Determining the value of an asset is at the heart of analysts professional activities and skill in valuation is a very important element of success in investing

Valuation is the estimation of an asset's value based on:

Variables perceived to be related to future investment returns

Or, on comparisons with similar assets

Or, on estimates of immediate liquidation proceeds

Intrinsic value is the value of the asset given a hypothetically complete understanding完全掌握资产的所有信息下的估值 of the asset's investment characteristics

Sources of Perceived Mispricing

There are two sources of perceived mispricing(V_E-P)

E(IV)-P=(IV-P)+(E(IV)-IV)

IV-P: true mispricing

E(IV)-IV: estimation error

The difference between the true (real) but unobservable intrinsic value and the observed market price contributes to the abnormal return or alpha which is the concern of active investment managers

Other Definitions of Value / Price

Fair market value (price) is the price at which a willing, informed, and able seller would trade an asset to a willing, informed, and able buyer

Investment value is the value to a specific buyer taking account of potential synergies and based on the investor's requirements and expectations

Intrinsic value is most relevant to public company valuation

Going-Concern and Liquidation

Going-concern value

The value under a going-concern持续经营 assumption that the company will continue its business activities into the foreseeable future

Liquidation value

The value if the company is dissolved and its assets sold individually

Orderly liquidation value assumes adequate time to realize liquidation value

Going-concern value > Liquidation value

Valuation Model Selecting

Valuation Models

Absolute valuation models

Models that specify an asset's intrinsic value which is in order to be compared with the asset's market price

It does not need consider about the value of other firms

Relative valuation models

Models that derive values from relative comparison to similar assets,based on law of one price

It is typically implemented using price multiples

For examples P/E_{stock} \lt P/E_{market} → stock is relatively undervalued

Models Selection

Consistent with characteristics of company

Understand the company and how its assets create value

Based on quality and availability of data

DDM problematic when no dividends

P/E problematic with highly volatile earnings

Consistent with purpose of analysis

Free cash flow vs. dividends for controlling interest

Common Adjustments for Valuation

The value of a stock investment that would give an investor a controlling position will generally reflect a control premium

The value of non-publicly traded stocks generally reflects a lack of marketability discount

Among publicly traded(i.e., marketable) stocks, the prices of shares with less depth to their markets (less liquidity) often reflect an illiquidity discount

The price that could be realized for that block of shares would generally be lower than the market price for a smaller amount of stock, a so-called blockage factor

Sum-of-the-Parts Value

Sum-of-the-parts value (breakup value, private market value) is the value for a company as a whole obtained by adding up the values of individual parts of the firm

Useful when valuing a company with segments in different industries that have different valuation characteristics

Frequently used to evaluate the value that might be unlocked in a restructuring through a spinoff, split-off, or equity (IPO) carve-out

Conglomerate Discount

Conglomerate discount多元化经营折价 refers to the concept that the market applies a discount to the stock of a company operating in multiple, unrelated businesses compared to the stock of companies with narrower focuses

Possible explanations for the conglomerate discount include:

Inefficiency of internal capital markets

Companies' allocation of investment capital among divisions does not maximize overall shareholder value

Endogenous factors

Poorly performing companies tend to expand by making acquisitions in unrelated businesses

Research measurement errors

Process of Valuation

Steps of Valuation Process

Understanding the business

Industry and competitive analysis

Analysis of financial reports

Considerations in using accounting information

Forecasting company performance

A top-down forecasting approach moves from international and national macroeconomic forecasts to industry forecasts and then to individual company and asset forecasts

A bottom-up forecasting approach aggregates forecasts at a micro level to larger scale forecasts

Selecting the appropriate valuation model

Converting forecasts to a valuation

Applying the valuation conclusion

Sell-side analysts associated with investment firms' brokerage operations are perhaps the most visible group of analysts offering valuation judgments

Buy-side analysts works in investment management firms,trusts and bank trust departments, and similar institutions, an analyst may report valuation judgments to a portfolio manager or to an investment committee as input to an investment decision

Applications of Equity Valuation

Selecting stocks

Inferring (extracting) market expectations

Evaluating corporate events

Rendering fairness opinions

Evaluating business strategies and models

Communicating with analysts and shareholders

Appraising private businesses

Share-based payment (compensation)

Contents of a Research Report

Contain timely information

Be written in clear, incisive language

Be objective and well researched, with key assumptions clearly identified

Distinguish clearly between facts and opinions

Present sufficient information to allow a reader to critique the valuation

State the key risk factors involved in an investment in the company

Disclose any potential conflicts of interests faced by the analyst

Discounted Dividend Valuation

Framework of Model

Models

DCF Model

{V}_0=\sum_{{i}=1}^{+\infty} \frac{{CF}_{{i}}}{(1+{r})^{{i}}}

An asset's intrinsic value is the present value of its expected future'cash flows'

DDM Model

V_0=\sum_{i=1}^{+\infty} \frac{D_i}{\left(1+r_e\right)^i}

DDM shows the intrinsic value to the investor is the present value of all future dividends discounted at required return of equity

DDM is from the perspective of non-controlling investors'judgment of stock's intrinsic value

Advantages and disadvantages of DDM

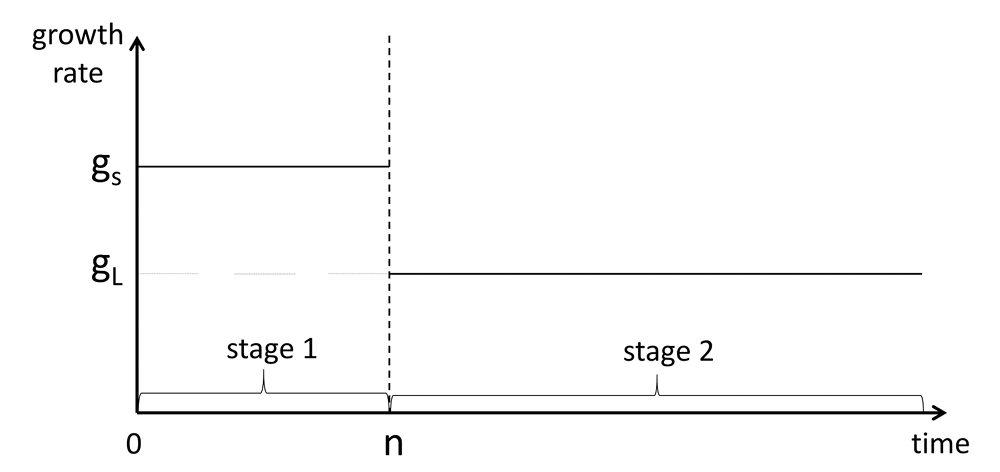

Infinite Stream

Forecast the stock price at a certain point in the future

V_0=\sum\frac{D_i}{(1+r)^i}+\frac{P_n}{(1+r)^n}

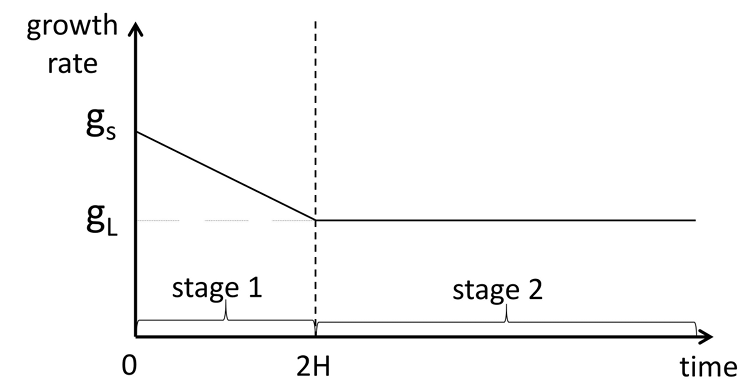

Future dividends can be forecast by assuming one of several stylized growth patterns

Constant growth forever(Gordon growth model)

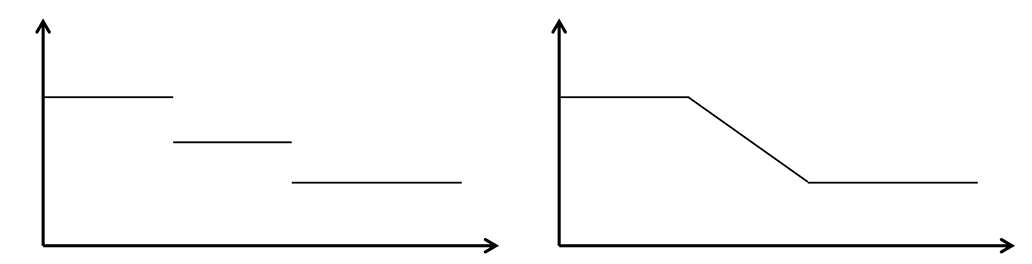

Two distinct stages of growth

Three (or more) distinct stages of growth

A finite number of dividends can be forecast individually up to a terminal point, then the terminal value is estimated

Forecasted value at beginning of the final mature growth phase

The terminal value is then discounted back, and added to the present value of prior stage dividends

Two methods are often used

Apply a price multiple to a projected terminal value of a fundamental such as P/E, P/B

Gordon growth model

Gordon Growth Model

Basic Concepts of GGM

Gordon Growth Mode

V_0=\frac{D_1}{r_e-g}

Assumptions of Gordon Growth Model

Dividends grow at constant rate (g) forever

Growth rate is less than required return (r_e \gt g)

Considerations of Using Gordon Growth Model

The GGM should reflect long-term growth expectations: GDP growth, industry life cycle stages and the impact of the five force model

The model's intrinsic values V_0 are very sensitive to the input variables for r_e and g Sensitivity analysis may be required to obtain a range of values rather than a specific point estimate of value

Gordon growth model can accurately value companies that are repurchasing shares when the analyst can appropriately adjust the dividend growth rate for the impact of share repurchases

Sustainable Growth Rate

SGR(g) is the sustainable growth rate in earnings and dividends if we assume:

Growth from internally generated sources (No new equity issued)

Some key financial ratios remain unchanged

SGR(g)= ROE × retention rate(b)

ROE is calculated using beginning-of-period shareholders' equity

The lower the earnings retention ratio, the lower the growth rate(dividend displacement of earnings)

PRAT model: SGR = Net Profit Margin × Total Asset Turnover × Financial Leverage × retention rate

Applications of GGM

Valuation of Preferred Stock

V_0=\frac{D_p}{r_p}

The discount rate or capitalization rate is often at a positive spread over the firms junior ranking debt yield

Justified P/E Ratio

The Gordon model can also be used to calculate a "justified (or fundamental)"price multiple

Justified leading P/E Ratio

\text{Justified leading P/E}=\frac{V_0}{E_1}=\frac{\frac{D_1}{r-g}}{E_1}=\frac{\frac{D_1}{E_1}}{r-g}=\frac{1-b}{r-g}

High growth followed by linearly declining followed by perpetual growth

Strengths

Ability to model many growth patterns

Solve for V, implied g, and implied r

Weaknesses

Require high-quality inputs (GIGO)

Model must be fully understood

Value estimates are sensitive to g and r

Model suitability is very important

Spreadsheet Modeling

In practice we can use spreadsheets to model any pattern of dividend growth

It can involve a great deal of information and can project different growth rates for differing periods

The reason for this is the inherent flexibility and computational accuracy of spreadsheet modeling.

Free Cash Flow Valuation

Basic Concepts of FCFs

Introduction of Free Cash Flows

Dividends are the cash flows actually paid to stockholders

Free cash flows(FCF) are the cash flows available for distribution after:

Fulfilling all obligations (operating expenses and taxes)

Without impacting on the future growth plans of the company (incremental working capital and fixed capital)

Strengths of FCFs

Used with firms that have no dividends

Functional model for assessing alternative financing policies

Rich framework provides additional detailed insights into company

Other measures such as EBIT, EBITDA, and CFO either double count or omit important cash flows

Limitations of FCFs

FCF may be negative due to large capital demands

Requires detailed understanding of accounting and FSA

Information may be not readily available or published

Free Cash Flows vs. Dividends

The logics behind the general valuation models are the same for both DDM and FCF models, but the numerator is different

FCFE could be either greater or less than dividends, but the same economic forces that lead to low (high) dividends lead to low (high) FCFE

Ownership perspective is very different between DDM and FCF model

FCFE model takes a control perspective and can be used in control perspective

DDM takes a minority perspective and can be used in valuing minority position in publicly traded shares

FCFF and FCFE

FCFF is the cash available to shareholders and bondholders after taxes,capital investment, and WC investment, pre-levered cash flow

FCFE is the cash available to equity holders after payments to and inflows from bondholders, post-leveraged cash flow

The two FCF approaches, indirect and direct, for valuing equity should theoretically yield the same estimates, if all inputs reflect identical assumptions

An analyst may prefer to use one approach rather than the other because of the characteristics of the company being valued

If the company's capital structure is relatively stable, using FCFE to value equity is more direct and simpler

The FCFF model is often chosen in two other cases:

Alevered company with negative FCFE

Alevered company with a changing capital structure

Calculations of FCFs

Calculating FCFF

Basic Formula

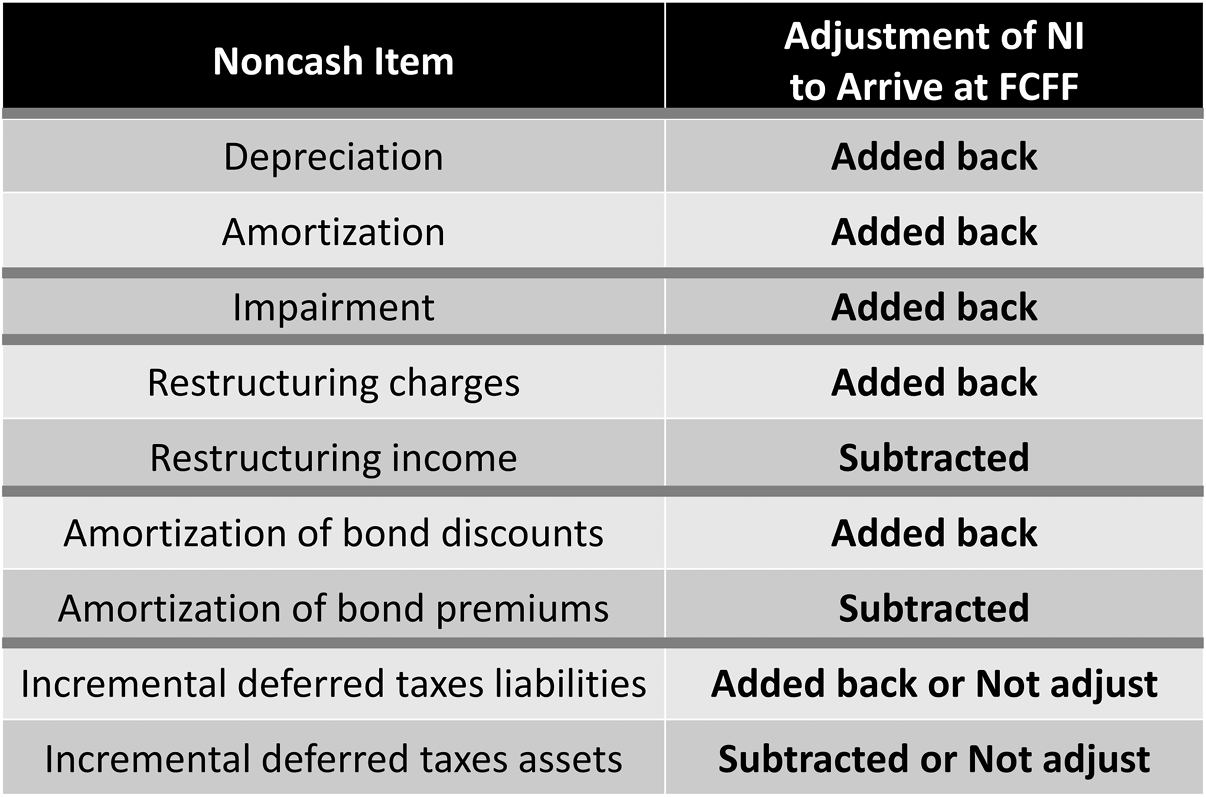

FCFF=EBIT\times(1-t)+NCC-WCInv-FCInv

NCC is non-cash charges, which represent an adjustment for noncash decreases and increases in net income

FCInv is net fixed capital investment, which equals to capital expenditure less proceeds from sales

WCInv is working capital investment excluding cash and short-term debt (notes payable and current portion of long-term debt)

Expanding Formulas

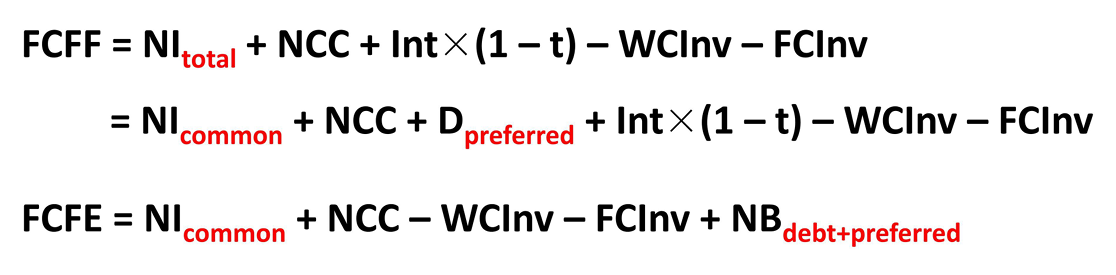

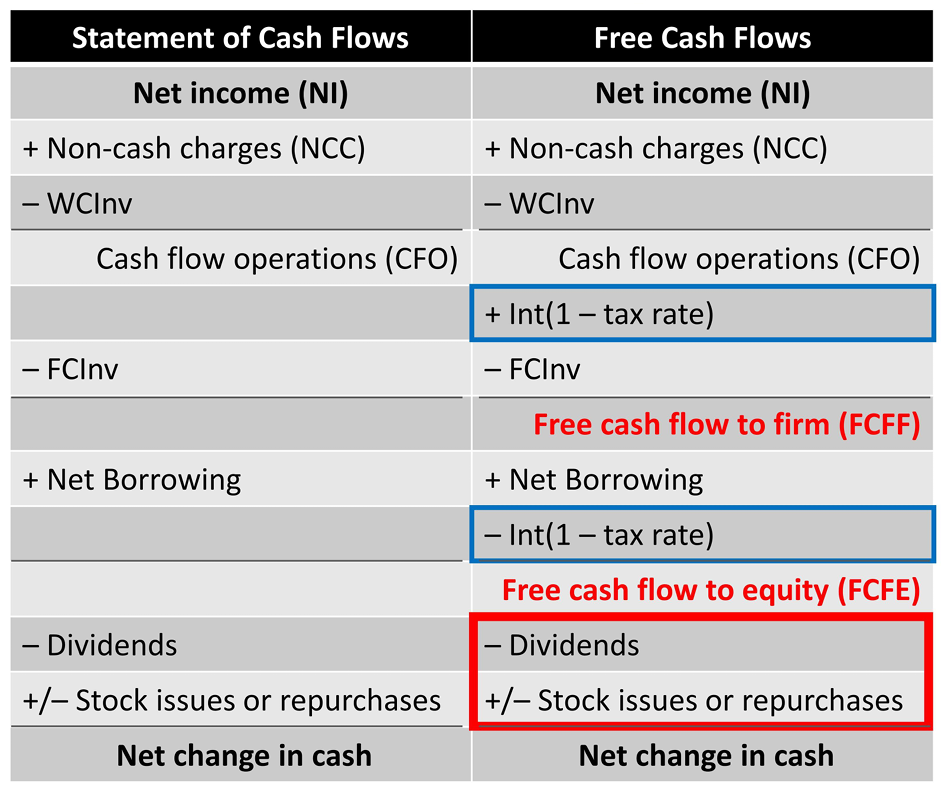

FCFF= NI+NCC+Int\times(1-t)-WCInv-FCInv

FCFF=EBITDA\times(1-t)+NCC\times t-WCInv-FCInv

FCFF=CFO+Int\times(1-t)-FCInv

Calculating FCFE

Basic Formula

FCFE=FCFF-Int \times(1-t)+NB

NB is net borrowings, which is debt issued less debt repaid over the period for which one is calculating free cash flow

NI is a Poor Proxy for FCFE

NI is a cash flow concept

NI recognizes non-cash charges such as depreciation, amortization

NI fails to recognize the cash flow impact of investments in working capital and net fixed assets, and net borrowings

EBITDA is a Poor Proxy for FCFE

EBITDA does not reflect taxes paid

EBlTDA ignores effect of depreciation tax shield

EBITDA does not account for needed investments in working capital and net fixed assets for going concern viability

EBlTDA is a pre-levered figure so it is pre-interest and before net borrowings

More Details About the Parameters

Non-Cash Charges

Working Capital Investments

Net investment in working capital for the purpose of calculating FCF excludes

Changes in cash and cash equivalents

Notes payable

Current portion of L.T.debt

There is an inverse (direct) relationship between changes in current assets (current liabilities) and changes in free cash flows

Fixed Capital Investments

Fixed capital investment (FCInv) represent a cash out flow necessary to support the company's current and future operations

Expenditures can include acquisition of intangible items such as trademarks

Care should be used with non-recurring large acquisitions in forecasts

Fixed capital investment is a net amount

It is equal to the difference between capital expenditures (investments in long-term fixed assets) and the proceeds from the sale of long-term assets

If there were no disposals of fixed assets

Given gross PP&E: FCInv= GV_{ending}-GV_{beginning}

Given net PP&E: FCInv = BV_{ending}- BV_{beginning} + \text{depreciation expense}

If there were disposals of fixed assets

Given gross PP&E: FCInv_{disposals}=FCInv +\text{AD of disposed assets}-\text{P/L from disposals}

Given net PP&E: FCInv_{disposals}=FCInv - \text{P/L from disposals}

Adjust FCFF if there were disposals of fixed assets

Calculate "FCInv = CAPEX - proceeds from disposal", Subtract P/L from disposals from NI

Net Borrowing

Net borrowings only affect FCFE, they do not affect FCFF

Notes payable

Increase in notes payable, add to FCFE

Decrease in notes payable, subtract from FCFE

Current portion of long-term debt

Increase in short-term debt, add to FCFE

Decrease in short-term debt, subtract from FCFE

Long-term debt

Add debt issuances to net income to arrive at FCFE

Subtract debt repurchases from net income to arrive at FCFE

Free Cash Flows with Preferred Stocks

For the most part, the discussion of FCFF and FCFE so far has assumed the company has a simple capital structure with two sources of capital, namely, debt and equity

Including preferred stock as a third source of capital requires the analyst to account for the dividends paid on preferred stock and for the issuance or repurchase of preferred shares

Usages of FCFs

Interesting Contrasts

Effects of Changing Leverage

An increase in leverage will not affect FCFF

Changing leverage (i.e. changing the amount of debt financing in the company's capital structure), does have some effects on FCFE particularly

An increase in leverage affects FCFE in two ways

In the year the debt is issued, it increases FCFE by the amount of debt issued

After the debt is issued, FCFE is then reduced by the after-tax interest expense

Estimations of FCFs

Approach one: forecast overall growth rate of FCFs

Calculate historical FCF

Estimate FCF for current period

Apply a constant growth rate to current FCF: FCF\times(1+g)^n

Usually, g_{FCFF}\ne g_{FCFE}

Approach two: forecast components of FCFs

Forecast each underlying component of FCFs

NI, NCC, FCInv and WCInv are tied to sales forecast

More realistic and flexible, but time consuming

Approach three: sales-based forecasting method

Investment in fixed capital in excess of depreciation (FCInv- Dep) and investment in working capital (WCInv) both bear a constant relationship to forecast increases in the size of the company as measured by increases in sales \frac{FCInv-Dep}{\Delta Sales} and \frac{WCInv}{\Delta Sales} will keep constant

Optimal capital structure represented by the debt ratio (DR) is constant DR=\frac{D}{D+E} will keep constant

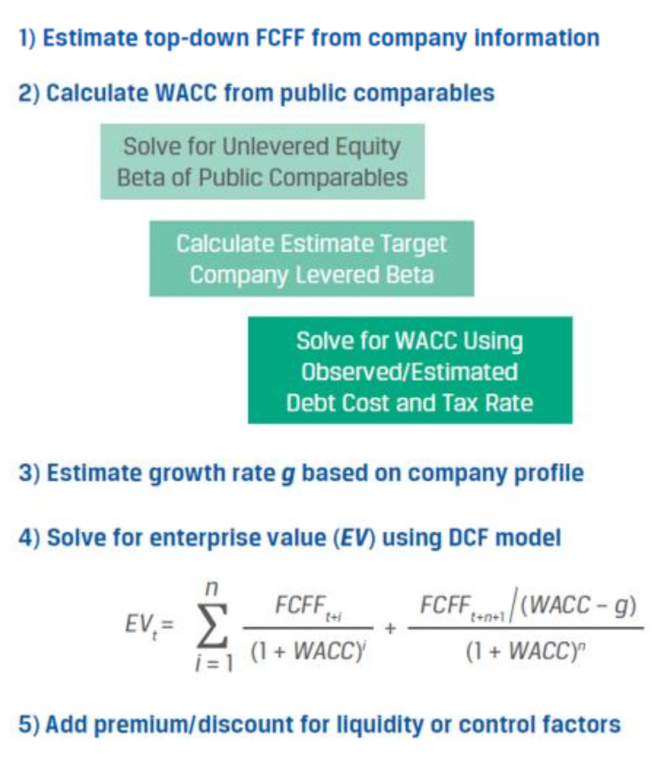

Use FCFF when high or changing debt levels, negative FCFE

Single-stage, two or more stages?

Single-stage model for income stock(slow and constant growth)

More-stage models for whose competitive advantage will disappear over time

Total FCF or components of FCF?

Terminal value via GGM or Multiples?

Nominal or real?

International setting or volatile inflation rates: use real rates

Total value or value of the operating assets?

Free cash flow valuation focuses on the value of assets that generate operating cash flows

If a company has significant non-operating assets, such as excess cash, excess marketable securities, or land held for investment, then analysts often calculate the value of the firm as the value of its operating assets (as estimated by FCFF valuation) plus the value of its nonoperating assets

Sensitivity Analysis

Apply sensitivity to each of the following variables:

The base-year value for the FCFF or FCFE

Future growth rate

Risk factors: beta, risk free rate and ERP

Relationship between discount rate and the growth rate is critical In general

Most sensitive: Beta and growth rate of FCF

Less sensitive: r_f, and FCF.

Market-Based Valuation

Basic Concepts of Multiples

Introduction of Multiples

Price multiples are ratios of a stock's market price to some measure of fundamental value per share

The intuition is that investors evaluate the price of a stock by considering what a share buys in terms of per share earnings,net assets, cash flow, or some other measure of value

Enterprise value multiples relate the total market value of all sources of a company's capital to a measure of fundamental value for the entire company

Relative Valuation Method

The method of comparables (i.e. relative valuation method)involves using a multiple to evaluate whether an asset is relatively fairly valued, relatively undervalued, or relatively overvalued in relation to a benchmark value of the multiple

Choices for the benchmark include:

A closely matched individual stock

The average for peer group of companies or industry

Own history

The economic rationale for the methods of comparable is law of one price

Cross Border Valuation Differences

Comparing companies across borders frequently involves accounting method differences, cultural differences,economic differences, and resulting differences in risk and growth opportunities

For example, P/E ratios for individual companies in the same industry across borders have been found to vary widely

Justified Price Multiples

A justified price multiple (also called warranted price multiple or intrinsic price multiple) for the stock is the estimated fair value of multiples

Justified price multiples can be justified on the basis of 1) method of comparables or 2) method of forecasted fundamentals

Comparison

If actual price multiple = justified price multiple, then be properly valued

If actual price multiple < justified price multiple, then be undervalued

If actual price multiple > justified price multiple, then be overvalued

The method is based on forecasted fundamentals relates multiples to company fundamentals (growth, risk, payout) through DCF model, and may permit the analyst to explicitly examine how valuations differ across stocks and against a benchmark given different expectations for growth and risk

Price Multiples

PE ratio

Rationale and Drawbacks of PE ratio

Rationale for Using P/E Ratio

Earnings power is a chief driver of investment value

P/E ratio is widely recognized and used by investors

Differences in stock's P/Es may be related to differences in long-run average returns on investments in those stocks, according to empirical research

Potential Drawbacks of P/E Ratio

Negative and very low earnings make P/E useless

Volatile or transitory earnings make interpretation difficult

Management discretion on accounting choices can distort earnings

Solely using the ratio avoids addressing the fundamentals (growth, risk, and cash flows)

Trailing and Leading P/E Ratio

Trailing P/E_0 (a.k.a. current P/E), is stock's current market price divided by the last four quarters (or past 12 months) EPS

In such calculations, EPS is sometimes referred to as "trailing 12 month (TTM) EPS"

Leading P/E_1 (a.k.a. forward P/E or prospective P/E), is stock's current market price divided by next year's expected EPS

Analysts interpreted "next year's expected earnings" as expected EPS for:

next four quarters

next 12 months (NTM P/E)

next fiscal year

Problems with Trailing P/E Ratio

Transitory and non-recurring components of earnings are company-specific

Non-recurring earnings are needed to be removed because valuation focus on future cash flows, so we calculate underlying earnings (persistent earnings, continuing earnings, or core earnings)

Non-recurring items to remove include: Gains/losses on asset sales; Asset write-downs for impairment; Loss provisions; Changes in accounting estimates

Cyclicality components of earnings due to business or industry trends

The countercyclical property of P/E (Molodovsky Effect)

Analysts should calculate normalized EPS to remove cyclical component of earnings and capture mid-cycle earnings under normal market conditions

Differences in accounting methods

Potentialdilution of EPS

Normalized Earnings

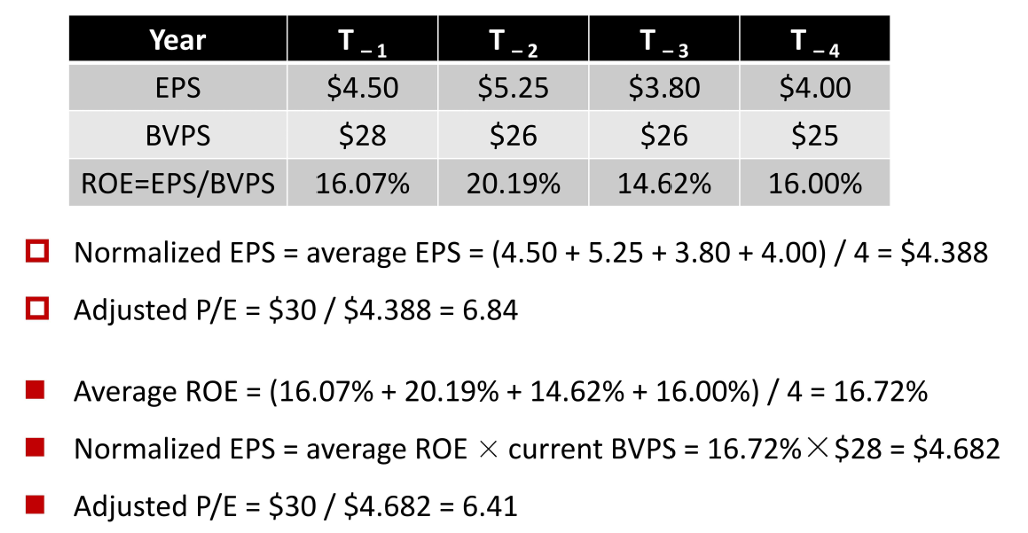

Method 1: historical average EPS

Normalized EPS is the average EPS over the most recent full cycle

Method 2: average ROE

Normalized EPS is the average ROE from the most recent full cycle multiplied by current book value per share

Method 2 is preferred since it more accurately reflects the effect of growth in company size on EPS

Example

Justified P/E Ratio

Fundamental factors affecting justified P/E ratio

Justified P/E positively related to growth rate and payout ratio, "all else equal"

Justified P/E inversely related to required return (real rate, inflation and equity risk premium), "all else equal"

Terminal Value Estimation

Terminal value is the intrinsic value projected at end of estimation horizon

Using fundamentals: Requires estimates of g, r, and payout

Using comparables: Uses market data to calculate benchmark

Predicted P/E from Regression

The P/E ratios may be regressed against the stock and company characteristics

The estimated equation exhibits the relationship between P/E and stock's characteristics

Positive coefficient with growth rate and payout ratio

Negative coefficient with beta

Limitations of regression

The method captures valuation relationships only for the sample of stock over a particular time period, and the predictive power of the regression for a different stock and different time period is not know

The relationship between P/E and fundamentals may change over time

Multicollinearity(correlation within linear combinations of the independent variables)

P/E-to-Growth[PEG] Ratio

PEG ratio is calculated as the stock's P/E divided by the expected earnings growth rate (in percentage terms)

PEG ratio is a calculation of a stock's P/E per percentage point of expected growth

Stocks with lower PEGs are more attractive than stocks with higher PEGs, all else being equal

PEG is useful but must be used with care for several reasons

PEG assumes a linear relationship between P/E and growth rate

The model for P/E in terms of the DDM shows that, in theory, the relationship is not linear

PEG does not factor in differences in risk, an important determinant of P/E

= PEG does not account for differences in the duration of growth

For example, dividing P/Es by short-term growth forecasts may not capture differences in long-term growth prospects

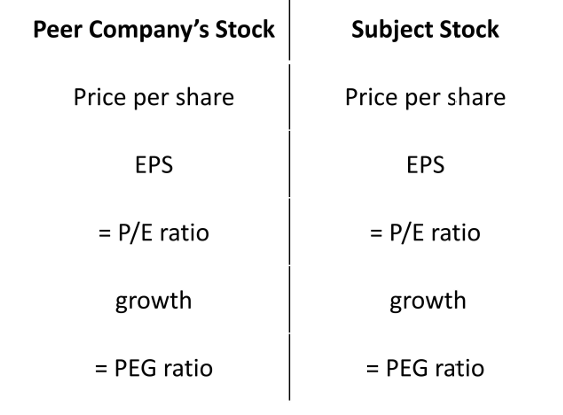

Valuation Based on Comparables

Peer company multiples

The subject stock's P/E is compared with the median or mean P/E for the peer group to arrive at a relative valuation

Are observed differences between P/E ratios explained by underlying determinants of P/E?

If not, asset may be mispriced

Industry and sector multiples

Using industry and sector data can help an analyst explore whether the peer-group comparison assets are themselves appropriately priced

Own historical P/E

Analyst shall be alert to the impact on P/E levels of changes in a company's business mix and leverage overtime

Changes in the interest rate environment and economic fundamentals over different time period can be another limitations

Overall Market Multiples

The question of whether the overall market is fairly priced has captured analyst interest throughout the entire history of investing

Fed Model

The stock market is to be overvalued when the stock market's current earnings yield is less than the 10-year Treasury bond (T-bond) yield

Fed Model uses expected earnings for the next 12 months in calculating the ratio

Yardeni Model

Yardeni obtained the following expression for the justified P/E on the market

\frac{P}{E}=\frac{1}{C B Y-b \times L T E G}

CBY is current Moody's Investors Service A-rated corporate bond yield LTEG is the consensus five-year earnings growth rate forecast for market index b measures the weight the market gives to five-year earnings projections

Higher current corporate bond yield imply a lower justified P/E

Higher expected long-term growth results in a higher justified P/E

Earnings Yield and Dividend Yield

Ranking Stocks by P/E Ratio

Stock selection disciplines that use P/E ratios often involve ranking stocks

The security with the lowest positive P/E has the lowest purchase cost per currency unit of earnings among the securities ranked

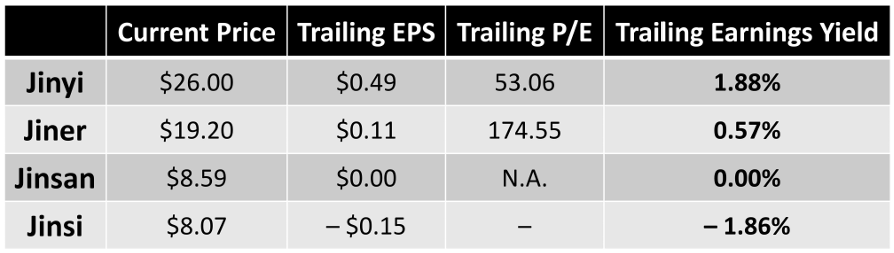

Zero earnings and negative earnings pose a problem if the analyst wishes to use P/E as the valuation metric

Because division by zero is undefined, P/Es cannot be calculated for zero earnings

A "negative P/E security" will rank below the lowest positive P/E security, but the negative earning security is actually the most costly in terms of earnings purchased

Earnings Yield

If the analyst is interested in a ranking, however, one solution is the use of reciprocal of the original ratio, which places"price" in the denominator

In the case of the P/E, the inverse price ratio is earnings yield

Ranked by earnings yield from highest to lowest, the securities are correctly ranked from cheapest to most costly

In addition to zero and negative earnings, extremely low earnings can pose problems when using P/Es, particularly for evaluating the distribution of P/Es of a group of stocks under review. In this case, inverse price ratios can be useful

An extremely high P/E (an outlier P/E) can overwhelm the effect of the other P/Es in the calculation of the mean P/E

Although the use of median P/Es and other techniques can mitigate the problem of skewness caused by outliers, the distribution of inverse price ratios (earnings yield) is inherently less susceptible to outlier-induced skewness

Dividend Yield

Rationales for using dividend yield(D/P)

Dividend yield is a component of total return

Dividends are a less risky component of total return than capital appreciation

Drawbacks for using dividend yield(D/P)

Dividend yield is just one component of total return

Dividends paid now displace earnings in all future periods (dividend displacement of earnings)

Trailing dividend yield and Leading dividend yield

Trailing dividend yield is the dividend rate (annualized amount of the most recent dividend) divided by the current market price

Leading dividend yield is the forecasted dividends over the next year divided by the current market price

Justified Dividend Yield

Justified leading dividend yield

\frac{D_1}{V_0}=\frac{D_1}{\frac{D_1}{r-g}}=r-g

An analyst can generally use P/B when EPS is zero or negative

BVPS is usually positive

P/B maybe more meaningful than P/E when EPS is abnormally high or low or is highly variable

Book value of equity is more stable than EPS

BVPS has been viewed as appropriate for valuing companies composed chiefly of liquid assets, such as finance, investment,insurance, and banking institutions

Book value has also been used in the valuation of companies that are not expected to continue as a going concern

Potential Drawbacks for Using P/B Ratio

Does not reflect value of intangible assets, off-B/S assets(e.g., human capital)

Misleading when comparing firms with significant differences in asset size

Different accounting conventions obscure comparability (particularly international)

Inflation and technological change can cause big differences between BV and MV

Share repurchase and issuances may distort historical comparison

Adjustments to P/B Ratio

To make the book value more accurately reflect the value of shareholders' investment or to make P/B more comparable among different stocks

May calculate tangible book value per share

Certain adjustments may be appropriate for enhancing comparability

For example, restate the book value of the company using LIFO

The balance sheet should be adjusted for significant off-balance items

Justified P/B Ratio

Formula

\begin{aligned} \text { Justified P/B ratio } & =\frac{V_0}{B V\left(E_0\right)}=\frac{\frac{D_1}{r-g}}{B V\left(E_0\right)}=\frac{\frac{D_1}{B V\left(E_0\right)}}{r-g}=\frac{\frac{N I_1\times(1-b)}{B V\left(E_0\right)}}{r-g} \\ & =\frac{R O E \times(1-b)}{r-g}=\frac{R O E-R O E \times b}{r-g}=\frac{R O E-g}{r-g}\end{aligned}

Fundamental factor affecting P/B ratio

Spread between ROE and r increases → value creation → higher market value

P/B increases as ROE increases

P/B increases as g increases

P/B increases as r decreases

(falling risk, interest rates, inflation and beta)

P/S Ratio

Rationales for Using P/S Ratio

P/S is useful for distressed firms

Sales revenue is often positive

Sales are generally more stable and less prone to distortion than EPS over time

P/S is useful for mature, cyclical, and zero-income stocks

Differences in P/S ratios may be related to difference in long-run average returns

Potential Drawbacks for Using P/S Ratio

High sales growth does not translate to operating profitability

P/S ratio does not capture different cost structures between firms

Revenue recognition methods can distort reported sales and forecasts

Adjusted CFO

Adjustments to CFO for components not expected to persist into future time periods

Adjustments to CFO may be required when comparing companies that use different accounting standards.

EBITDA

FCFE may be a cash flow concept with the strongest link to valuation theory

Rationales for Using P/CF Ratio

It is more difficult to manipulate CF than EPS

Cash flow is more stable than earnings

Addresses quality of earnings problem

Differences in P/CFs may explain differences in long-run average returns

Potential Drawbacks for Using P/CF Ratio

Earnings plus non-cash charges approach ignores some cash flows such as net fixed investments, working capital investment and net borrowings

FCFE is preferable to CFO, but FCFE more volatile and more difficult to compute, and can be negative with large CapEx

Some companies have increased their use of accounting methods that enhances cash flow measures

Operating cash flows under IFRS may not be comparable to operating cash flow under US GAAP

Enterprise Value Multiples

Enterprise value to EBITDA

Enterprise value multiple provides an indication of company/firm value, not equity value

Enterprise value to EBITDA (EV/EBITDA) is by far the most widely used enterprise value multiple

Because the numerator is enterprise value, EV/EBITDA is a valuation indicator for the overall company rather than common stock

EBITDA is a earnings flow to both debt and equity holders

Rationales for using EV/EBITDA ratio

Appropriate for comparing firms with different financial leverage since EBITDA is pre-interest

Controls for depreciation/amortization differences among businesses

EBITDA usually positive when EPS is negative

Potential drawbacks for using EV/EBITDA ratio

lgnores changes in working capital investments

FCFF (which controls for capital expenditures) is more closely tied to value

Enterprise Value

Enterprise Value(EV) = MV of common stock + MV of preferred stock + MV of debt - cash and cash equivalents - short-term investments

Cash and investment are subtracted because EV is designed to measure the net price an acquirer would pay for the company

Total invested capital(TIC) (a.k.a. market value of invested capital) is an another measure of total firm value, that is an alternative to enterprise value

Total invested capital(TIC) = MVof common stock + MVof preferred stock + MV of debt

Valuation Based on Forecasted Fundamentals

As with other multiples, intuition about the fundamental drivers of enterprise value to EBITDA can help when applying the method of comparables

All else being equal, the justified EV/EBITDA based on fundamentals should be

Positively related to the expected growth rate in free cash flow to the firm

Negatively related to the business's weighted average cost of capital

Positively related to expected profitability as measured by return on invested capital

ROIC is the relevant measure of profitability because EBITDA flows to all providers of capital

Other Enterprise Value Multiples

EV/FCFF

EV/EBITDAR(where R stands for rent expense)

It is favored by airline industry analysts

Enterprise value-to-sales(EV/S)

Price-to-sales ratio has the conceptual weakness that some of the proceeds from the company's sales will be used to pay interest and principal to the providers of the company's debt capital

A P/S for a company with little or no debt would not be comparable to a P/S for a company that is largely financed with debt, however EV/S would be the basis for a valid comparison in such a case

Momentum valuation indicators

Momentum Valuation Indicators

Momentum indicators are the valuation indicators that relate either price or a fundamental to the time series of their own past values

Momentum investment strategies

Buy winners, sell losers

Contrary investment strategies

Buy losers, sell winners

Unexpected Earnings

Unexpected earnings (also referred to as earnings surprise) is the difference between reported EPS and expected EPS

\mathrm{U E}_\mathrm{t}=\mathrm{E P S}_\mathrm{t}-\mathrm{E}\left(\mathrm{E P S}_\mathrm{t}\right)

The rationale is that positive surprise may be associated with persistent positive abnormal return,or alpha

Another momentum indicator based on the relative change in earnings per share is called standardized unexpected earnings

\mathrm{SUE}_{\mathrm{t}}=\frac{\mathrm{EPS}_{\mathrm{t}}-\mathrm{E}\left(\mathrm{EPS}_{\mathrm{t}}\right)}{\sigma_{\left[\mathrm{EPS}_{\mathrm{t}}-\mathrm{E}\left(\mathrm{EPS}_{\mathrm{t}}\right)\right]}}

Relative Strength Indicators

Relative strength indicators compare a stock's performance during a period 1) to its own past performance or 2) to the performance of some group of stocks

The simplest relative strength indicator of the first type is the stock's compound rate of return over some specified time

A simple relative strength indicator of the second type is the stock's performance divided by the performance of an equity index

This indicator maybe scaled to one at the beginning of the study period and if the stock goes up quickly (slowly) than the index, then relative strength will be above (below) one

Central tendency

Measuring Central Tendency in Multiples

Arithmetic mean

Most affected by outliers

Median

Least affected by outliers

Harmonic mean

Less affected by large outliers, more affected by small outliers

Weighted harmonic mean

Effect of outliers depend on market value weight

Harmonic mean

X_H=\frac{n}{\sum_{i=1}^n \frac{1}{X_i}}

Less weight on higher ratios

Reduces impact of large outliers

More weight on lower ratios

The harmonic mean may aggravate the impact of small outliers,but such outliers are bounded by zero on the downside

Lower value than arithmetic mean

Unless all observations are the same value

Used when market weight information unavailable

Weighted Harmonic Mean

X_{WH}=\frac{n}{\sum_{i=1}^n \frac{w_i}{X_i}}

Similar to simple harmonic mean except in weighting

Uses market value weights

Corresponds to portfolio value and can reflect the true "average P/E"(e.g., total price/total earnings)

Residual Income Valuation

Concepts of Residua Income

Introduction of Residual Income

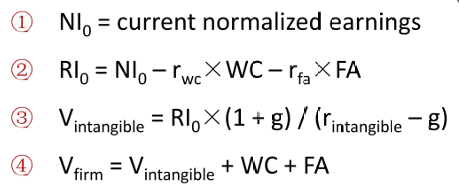

Residual income (RI) is net income less a charge (deduction) for shareholders' opportunity cost

Residual income explicitly deducts all capital costs of both debt and equity, so it is the "residual or remaining income" after considering the costs of all of a company's capital

Residual income has sometimes been called "economic profit"

The cost of equity(r_e) is the marginal cost of equity, because it represents the cost of additional equity

It is also referred to as the required rate of return on equity

Introduction of Residual Income Models

The appeal of residual income models stems from a shortcoming of traditional accounting

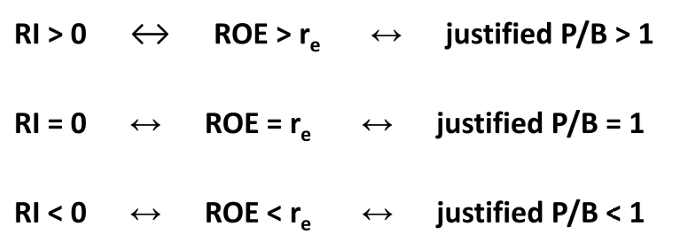

A company that is generating more income than its cost of obtaining capital (that is, one with positive residual income) is creating value

In forecasting future residual income, the term "abnormal earnings" is also used

In the long term, companies that earn more (less) than the cost of capital should sell for more (less) than book value

Formula to Calculate RI

Basic Formula

R I_t=N I_t-B V\left(E_{t-1}\right) \times r_e

R I_t=B V\left(E_{t-1}\right) \times\left(R O E_t-r_e\right)

Alternative Formula

\mathrm{RI}_{\mathrm{t}} =\text { NOPAT }_{\mathrm{t}}-\text { total capital charge }_{\mathrm{t}} =\text { EBIT }_{\mathrm{t}} \times(1-\text { tax rate })-\left(\text { cost of debt capital }_{\mathrm{t}}+\text { cost of equity capital }_{\mathrm{t}}\right)

Violations of clean surplus relationship occur when items bypass the income statement and direct adjustments to equity are made

Examples for considerations

Unrealized changes in the fair value of some financial instruments

Foreign currency translation adjustments

Certain pension adjustments

Portion of gains and losses on certain hedging instruments

Changes in revaluation surplus related to property, plant, and equipment or intangible assets (applicable under IFRS but not under US GAAP)

For certain categories of liabilities, change in fair value attributable to changes in the liability's credit risk(applicable under IFRS but not under US GAAP)

Balance Sheet Adjustments for Fair Value

To have a reliable measure of book value of equity, an analyst should identify and scrutinize significant off-balance-sheet assets and liabilities

Additionally, reported assets and liabilities should be adjusted to fair value when possible

Examples for considerations

Inventory

Deferred tax assets and liabilities

Operating leases

Reserves and allowances

Intangible Items

Intangible items require special consideration because they are often not recognized as an asset unless they are obtained in an acquisition

For example, advertising expenditures can create a highly valuable brand, but they are shown as an expense, and the value of a brand would not appear as an asset on the financial statements unless the company owning the brand was acquired

Research and development(R&D) costs provide another example of an intangible asset that must be given careful consideration

If a company engages in unproductive R&D expenditures, these will lower residual income through the expenditures made

If a company engages in productive R&D expenditures, these should result in higher revenues to offset the expenditures over time

Nonrecurring Items

Companies often report nonrecurring charges as part of earnings, which can lead to overestimates and underestimates of future residual earnings if no adjustments are made

Example for considerations

Unusual items

Extraordinary items

Restructuring charges

Discontinued

Accounting changes

Other Aggressive Accounting Practices

Companies may engage in accounting practices that result in the overstatement of assets (book value) and/or overstatement of earnings

Other activities that a company may engage in include accelerating revenues to the current period or deferring expenses to a later period

Conversely, companies have also been criticized for the use of "cookie jar" reserves (reserves saved for future use), in which excess losses or expenses are recorded in an earlier period

Accounting Issues-International Considerations

Accounting standards differ internationally and these differences result in different measures of book value and earnings internationally

It suggests that valuation models based on accrual accounting data might not perform as well as other valuation models in international contexts

Commercial implementations

Economic Value Added

Economic value added(EVA) = NOPAT - (C% × TC)

NOPAT is the company's net operating profit after taxes

C% is the cost of capital

TC is total capital

In EVA model, both NOPAT and TC are adjusted for a number of items

Because of the adjustments made in calculating EVA, a different numerical result may be obtained, in general, than that resulting from the use of the simple computation of RI (economic profits)

Economic value added (EVA) measures valued added to shareholders by management

Some of the more common adjustments include the following

Research and development (R&D) expenses are capitalized and amortized rather than expensed

Deferred taxes are eliminated such that only cash taxes are treated as an expense

Any inventory LIFO reserve is added back to capital, and any increase in the LIFO reserve is added in when calculating NOPAT

Operating leases are treated as capital leases, and nonrecurring items are adjusted

Market Value Added

Market value added (MVA) = market value of the company - accounting book value of total capital

A company that generates positive economic profit should have a market value in excess of the accounting book value of its capital

Analysts should evaluate the change in MVA over time

MVA measures the effect on value of management's decisions since the firm's inception

Tobin's Q

Tobin's q = Market value of debt and equity / Replacement cost of total asssets

Denominator uses assets that are valued at replacement cost rather than at historical accounting cost

Replacement costs take into account the effects of inflation

Valuation Models

Single-Stage Residual Income Model

If we assume constant growth rate for residual income

V_0=B_0+\sum_{i=1}^{+\infty} \frac{R_i}{\left(1+r_e\right)^i}=B_0+\frac{R_1}{r_e-g}=B_0+\frac{B_0\times\left(R O E-r_e\right)}{r_e-g}=B_0\times \frac{R O E-g}{r_e-g}

\frac{RI_1}{r_e-g} is the additional value generated by the firm's ability to produce returns in excess of the cost of equity, and consequently, it is the present value of a firm's expected economic profits

In practice, if we use single-stage residual income valuation model,we always assume that a company has a constant return on equity and constant earnings growth rate through time

Multi-Stage Models-Using P/B Ratio

The main task here is to solve the PV of continuing residual income

V = B + PV(interim high-growthRI) + PV(continuing RI)

One finite-horizon model of residual income valuation assumes that at the end of time horizon T, a certain premium over book value P^\ast_T-B_T exists for the company

V_0=B_0+\sum_{t=1}^T \frac{N_t-r \times B_{t-1}}{(1+r)^t}+\frac{P_T^*-B_T}{(1+r)^T}

The essence here is that the Rl will decline to mature industry level

The longer the forecast period, the greater the chance the company's residual income will converge to zero, thus P^\ast_T-B_T may be treated as zero

Continuing Residual Income

Situation I: RI will drop immediately to zero after year T

PV_T=0

PV_0=0

Situation II: RI will persist at current level forever

PV_T=\frac{RI_{T+1}}{r_e}=\frac{RI_{T}}{r_e}

PV_0=\frac{PV_T}{(1+r_e)^T}

Situation III: RI will decline over time to zero after year T

PV_T=\frac{RI_{T+1}}{1+r_e-\omega} \omega is a persistence factor, which is between zero and one

PV_0=\frac{PV_T}{(1+r_e)^T}

Situation IV: RI will decline to mature industry level at the end of year T

PV_T=P_T^\ast-B_T=(P/B)_t\times B_T-B_T

PV_0=\frac{PV_T}{(1+r_e)^T}

Persistence Factor

Factors suggesting higher\omega

Low dividend payout

Strong market leadership positions

High historical persistence in the industry

Factors suggesting lower\omega

Extreme accounting rates of return(ROE)

Extreme levels of special items

Extreme levels of accounting accruals

Model Comparisons

DDM

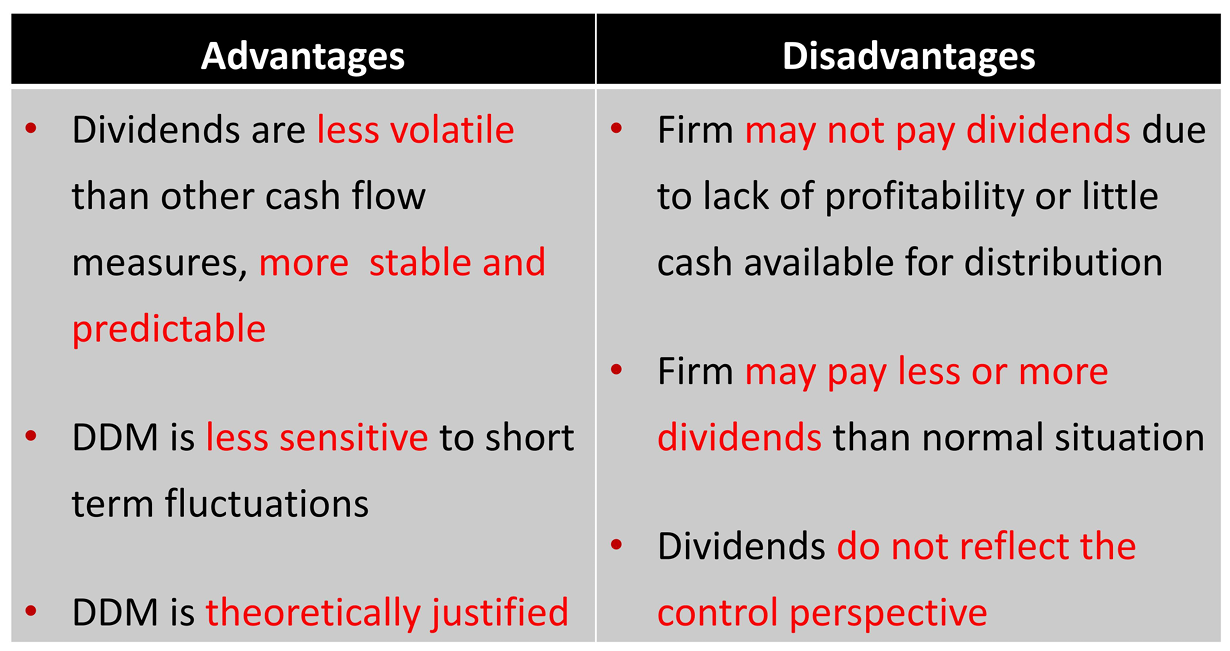

Advantages of DDM

Investors generally receives cash returns only in the form of dividends

The relative stability of dividends may make DDM values less sensitive to short-run fluctuations in underlying value than alternative DCF models

Analysts often view DDM values as reflecting long-run intrinsic value

Disadvantages of DDM

A company might not pay dividends on its stock

Predicting the timing of dividend initiation and the magnitude of future dividends without any prior dividend data is generally not practical

Dividends may not reflect the control perspective desired by the investor

Appropriateness for using DDM

The company is dividend-paying (i.e., the analyst has a dividend record to analyze)

The board of directors has established a dividend policy that bears an understandable and consistent relationship to the company's profitability

The investor takes an on-control perspective Mature firms, profitable but not fast growth

FCF Model

Advantages of FCF model

Popular in current investment practice

The record of free cash flows can also be examined even for a non-dividend-paying company

FCFE can be viewed as measuring a company's capacity to pay dividends

Disadvantages of FCF model

Negative free cash flow, resulting from large capital expenditure demands

May require long forecast periods for CF to turn positive, introducing greater model uncertainty

Appropriateness for using FCF model

No dividend payment history

Dividends not related to earnings or dividends and FCF differ significantly

FCF consistent with profitability within a reasonable time period

Controlling shareholder perspective

RI Model

Advantages of RI model

Wide applicability, even if FCF < 0

Used for dividend and non-dividend paying firms

Incorporates opportunity cost of capital for both debt and equity holders

Brings recognition value closer to the present by focusing on current book value plus forecasted residual income

Disadvantages of RI model

Application of the RI model requires a detailed knowledge of accrual accounting

The quality of accounting disclosure can make the use of Rl valuation less robust and more error prone

RI model is appropriate when

No dividends or volatile dividends

Negative free cash flows

Uncertainty in forecasting terminal values

RI model is not appropriate when

Clean surplus solution violated significantly

Unreliable estimates of BV and ROE

Private Company Valuation

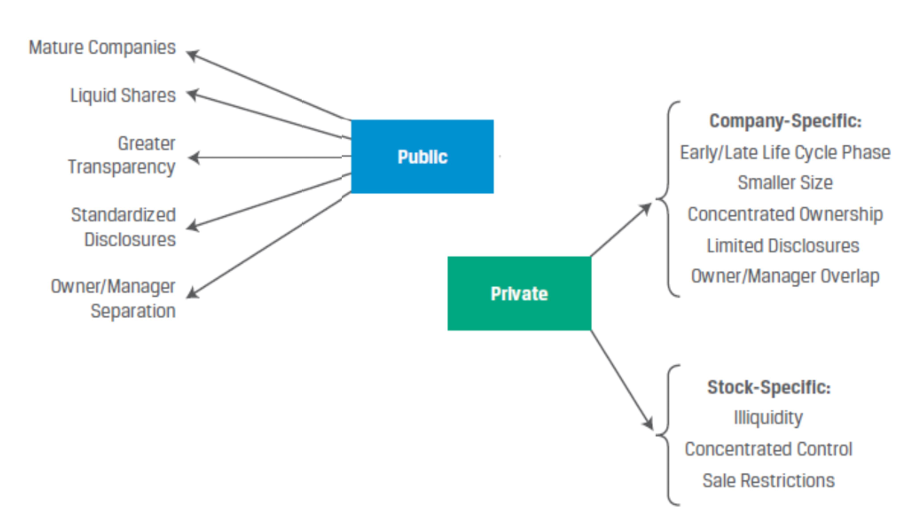

Public vs.Private Company Valuation

Public Versus Private Company Features

The valuation of smaller firms often warrants the use of a higher required rate of return due to greater income variability and risk resulting from:

fewer and less-diversified lines of business and customers;

less well developed marketing, sales, and distribution;

limited growth prospects because of reduced access to capital.

Company-specific factors may be positive or negative.

The senior management of many private firms often has a controlling ownership interest. This feature greatly reduces the principal-agent problem which may arise when owners and managers are separate.

Private equity firms often acquire underperforming public companies to restructure, divest, or acquire lines of business while under private ownership and control with the goal of selling the reorganized firm at a higher price to another private buyer or the public via an IPO

Private company managers can take a longer-term perspective in strategic decision making without pressure from external investors seeking short-term gains on publicly traded shares.

Family Ownership of Private Companies

Family owned and operated businesses dominate the private company landscape in many developed and developing economies.

The small and medium-sized enterprises in the German-speaking countries of Germany, Austria, and Switzerland known as the Mittelstand are predominantly family owned and managed.

Private company valuation often plays an important role as business owners consider turning over control to non-family managers while retaining ownership, accessing external capital, or selling a minority stake or the entire business.

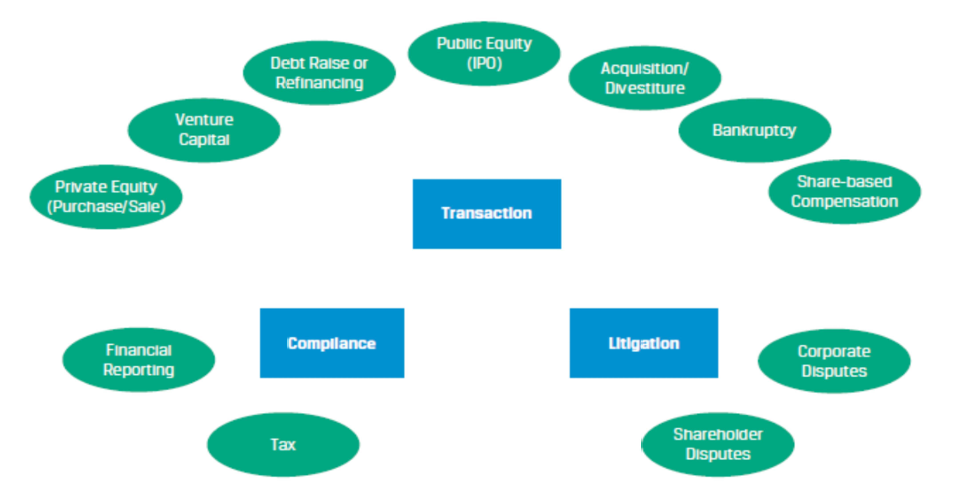

Private Company Valuation Uses and Areas of Focus

Transaction-related valuations(transfer of ownership or incremental financing)

Venture capital financing (early stage); Private equity financing (growth or buyout stage);Debt financing; Initial public offering (IPO); Acquisitions and divestitures; Bankruptcy; Share-based incentive compensation

Compliance-related valuations(compliance and litigation purposes)

Financial reporting; Tax reporting; Litigation

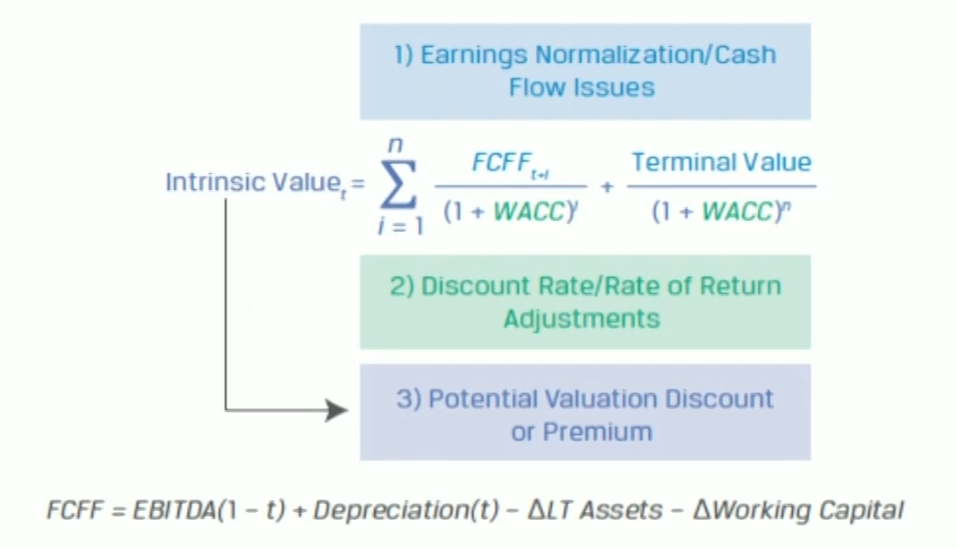

Three key areas related to private company valuation warrant the particular attention of analysts

Cash Flow and Earnings Adjustments: analysts must first identify and adjust key balance sheet and income statement items to address private versus public company differences to estimate a company's normalized earnings.

Discount Rate and Rate of Return Adjustments: due to the lack of observable market prices for debt and equity, the assumptions associated with the CAPM for public companies often do not apply to private companies and require estimation and adjustment

Valuation Discount or Premium: stock-specific considerations related to either the benefit of greater control or the drawback of illiquidity and a minority interest in a business with lesser control must be factored into a company's valuation.

Areas of Focus on Private Company Valuation

Earnings Normalization Issues for Private Companies

Private companies may have their financial statements reviewed rather than audited.

Reviewed financial statements involve an opinion letter with representations and limited assurances by the reviewing accountant and a less thorough review than for audited financials

Compiled financial statements are the most basic approach and are unaccompanied by an auditor's opinion letter.

Reviewed or compiled statements usually require adjustment.

Earnings Normalization and Cash Flow Estimation

Normalized earnings

Private company valuation: specific adjustments for non-recurring,non-economic items as well as for ongoing anomalies which prevent direct comparisons to publicly owned entities.

Related Party Transaction: A related party transaction is one between parties which share economic or other interests

An arm's length transaction is one between independent parties acting in their own self-interest which occur and are recorded at or near fair market value.

Cash Flow Estimation Issues for Private Companies

Specific challenges associated with private company cash flow valuation include the nature of the interest being valued,potentially acute uncertainties regarding future operations, and managerial involvement in forecasting.

A valuation based upon scenario analysis is a common approach.

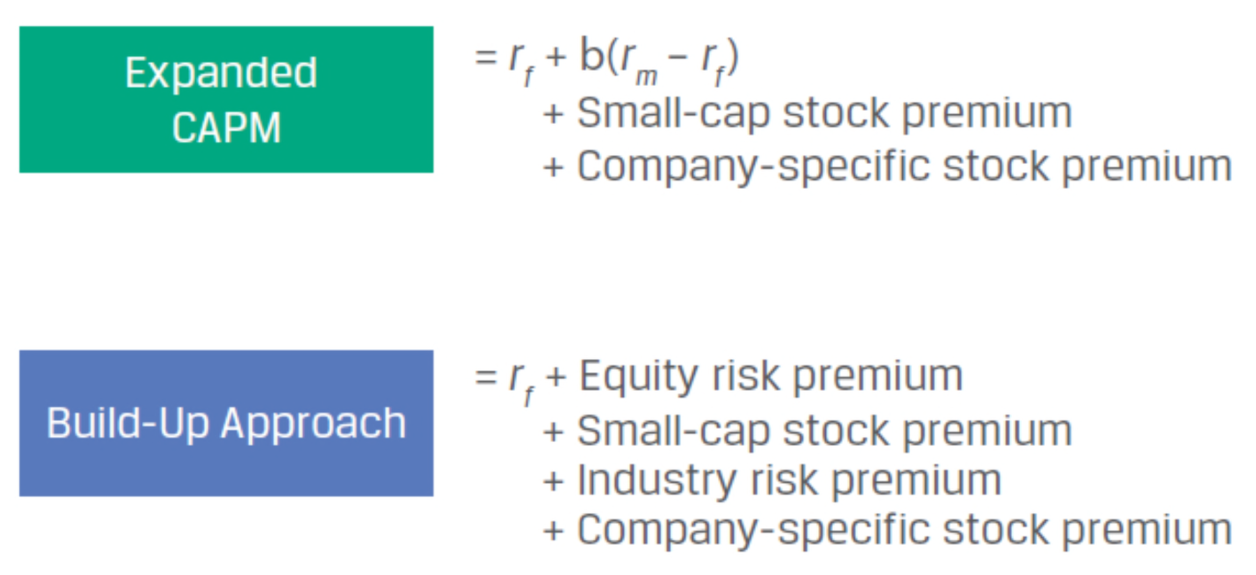

Factors Affecting Private Company Discount Rates

Application of size premiums to discount rates.

Relative debt availability and cost of debt.

Private company may have less access to debt financing than similar public company. Reduced debt access may lead a private company to rely more on equity financing,which would tend to increase its WACC

A smaller private company could face greater operating risk and a higher cost of debt

Discount rates in an acquisition context.

When larger, more mature companies acquire smaller, riskier target companies, the buyer would be expected to have a lower cost of capital than the target.

Discount rate adjustment for projection risk would typically be highly judgmental.

Required Rate of Return Models

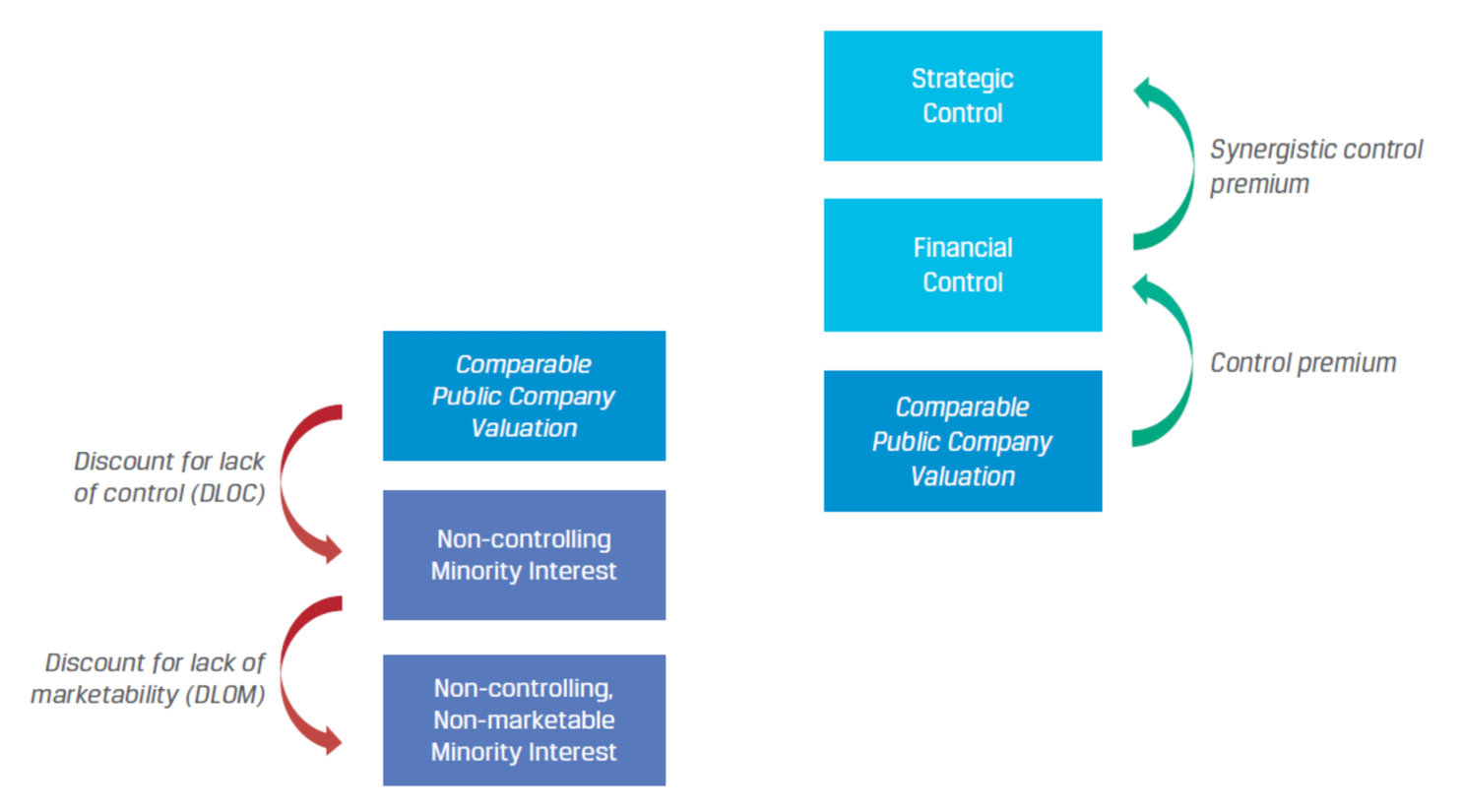

Valuation Discounts and Premiums

Strategic buyer: this value reflects a buyer who intends to use their controlling stake to take action to increase firm revenue and/or decrease costs beyond current expectations in order to increase the company's value.

Financial buyer: may be willing to pay a premium for a controlling interest for a private firm but is either unable to identify any synergies from a controlling interest, may be unable or unwilling to take advantage of them due to a lack of operational or management expertise, or has limited risk appetite.

Discount for lack of control (DLOC): involves a deduction from the pro rata share of 100% of the value of an equity interest to reflect the absence of some or all powers of control.

A lack of control may be disadvantageous to an investor because of the inability to select directors, officers, and management that control an entity's operations.

DLOC= 1- [1 / (1 + Control premium)]

Discount for lack of marketability (DLOM): is a deduction from an ownership interest's value to reflect the relative absence of a liquid market for a company's shares.

Develop marketability discount estimates. Restricted stock: The sale of blocks of restricted stock that exceed public trading activity in the stock.

The relationship of stock sales prior to IPOs: early-stage or high-growth companies approaching an IPO, an increase in value may result from lower risk and uncertainty as a company progresses in its development.

Option-based approaches: an at-the-money put option is priced; The put option premium as a percentage of the stock value provides an estimate of the DLOM.

Total Discount = [1 - (1 - DLOC) × (1 - DLOM)]

Private Company Valuation Approaches

Approaches for Private Company Valuation

The income approach values an asset as the present discounted value of the income expected from it

The market approach values an asset based on pricing multiples from sales of assets viewed as similar to the subject asset

The asset-based approach values a private company based on the values of the underlying assets of the entity less the value of any related liabilities

Income Approach

Free cash flow method

Capitalized cash flow method

CCM estimates value based on a company's projected performance as a growing perpetuity under the assumption of stable growth.

\text{Firm Value}_t=\frac{F C F F_{t+1}}{W A C C-g}

The expected FCFF may be estimated using the company's expected after-tax EBIT and the firm's reinvestment rate

\begin{align}

&\text { Firm Value }_t=\frac{\text { EBIT }_{t+1}(1-t)(1-\text { RIR })}{\text { WACC }-g}

\\

&\text { Revinvestment rate }=\mathrm{RIR}=\frac{g}{\mathrm{WACC}}

\end{align}

To solve for the intrinsic equity value, we must subtract the estimated market value of debt from firm value.

A constant WAcC---the capital structure will remain unchanged.

Estimate the market value of private debt when traded market values are unavailable.

Debt represents a small fraction --the face value of debt

Significant leverage, changing financial conditions, significant volatility--significant premium or discount from face value

FCFE excludes payments to debtholders and uses the cost of equity.

The denominator is referred to as the capitalization rate.

I V_t=\frac{\mathrm{FCFE}_{t+1}}{r_e-g}

Excess earnings method

Market-Based Approach

Guideline Public Company Method(GPCM)

The PE ratio are frequently cited in the valuation of public companies, while metrics such as EV are more common in private company valuation as they offer greater flexibility to accommodate changes to the capital structure over the valuation period.

It is important to consider not only firms from the same industry but also firms of similar size, leverage, and stage in the company life cycle when choosing comparable.

Control premiums may be used in valuing a controlling interest in a company.

Several factors require careful consideration in estimating a control premium.

Type of transaction: strategic buyer > financial transactions

Industry factors: different time reflect different environment

Form of consideration: the exchange of stock or cash

Advantage of GPCM: potentially large pool of guideline companies and significant financial and trading information available

Disadvantage of GPCM: issues regarding to comparability and subjectivity in the risk and growth adjustment

Guideline Transactions Method (GTM)

Guideline Transactions(GTM) uses pricing multiples derived from acquisitions of public or private companies.

Transaction multiples would be the most relevant evidence for valuation of a controlling interest in a private company.

Several factors must be considered in assessing transaction-based pricing multiples:

Synergies

Contingent consideration

Non-cash consideration

Availability of transactions

Changes between transaction date and valuation date

Prior Transaction Method(PTM)

The prior transaction method (PTM) uses the actual price paid for shares or the price multiples implied by past transactions in the stock of the subject private company as the guideline

PTM is most relevant when considering the value of a minority equity interest in a company

Disadvantage of PTM: Historical transactions in the subject stock are very limited

Asset-Based Approach

The value of equity is calculated as the fair value of total assets less the fair value of total liabilities

Appropriateness

Not used for going concerns

Usually the lowest valuation

Difficulties in valuation:

Individual assets, Specialized assets, Intangibles