sqrt{{r}_{{t}}} in the stochastic term tries to prevent interest rate to be non-negative, and assets that higher interest rate will lead to higher volatility

Vasicek model

\mathrm d {r}_{{t}}={k}\left(\theta-{r}_{{t}}\right) {\mathrm d t}+{\sigma} {\mathrm d Z}

Disadvantages of Vasicek model

Does not force interest rates to be non-negative

Volatility remains constant over the period of analysis

Ho-Lee model

\mathrm d {r}_{{t}}=\theta_t {\mathrm d t}+{\sigma} {\mathrm d Z}

The drift term, \theta_t, is time dependent, which means there is a value for \theta_t, at each time step

The Ho-Lee model, similar to the Vasicek model, has constant volatility, and interest rates may become negative

KWF Model

\mathrm d \ln{r}_{{t}}=\theta_t {\mathrm d t}+{\sigma} {\mathrm d Z}

The KWF model is analogous to the Ho-Lee model in that it assumes constant drift, no mean reversion, and constant volatility

KWF model describes the dynamics of the log of the short rate, and as a result, the log of the short rate is distributed normally, meaning the short rate itself is distributed lognormally.

The main implication of modeling the log of the short rate is that it will prevent negative rates

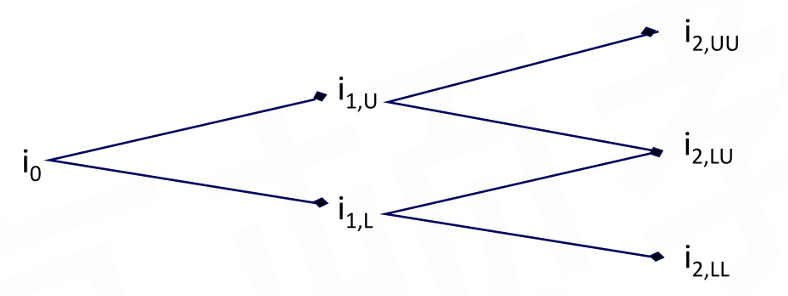

Binomial Tree Model

Binomial Interest Rate Tree

A interest rate model that assumes interest rates at any point of time(node) have an equal probability of taking one of two possible values in the next period, an upper path (U) and a lower path (L)

The binomial interest rate tree framework is a lognormal random walk(lognormal tree) that insures two appealing properties:

i_{1, U}=i_{1, L} \times e^{2\sigma} \quad i_{2, U U}=i_{2, L U} \times e^{2\sigma} \quad i_{2, U U}=i_{2, L L} \times e^{4\sigma}

Non-negativity of interest rates

higher volatility at higher interest rates

Estimation of volatility

Historical interest rate volatility: volatility is calculated by using data from the recent past with the assumption that what has happened recently is indicative of the future

Value bond by moving backward from last period to time 0

Bond value at any node is the average PV of two possible values from next period

Discount rate is the one-period forward rate at that node

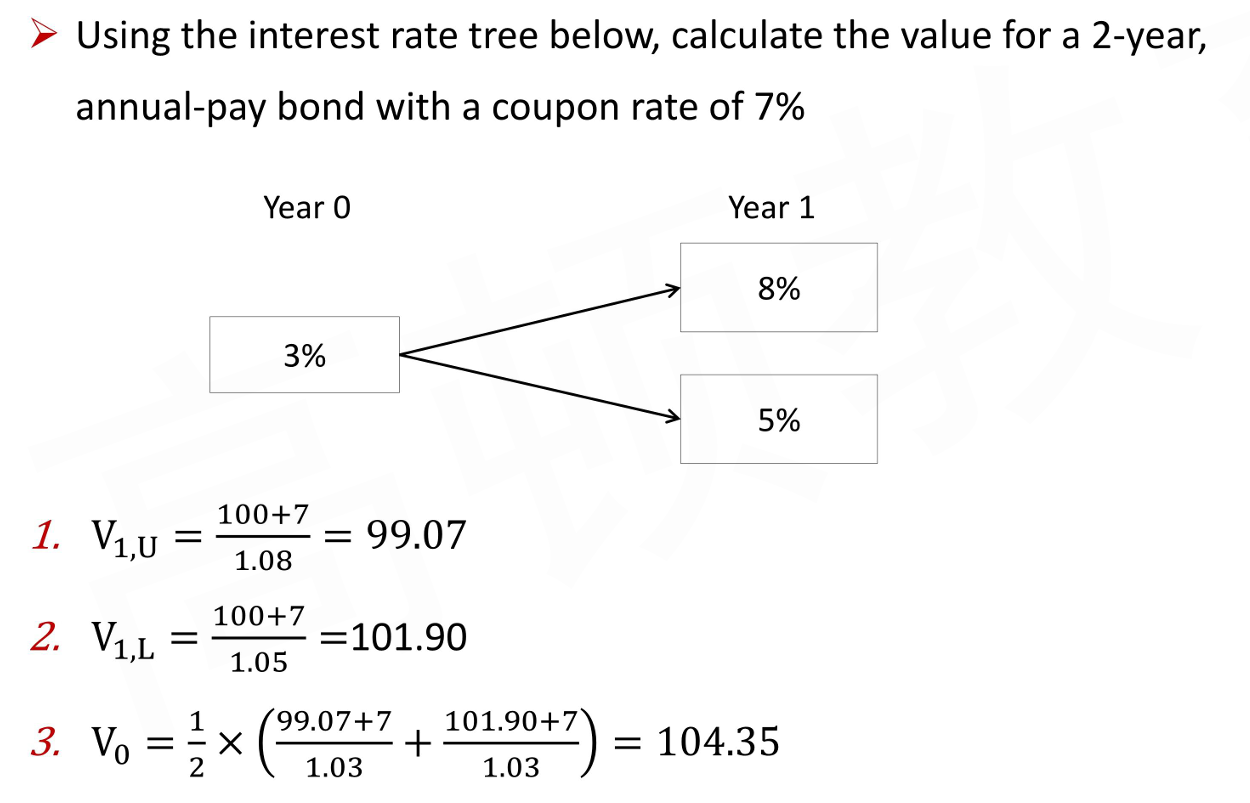

Example

Pathwise Valuation

For a binomial interest rate tree with n period, there will be 2^n paths

Calculate the present value of a bond for each possible interest rate path and takes the average of these values across paths

Monte Carlo Method

Binomial tree backward induction assumes cash flows are not path dependent, therefore it cannot value the securities with such cash flow.

Path dependency: cash flow to be received in a particular period depends on the path followed to reach its current level as well as the current level itself

Monte Carlo forward-rate simulation involves randomly generating a large number of interest rate paths, and it is often used when a security's cash flow are path dependent

For example, the valuation of MBS depends to a great extent on the level of prepayments, which are interest rate path dependent

Using the procedure just described, the model will produce benchmark bond values equal to the market prices only by chance

The constant added to all short interest rates is called a drift term

The model is said to be drift adjusted

Increasing the number of paths increases the accuracy of the estimate in a statistical sense

Yield curve modelers often include in the Monte Carlo estimation is mean reversion

We implement mean reversion by implementing upper and lower bounds on the random process generating future interest rates

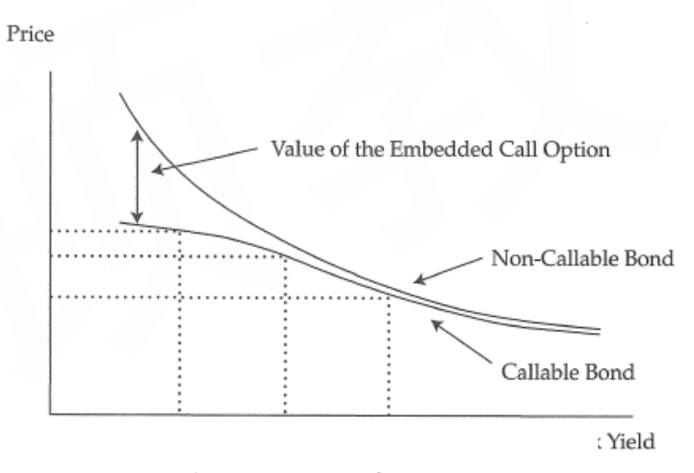

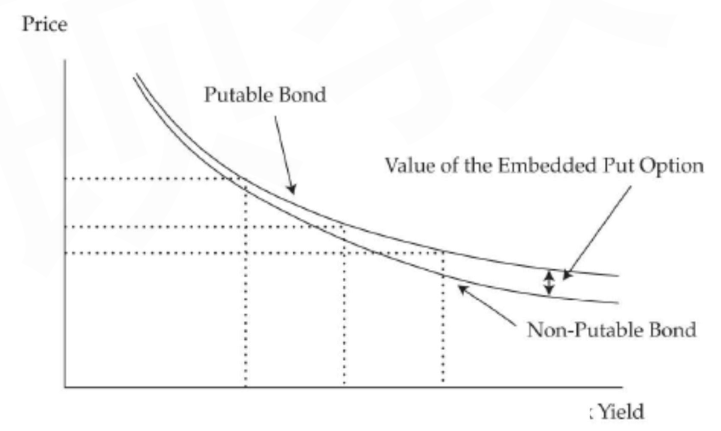

Bonds with Embedded Options

Callable and Putable Bond

Bonds with Embedded Option

Basic Concepts

Callable Bond

Callable bonds give the issuer the option to call back the bond

Investor is long the straight bond but short the call option on the bond

At maturity, the holder of an extendible展期 bond has the right to keep the bond for a number of years after maturity, possibly with a different coupon

Putable and extendible bonds are equivalent

Convertible bond allows bondholders to convert their bonds into the issuer's common stock

Bonds with estate put allows the heirs继承人 of an investor to put the bond back to the issuer upon the death of the investor

The value of the estate put depends on the bondholder's life expectancy

The shorter the life expectancy, the greater the value of the estate put

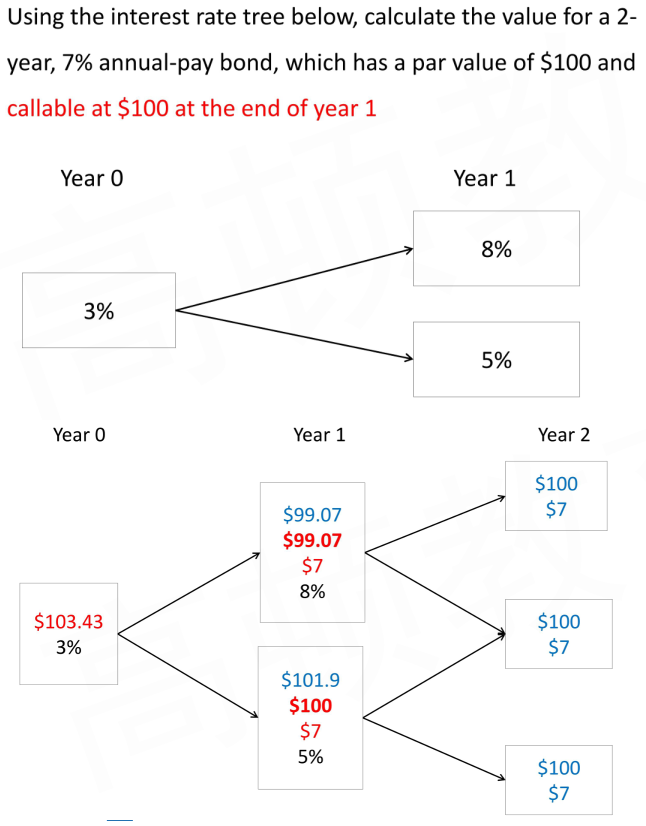

Valuation by Binomial Interest Rate Tree

The basic process to value a bond with embedded option is similar to the valuation of straight bond

However, the following two points are different

Only binomial interest rate tree model is applicable, valuation with spot rates is non-available any more

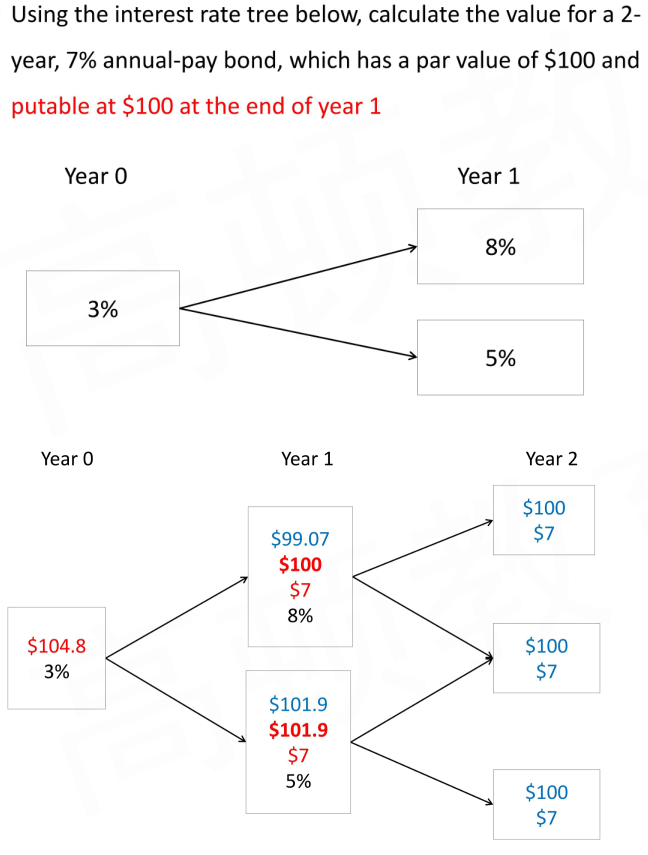

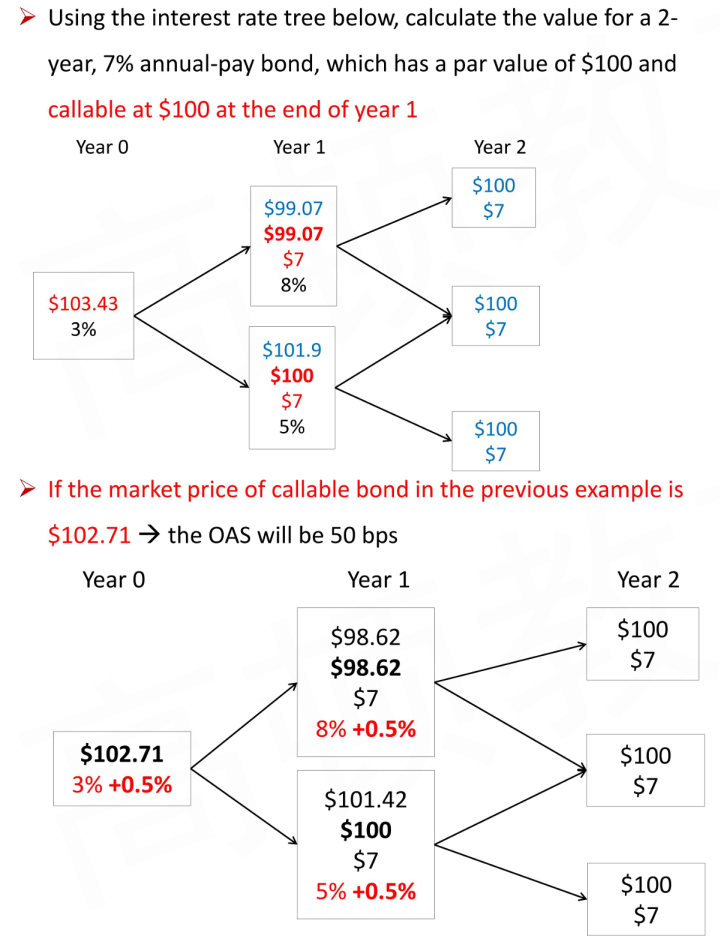

Need to check at each node to determine whether the embedded option will be exercised or not Call rule: the value of callable bond is the lower of the call price and the calculated price if the bond is not called Put rule: the value of putable bond is the higher of the put price and the calculated price if the bond is not put

Example of Callable Bond

Example of Putable Bond

Effects of Interest Rate Volatility

R_u=R_d \times e^{2\sigma \sqrt{t}}

R_d is the rate in the down state

\sigma is the interest rate volatility

t is the time in years between "time slices" (a year, so here t = 1)

Effects of Interest Rate Volatility

The value of a straight bond is unaffected by changes in the volatility of interest rate

Interest rate volatility affects the value of a callable or putable bond

The values of call and put options increase when interest rate volatility increases

As interest rate volatility increases, the value of the callable bond decreases

As interest rate volatility increases, the value of the putable bond increases

Option Adjusted Spread

Calculation of OAS

Option adjusted spread

yield spread that remove the influence of embedded option

When valuing risky bond with the interest rate tree generated from government spot curve, the model does not produce arbitrage-free price (typically higher than market price)

Option-adjusted spread(OAS) is the constant spread that, when added to all the one-period forward rates on the interest rate tree, makes the model price of the bond equal to its market price

OAS = Z-spread - Option value(%)

Callable bond → option value > 0 → OAS < Z-spread

Putable bond → option value < 0 → OAS > Z-spread

Example

Application of OAS

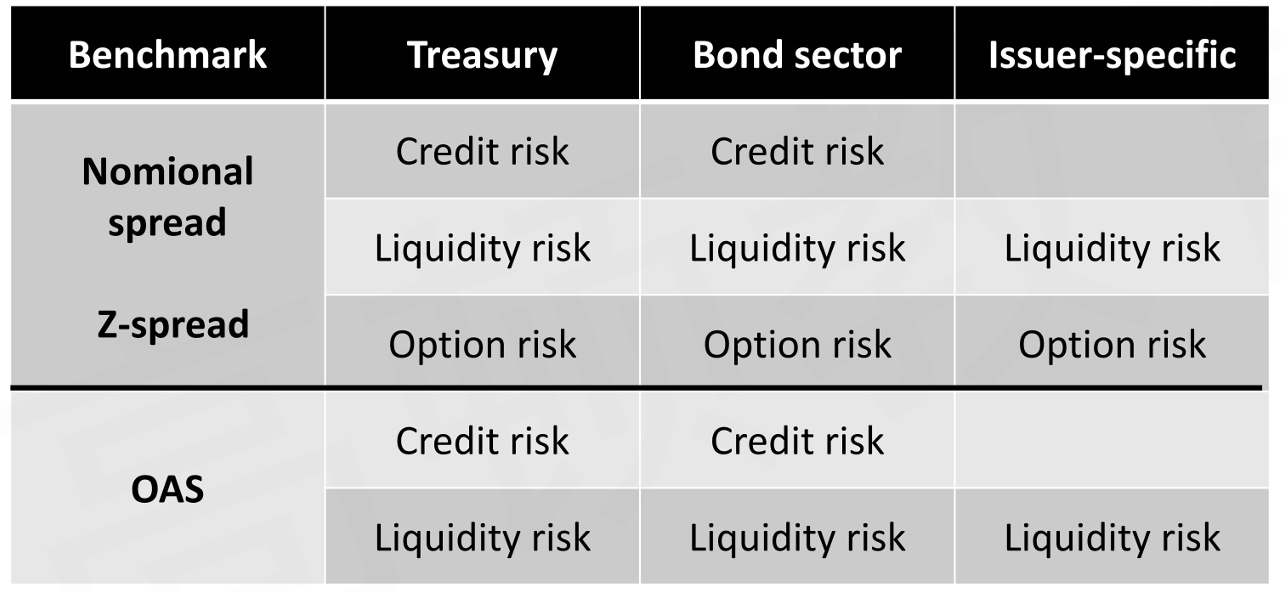

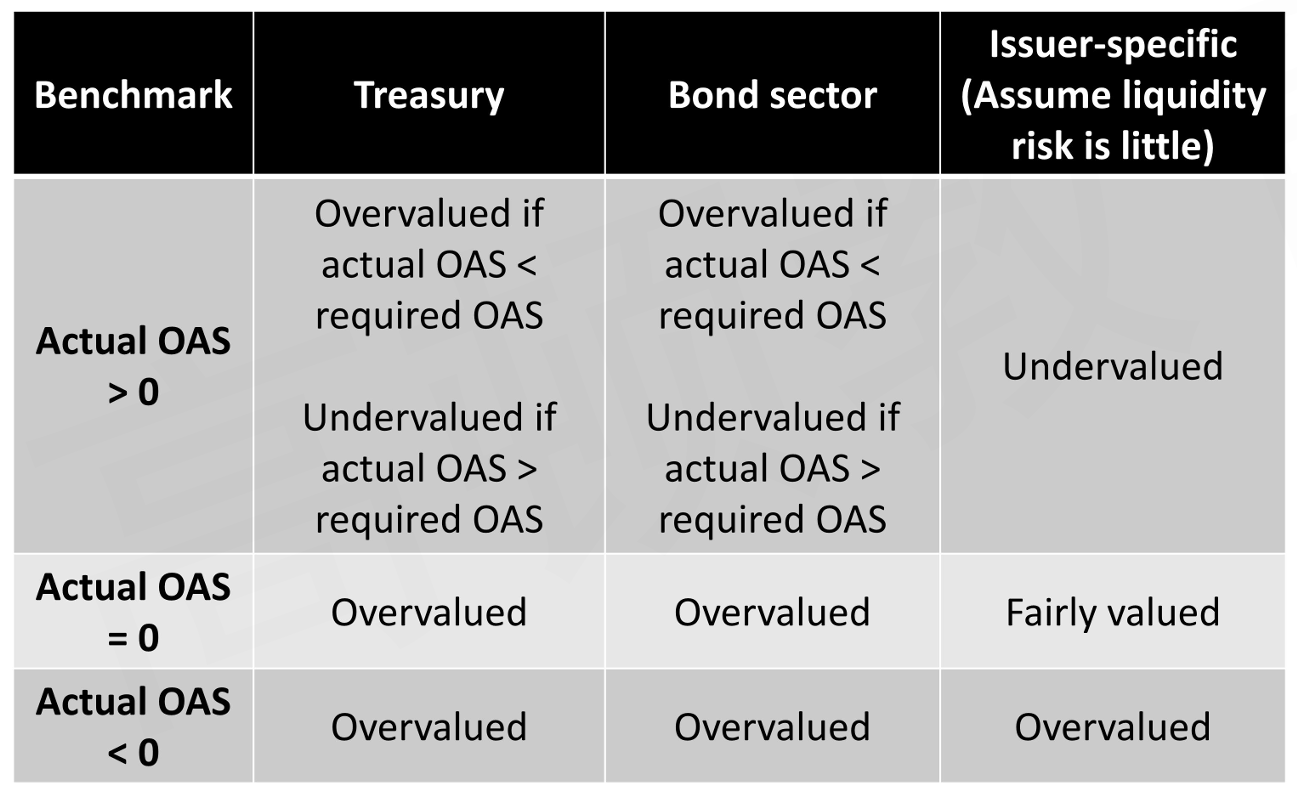

Comparison between Spreads

Option-Adjusted Spread

Interest Rate Volatility vs. OAS

The effect of volatility on the OAS for a bond embedded with option

As interest rate volatility increase, the OAS for the callable bond decreases

As interest rate volatility increase, the OAS for the putable bond increases

Interest Rate Risk

Effects of changes in the Shape of Yield Curve

As interest rates decline, the value of the callable bond rises less rapidly than the value of the straight bond, limiting the upside potential for the investor

Call option value increases as interest rate decline

The rise of the straight bond value is partially offset by the increase in the value of the call option

As interest rates rise, the value of the putable bond falls less rapidly than the value of the straight bond

Put option value increases as interest rates rise

The decline of the straight bond value is partially offset by the increase in the value of the put option

As the yield curve moves from being upward sloping, to flat, to downward sloping, the value of the call option increases

The one-period forward rates become lower and the opportunities to call increase

As the yield curve moves from being upward sloping, to flat, to downward sloping, the value of the put option decreases

The one-period forward rates become lower and the opportunities to put declines

Effective Duration

In the presence of embedded options, we use the binomial model to compute effective duration, and the process to calculate the PV_- and PV_+, is as following:

calculate the implied OAS to the current binomial tree according to the market price (PV_0)

shift the benchmark yield curve down by ,generate a new interest rate tree, and then calculate the PV_- using the OAS calculated in step 1

shift the benchmark yield curve up by , and calculate the PV_+. with similar method

calculate the bond's effective duration using the formula

Properties of Effective Duration

ED of zero-coupon bond ≈ maturity of the zero-coupon bond

ED of fixed-rate bond < maturity of the fixed-rate bond

ED of floating-rate bond ≈ time (years) to next reset

ED of both callable and putable bond ≤ ED of of identical straight bond

Decrease of interest rate will decrease the effective duration of callable bond

Increase of interest rate will decrease the effective duration of putable bond

Effective Convexity

Straight bond

Always exhibits low positive convexity

The increase in the value of an option-free bond is higher when rates fall than the decrease in value when rates increase by an equal amount

Callable bond

When interest rates are high, callable and straight bond have similar positive convexity

When the call option is in the money, the effective convexity of the callable bond turns negative

Putable bond

Always have positive convexity

When the put option is in the money, the effective convexity of the putable bond is higher than straight bond

One-Sided Duration

One-sided durations are the effective durations when interest rate curves go up or down

One-sided durations are better at capturing the interest rate sensitivity of a callable or putable bond than the(two-side)effective duration, particularly when the embedded option is near the money

One-side up-duration: durations that apply only when interest rate curve rises

One-side down-duration: durations that apply only when interest rate curve falls

Key Rate Duration

Definition of Key Rate Duration

Key rate durations measure the sensitivity of the bond's price to changes in specific maturities on the benchmark yield curve

Shifting any par rate has an effect on the value of the bond

Key rate durations help to identify the "shaping risk" for bonds Shaping risk: the sensitivity of bond's price to changes in the shape of the yield curve (e.g., steepening and flattening)

For option-free bond that is traded at par

Bond's maturity matched rate is the only rate that affects the bond's value

All other key rate durations are zero

For option-free bond that is not traded at par

Shift the maturity-matched par rate has the greatest effect

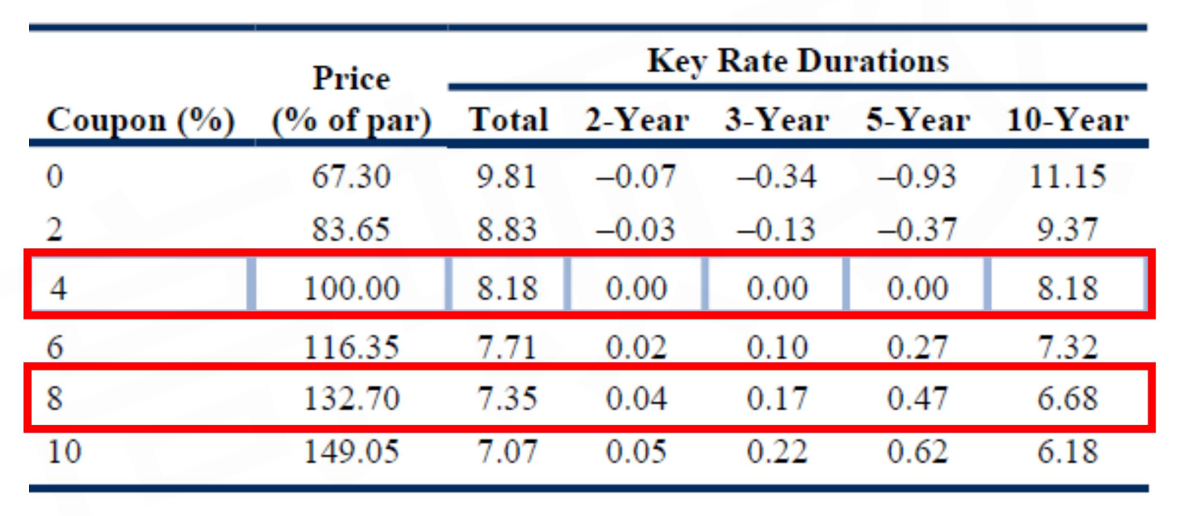

Example for Key Rate Durations of 10-Year Option-Free Bonds Valued at a 4% Flat Yield Curve

For callable bonds

With low coupon rate

The callable bonds are unlikely to be called

The rate that has the highest effect on the value of the callable bond is the maturity-matched rate

As the bond's coupon increase

So does the likelihood of the bond being called

The rate that has the highest effect on the callable bond value is the time-to-exercise rate

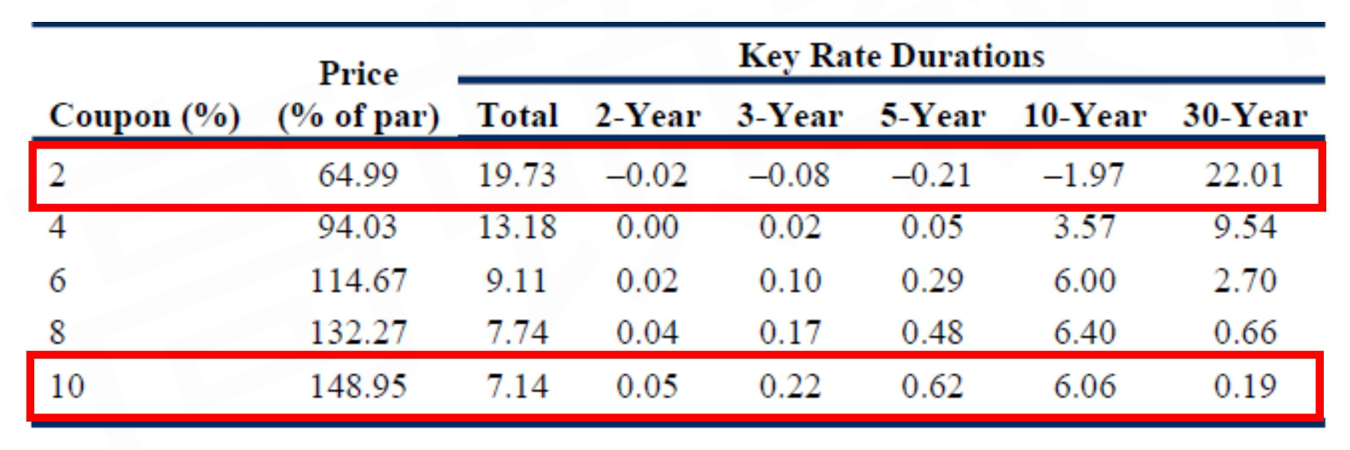

Example for Key Rate Durations of 30-Year Bonds Callable in 10Years Valued at a 4% Flat Yield Curve with 15% Interest Rate Volatility

For putable bonds

With high coupon rate

The putable bonds are unlikely to be put

Prices are most sensitive to their maturity-matched rates

As the bond's coupon decrease

So does the likelihood of the bond being put

price is most sensitive to the time-to-exercise rate

For zero-coupon bond or bond with a verylow coupon

Key rate durations can sometimes be negative for maturity points that are shorter than the maturity of the bond being analyzed

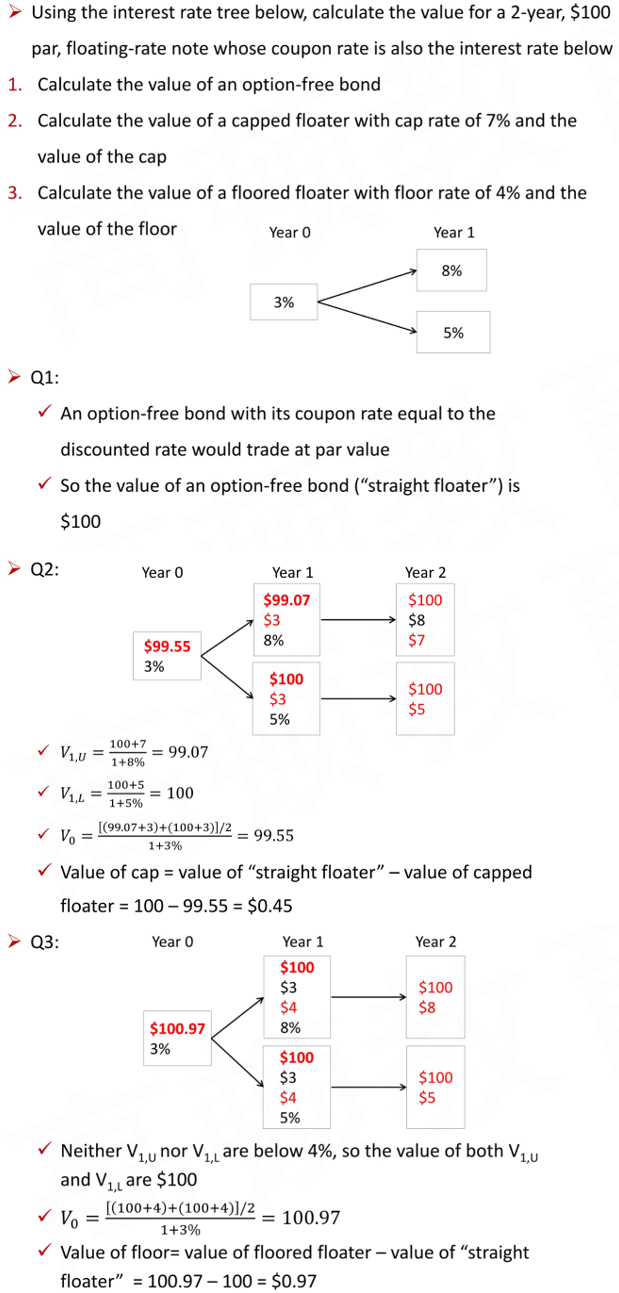

Capped or Floored Floating-Rate Bond

Definition and Application

Floating-Rate Bonds(Floaters)

The coupon rate is linked to an external reference rate, such as LIBOR

Coupon rate = reference rate + quoted margin

Reference rate reset periodically, typically quarterly

Quoted margin is usually constant

Coupon payments are in arrears: based on previous period's reference rate

Floater with Cap or Floor

Capped floating-rate bonds'coupon rate would not exceed the specified maximum rate (cap)

Floored floating-rate bonds' coupon rate would not fall below the specified minimum rate (floor)

A capped floaterprotects the issuer against rising interest rates and is thus an issuer option

The investor is long the bond but short the embedded "cap" option

Value of capped floating-rate bond = value of a "straight" floater - value of the embedded cap

Calculation of Floater with Cap or Floor

Similarly, capped and floored floaters can be valued by using the backward induction method in a binomial interest rate tree

We check whether the cap or floor applies at each node

If it does, the cash flow is adjusted accordingly

Example

Ratchet Bond

As with conventional floater, ratchet bond's coupon is reset periodically according to a formula based on a reference rate and a credit spread

Ratchet bonds are floating-rate bonds with both issuer and investor options

Ratchet bonds offer extreme protection as a capped floater protects the issuer against rising interest rates

At the time of reset, the coupon can only decline: it can never exceed the existing level

So, over time, the coupon "ratchets down"

At issuance, the coupon of a ratchet bond is much higher than that of a standard floater

Whenever a coupon is reset, the investor has the right to put the bonds back to the issuer at par

The embedded option is called a "contingent put", because the right to put is available to the investor only if the coupon is reset

Convertible Bond

Basic Concepts of Convertible Bond

Conversion ratio: the number of common shares that the bondholder receives from converting the bonds into shares

Conversion price = Issue price/ Conversion ratio

Typically, conversion bonds are issued at par value

Conversion ratio = Issue price/ Conversion price

Market conversion price: the price that investors effectively pay for the underlying common share if they buy the convertible bond and then convert it into shares

Market conversion price = Convertible bond price/ Conversion ratio

Market conversion premium ratio = Market conversion premium per share / Market share price

Conversion value: the value of the bond if it is converted to common shares

Conversion value = Market share price x Conversion ratio

Conversion ratio is fixed but the market share price is floating, so the conversion value is floating

Straight value: the value of the bond if it were not convertible

The PV of the cash flows

Minimum value is a floor value for the convertible bond at the greater of the conversion value or the straight value

Minimum value = Max(conversion value, straight value)

Analysis of Convertible Bond

Risk-Return Characteristics of Convertible Bond

Downside risk

Straight value can be used as a benchmark of the downside risk of a convertible bond Premium over straight value =(Convertible bond price / Straight price) - 1

Upside potential

Depends primarily on the prospects of the underlying common share

Influence of stock price

Stock price increases

Convertible bond will underperform

Reason: conversion premium

Stock price decreases

Returns on convertible bonds exceed those of the stock

Reason: The convertible bond's price has a floor value

Stock price remains stable

Returns on convertible bonds exceed those of the stock

Reason: The coupon payments received from the bond, assuming no change in interest rates or credit risk of the issuer

When the underlying share price is well below the conversion price, the convertible bond exhibits mostly bond risk-return characteristics

Straight value acts as a downside limit

Price of the common stock has little or no effect on the convertible's market price

When the underlying share price is well above the conversion price, the convertible bond exhibits mostly stock risk-return characteristics

In between these two extremes, the convertible bond trades like a hybrid instrument

Valuation Equivalence

The convertible bond can be valued as the equivalence of its component combination

Convertible bond = Straight bond + Call option on stock

Credit Analysis Models

Modeling Credit Risk

Loss Given Default

Expected loss = Probability of default x Loss given default

Loss given default(LGD) is the amount of loss if a default occurs

Loss given default(%) = 100% - Recovery rate

Loss given default($) = Expected exposure - Recovery($)

Recovery rate is percentage of the loss recovered from a bond in default

Expected exposure is the projected amount of money the investor could lose if an event of default occurs, before factoring in possible recovery

Probability of Default

Expected loss = Probability of default x Loss given default

Probability of default (POD) is the probability that the bond issuer will not meet its contractual obligations on schedule

Actual probability of default

The actual default probability for the corporate bond can observed from historical data

Risk-neutral probability of default

"Risk-neutral" follows the usage of the term in option pricing

In the risk-neutral option pricing methodology, the expected value for the payoffs is discounted using the risk-free interest rate

Usually, risk-neutral default probability is higher than actual default probability

The observed spread over the yield on a risk-free bond in practice also includes liquidity and tax considerations in addition to credit risk

The initial POD, which is called the hazard rate in statistics, is used to calculate the remaining PODs

Hazard rate is the conditional default rate, which means the default rate under the condition that no default happens before

Probability of survival(POS) is under the condition that no default happens before

Credit Valuation Adjustment

Fair value of corporate bond = VND - CVA

VND: the value for the corporate bond assuming no default

Credit valuation adjustment(CVA) is the value of the credit risk in present value term

CVA is the sum of PV of expected loss

Credit Spreads

Components of a Corporate Bond Yield

Benchmark Yield capture the macroeconomic factors affecting all debt securities

Expected real rate of return

Expected inflation rate

Risk aversion: compensation for uncertainty regarding expected inflation

Spread Over the Benchmark Yield capture the microeconomic factors that pertain to the corporate issuer and the specific issue itself

Expected loss from default

Liquidity

Taxation

Risk aversion: compensation for uncertainty regarding expected loss from default

Term Structure of Credit Spreads

Term structure of credit spreads is the curve that shows the spread over a benchmark security for an issuer for outstanding fixed-income securities with shorter to longer maturities

When a bond is very likely to default, it often trades close to its recovery value at various maturities

The credit spread curve is less informative about the relationship between credit risk and maturity

Key Drivers of the Term Structure of Credit Spreads

Credit quality

The credit term structure for highly rated securities tends to be either flat or slightly upward sloping

Securities with lower credit quality face greater sensitivity to the credit cycle

It results in a steeper credit spread curve or sometimes face a downward-sloping credit term structure

Financial conditions

A stronger economic climate is generally associated with lower credit spreads for issuers whose default probability declines

Market supply and demand dynamics

The credit curve will be most heavily influenced by the new and most frequently traded securities

Infrequently traded bonds trading with wider bid-offer spreads can also impact the shape of the term structure

Company-value model

These models take stock market valuation, equity volatility, and balance sheet information into account to derive the implied default probability for a company

For example, greater equity volatility will tend to drive a steeper credit spread curve

Appropriate risk-free or benchmark rates used to determine spreads

The duration and maturity of the most liquid or on-the-run government bonds rarely match that of corporate, so it is often necessary to interpolate

As the interpolation may impact the analysis for less-liquid maturities, the benchmark swap curve based on interbank rates is often substituted for the government

Term structure analysis should include only bonds with similar credit characteristics, which are typically senior unsecured general obligations of the issuer

Any bonds of the issuer with embedded options, first or second lien provisions, or other unique provisions should be excluded from the analysis

Sometimes securities typically include cross-default provisions,so that all securities across the maturity spectrum of a single issuer will be subject to recovery in the event of bankruptcy

Credit Analysis for Securitized Debt

ABS vs. Corporate Debt

In the case of a corporate bond, when the issuer defaults, the cash flows cease and there is a terminal cash flow

ABS do not default, but they can lose value as the SPE's pool of securitized assets incurs defaults

The credit risk metric of probability of loss is applied rather than probability of default

Credit Analysis for Securitized Debt

Granularity of the portfolio

A highly granular portfolio may have hundreds of underlying creditors, suggesting it is appropriate to draw conclusions about creditworthiness based on portfolio summary statistics rather than investigating each borrower

Alternatively, an asset pool with fewer discrete or non-granular investments would warrant analysis of each individual obligation

Homogeneity

Analyst might draw general conclusions about the nature of homogeneous obligations (eg. credit card or auto loan) given that an individual obligation faces strict eligibility criteria to be included in a specific asset pool

Heterogeneous leveraged loan, project finance, or real estate transactions require scrutiny on a loan-by-loan basis given their different characteristics

Investors are exposed to the ability of the servicer to effectively manage and service the portfolio over the life of the transaction

Structure of a collateralized or secured debt transaction is a critical factor in analyzing securitized debt

Bankruptcy remoteness can separate risk between the originator and SPE

Additional credit enhancements are a key structural element to be evaluated in the context of credit risk

Credit Analysis for Covered Bond

A covered bond is a senior debt obligation of a financial institution that gives recourse to the originator/issuer as well as a predetermined underlying collateral pool

The dual recourse双重还款源 to both the issuing financial institution as well as the underlying asset pool has been a hallmark of covered bonds

Credit Models

Credit Scores and Credit Ratings

Credit scoring ranks a borrower's credit riskiness

Provide an ordinal ranking of a borrower's credit risk

Do not tell the degree to which the credit risk differs among different ranks

Used for small businesses and individuals

The FICO(Fair Isaac Corporation) score is used in the United States by about 90% of lenders to retail customers

Five primary factors are included in the proprietary algorithm used to get the score:

35% for the payment history

30% for the debt burden

15% for the length of credit history

10% for the types of credit used

10% for recent searches for credit

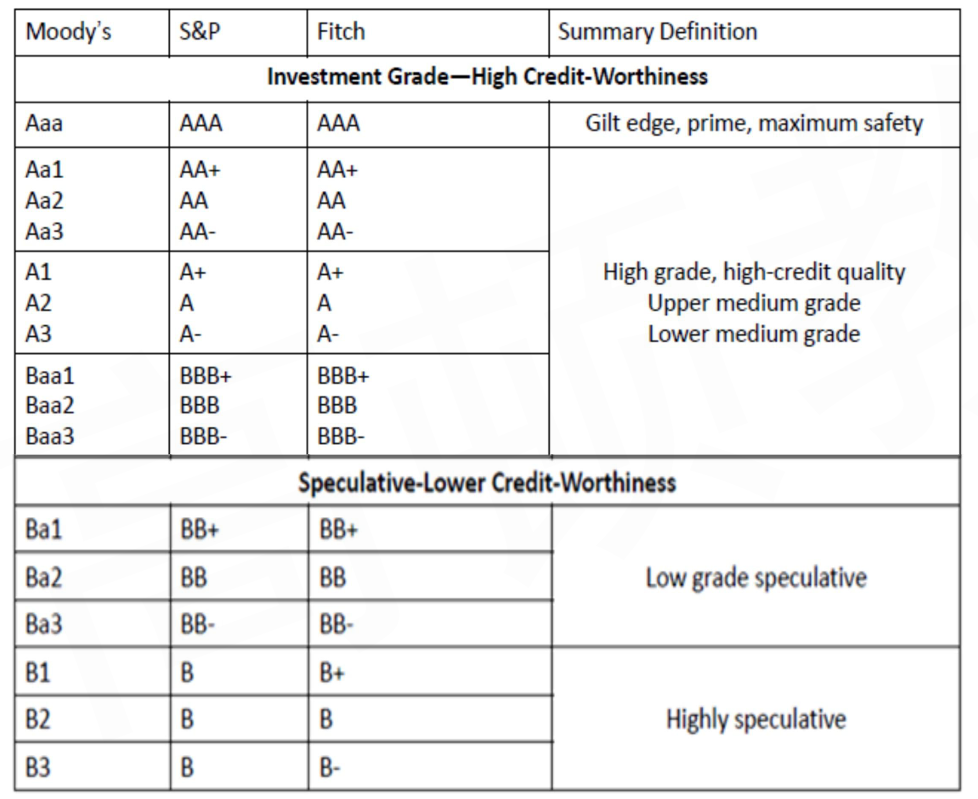

Credit ratings rank the credit risk of a company, government(sovereign),quasi-government,or ABS

Strengths of credit ratings

Provide a simple statistic

Tend to be stable over time, reducing debt market volatility

Weaknesses of credit ratings

The stability reduces the correspondence to a debt's default probability, and make the rating lag the market

Do not depend on business cycle, while default probability does

The issuer-pays model for compensating credit-rating agencies has a potential conflict of interest that may distort the accuracy of credit ratings

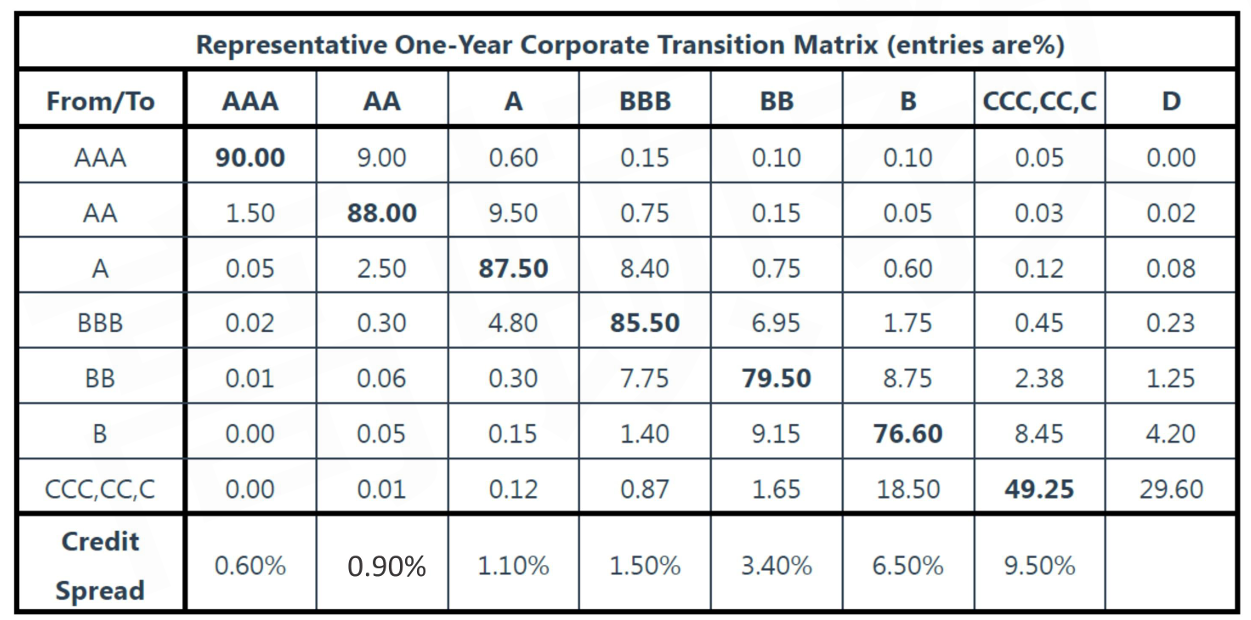

Credit Transition Matrix

Credit transition matrix shows the probabilities of a particular rating transitioning to another over the course of the following year

Structural Model

Assumptions of structural models

Company's assets(A) are traded in a frictionless arbitrage-free market

The company has a simple balance sheet structure with only one class of simple zero-coupon debtD(K,t)

The value of the company's assets has a lognormal distribution

The risk-free interest rate (r) is constant over time

The probability of default is endogenous内生的 (internal) to this structural model

Call Option Analogy

E_t=\max \left(A_t-K,0\right) Company's equity is economically equivalent to owning a European call option on the company's assets (A_t) with strike price K (face value of zero-coupon debt) and maturity t (maturity of debt)

D_t=A_t-\max \left(A_t-K,0\right)

Company's debt is economically equivalent to owning the company asset, and simultaneously selling a European call option on the assets (A_t) of the company with strike price K (face value of zero coupon debt) and maturity t

Put Option Analogy

D_t=K-\max \left(K-A_t,0\right)

Company's debt is economically equivalent to owning a riskless bond, and simultaneously selling a European put option on the assets (A_t) of the company with strike price K(face value of zero-coupon debt) and maturity t

Option Analogy for Debt

owning the company asset, and simultaneously selling a European call option on the assets

owning a riskless bond, and simultaneously selling a European put option on the assets

Strengths

It provides insight into the nature of credit risk

The company defaults when the value of its assets fall below the default barrier

Provide an option analogy for understanding a company's default probability and recovery rate

Can be estimated using only current market prices

Weaknesses

Model assumptions of simple balance sheet and traded assets are not realistic

Estimation procedures do not consider business cycle

Reduced-Form Model

Assumptions of reduced-form models

The company's zero-coupon bond trades in frictionless markets that are arbitrage free

Risk-free interest rate (r) is stochastic随机变量

Economy and recovery rate are stochastic

Probability of default is not constant and varies with the state of economy

Reduced-form models treating default as an exogenous (external) variable that occurs randomly

Under reduced form models, debt value can be computed as:

D_t=\tilde{E}\left(\frac{K}{\prod\left(1+r_i\right)}\right)

Strengths

Model inputs are observable, historical estimation procedures can be used

Credit risk allowed to fluctuate with business cycle

Do not require specification of the company's BS structure

Weaknesses

Do not explain the economic reasons for default

Unless the model has been formulated and back tested properly, the hazard rate estimation may not be valid

Credit Default Swaps

Structure and Features of CDS

Credit Derivative

Credit derivative is a derivative instrument in which the underlying is the credit quality of a borrower

Four types of credit derivative

Total return swaps

Credit spread options

Credit-linked notes

Credit default swaps(CDS)

Definition of CDS

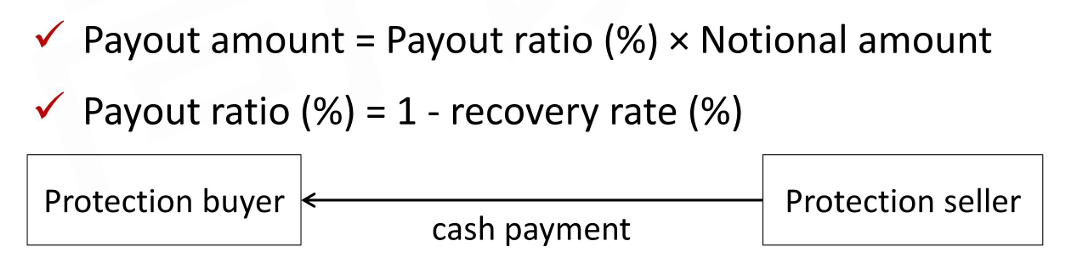

Credit default swaps (CDS) is a derivative contract between two parties, credit protection buyer and credit protection seller, in which the buyer makes a series of cash payments to the seller and receives a promise of compensation for credit losses resulting from the default (a pre-defined credit event) of a third party

Protection buyer / CDS buyer is the one who short CDS

Protection seller/ CDS seller is the one who long CDS

Fundamentals of CDS

CDS is essentially an insurance contract

Notional amount/principal保额 is the amount of protection being purchased

CDS spread(%)保费 is the premium that the buyer of a CDS pays to the seller for protection against credit risk

CDS spread is either paid upfront or over a period of time

Pricing of CDS Spread

The higher the probability of default, the higher the CDS spread

The higher the loss given default, the higher the CDS spread

Credit Events

Bankruptcy: allows the defaulting party to work with creditors under the supervision of the court so as to avoid full liquidation

Failure to pay: a borrower does not make a scheduled payment of principal or interest on any outstanding obligations after a grace period, without a formal bankruptcy filing

Restructuring: the issuer forces its creditors to accept terms that are different than those specified in the original issue.

Reduction or deferral of principal or interest

Change in seniority or priority of an obligation

Change in the currency in which principal or interest is scheduled to be paid

Settlement Protocols

Physical settlement: actual delivery of the debt instrument in exchange for a payment by the credit protection seller of the notional amount of the contract

Cash settlement: the credit protection seller pays cash to the credit protection buyer

Types of CDS

Single-Name CDS

Single-name CDS is a CDS on one specific borrower(reference entity)

Reference obligation is a particular debt instrument issued by the borrower that is the designated instrument being covered by CDS

The designated instrument is usually a senior unsecured obligation, but the reference obligation is not the only instrument covered by the CDS

Any debt obligation issued by the borrower that is pari passu(ranked equivalently in priority of claims) or higher relative to the reference obligation is covered

The payoff of the single-name CDS is determined by the cheapest-to-deliver obligation

Cheapest-to-deliver obligation is the debt instrument that can be purchased and delivered at the lowest cost but has the same or higher seniority as the reference obligation

Index CDS

Index CDS(CDX) is a CDS that allows participants to take positions on the credit risk of a combination of borrowers

The notional principle is the sum of the protection on all the borrowers

Credit correlation is a key determinant of the value of an index CDS

The more correlated the defaults, the more costly it is to purchase protection for a combination of the companies

Pricing of CDS

CDS Spread and Fixed Coupon

CDS spread(%) is the premium that the buyer of a CDS pays to the seller for protection against credit risk

Standardization in the market has led to a fixed coupon (CDS coupon rate) on CDS 1% for a CDS on an investment-grade company or index 5% for a CDS on a high-yield company or index

Upfront Payment

Upfront payment ($) = Total present values of protection leg - Total present values of premium leg

Premium leg: The series of payments the credit protection buyer promises to make to the credit protection seller

Protection leg: The contingent payment that the credit protection seller may have to make to the credit protection buyer

Upfront Premium

Upfront premium is the differential between the credit spread and the standard fixed coupon rate that converted to a present value basis

A credit spread more than the standard coupon rate will result in a cash upfront payment from the protection buyer to the seller

A credit spread less than the standard rate would result in a cash upfront payment from the protection seller to buyer

Upfront premium(%) ≈ (Credit spread - Fixed coupon) × Duration

Upfront premium (%) ≈ Total present values of credit spread - Total present values of fixed coupon

Credit spread ≈ Upfront premium / Duration + Fixed coupon

CDS Pricing Conventions

Price of CDS in currency per 100 par ≈ 100 - upfront premium(%)

Upfront premium(%)= 100 -Price of CDS in currency per 100 par

Profits of CDS

The value of a CDS may change if the credit quality of the reference entity or the credit risk premium in the overall market change

Monetizing a gain or loss: changes in the value of a CDS gives rise to opportunities to unwind the position

Profit(%) ≈ Change in spread(%) × Duration of CDS

Profit($) ≈ Change in spread(%) × Duration of CDS × Notional amount($)

Applications of CDS

A derivative instrument has two general uses

One is to exploit an expected movement in the underlying Managing credit exposure: Taking on or shedding of credit risk

The other trading opportunity is in valuation differences between the derivative and the underlying Valuation disparity: The focus is on differences in the pricing of credit risk in the CDS market relative to that of the underlying bonds

Managing Credit Exposure

Adjustment of credit exposure: increasing/decreasing credit exposure by selling/buying CDS if having assumed too little/much credit risk

Naked CDS: buying or selling credit protection without credit exposure to the reference entity

The buyer (seller) of a naked CDS is taking a position that the entity's credit quality will deteriorate (improve)

Long/short trade: taking a long position in one CDS and a short position in another

A bet that the credit position of one entity will improve relative to that of another

Managing Credit Exposure

Credit curve is the credit spreads for a range of maturities of a company's debt Upward-sloping credit curves imply a greater likelihood of default in later years, which are more common than downward-sloping curves

Curve trade: buying a CDS of one maturity and selling a CDS on the same reference entity with a different maturity

If an investor believes that the credit curve will become steeper, he can buy a long-term CDS and sell a short-term CDS

If an investor believes that the credit curve will become flatter,he can buy a short-term CDS and sell a long-term CDS

Valuation Disparity

Basis trade: exploit the difference of credit spread between bond market and CDS market

In principle, the amount of yield attributable to credit risk on the bond should be the same as the credit spread on a CDS

The general idea behind is that any such mispricing will disappear when the market recognizes the disparity

Another type of trade using CDS can occur within the instruments issued by a single entity

Arbitrage trade: buy the cheaper and sell the more expensive

If the cost of the index is not equivalent to the aggregate cost of the index components

If a synthetic CDO is not equivalent to the actual CDO Synthetic CDO is created by combining a portfolio of default-free securities with a combination of credit default swaps undertaken as protection sellers

i_{1, U}=i_{1, L} \times e^{2\sigma} \quad i_{2, U U}=i_{2, L U} \times e^{2\sigma} \quad i_{2, U U}=i_{2, L L} \times e^{4\sigma}

i_{1, U}=i_{1, L} \times e^{2\sigma} \quad i_{2, U U}=i_{2, L U} \times e^{2\sigma} \quad i_{2, U U}=i_{2, L L} \times e^{4\sigma}