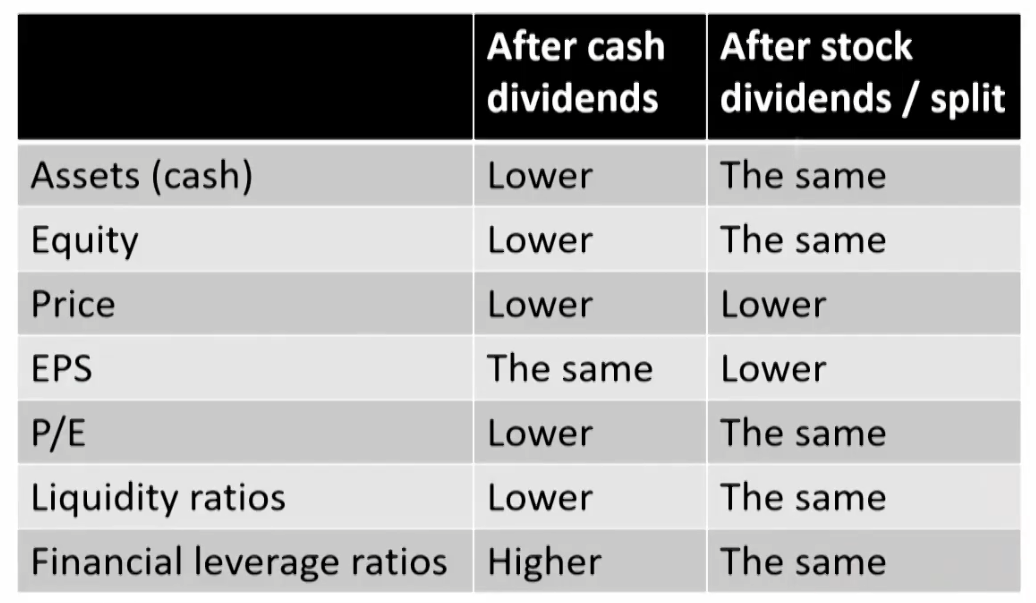

Cash dividends

Stock price will drop by the dividend amount, but the wealth of shareholders will not changes if there is no tax.

Stock dividends and stock split

Generally not taxable to shareholders.

The proportionate ownership and wealth of shareholders will not change.

Effects of dividends on financial ratio

Cash dividends Reduces both the asset and shareowners' equity. Liquidity ratio will decrease (current ratio, etc).

Financial leverage ratio will increase (D/E, D/A).

Stock dividends and stock split

No effect on total asset and total shareowners' equity, but number of shares will increase.

Both share price and EPS will decline.

Dividend Theories

Theories

Dividend policy does not matter(MM)

Dividend policy does matter

Bird-in-hand argument

Tax argument

Other theoretical issues

Information signaling

Agency costs

Information Signaling

Dividend increases or decreases may affect share price because they may convey new information about the company.

Dividend declaration resolves information asymmetry Initiations or increases convey positive information. Omissions or reductions convey negative information.

Companies that consistently increase their dividends seem to share certain characteristics: Dominant or niche positions in their industry Global operations

Relatively high returns on assets

Relatively low debt ratios

Agency Costs

Between shareholders and managers

Dividends payout reduces free cash flow for managers to overinvest and run out of control.

Between shareholders and bondholders

All else equal, both dividends and share repurchases increase the risk that the company will default on its debt

Dividends transfer wealth from bondholders to shareholders.

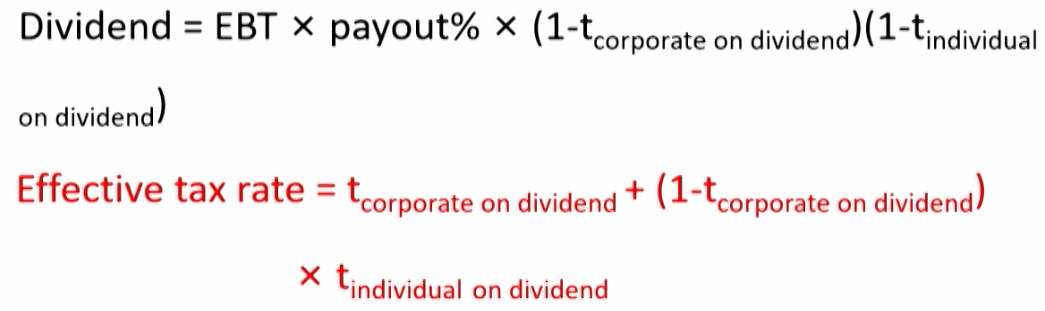

Tax Considerations

Double taxation system

Corporate pretax earnings are taxed at the corporate level and then taxed again at the shareholder level if they are distributed to taxable shareholders as dividends.

Dividend imputation tax system

Effectively ensures that corporate profits distributed as dividends are taxed just once,at the shareholder's tax rate.

Split-rate tax system

Corporate earnings that are distributed as dividends are taxed at a lower rate at the corporate level than earnings that are retained.

Dividends Payout Policies

Stable Dividend Policy

Most common used policy.

A process of gradual adjustment towards a target payout ratio based on long-term sustainable earnings.

Expected dividend = Previous dividend + (Expected earnings x Target payout ratio - Previous dividend) x Adjustment factor

Adjustment factor = 1/N (N is the number of years over which the adjustment in dividends should take place)

Constant Dividend Payout Ratio Policy

A dividend payout ratio decided on by the company is applied to current earnings to calculate the dividend.

Payout ratio = Dividends paid / Net income

Infrequently used, fluctuate with short-term earnings.

Share Repurchase and its Effects

Concept of share repurchase

Share repurchase: a transaction in which a company buys back its own shares.

Can be viewed as an alternative to cash dividends.

Treasury shares/stocks: shares that have been issued and subsequently repurchased.

Not considered for dividends, voting, or computing EPS.

Share repurchase methods

Buy in the open market

Flexibility in timing and amount.

Tender offer邀约收购,广而告之 Fixed price tender offer: buy a fixed number of shares at a fixed price, typically at a premium to market. Dutch auction: use auction to determine the lowest price.

Direct negotiation单独协商

Typically at a premium to market.

Effect on EPS

Repurchased with excess cash (financed internally) Asset (cash) and equity will decline

Financial leverage ratio (D/A, D/E) will increase. EPS will increase (only if the fund used to repurchase do not earn their cost of capital).

Repurchased with debt (financed externally) Debt increase and equity decline

Financial leverage ratio (D/A), will increase (even more than repurchase by excess cash).

If earning yield(E/P) > after-tax cost of debt, EPS will increase

If earning yield(E/P) < after-tax cost of debt, EPS will decrease

Effect on Book Value Per Share(BVPS)

BVPS = Book value of equity / shares outstanding

Share repurchase will result book value per share (BVPS): Decrease, if the repurchase price > the original BVPS. Remain the same, if the repurchase price = the original BVPS. Increase, if the repurchase price < the original BVPS.

Analysis of Dividend and Share Repurchase

Dividends vs. Share Repurchase on shareholders wealth

Assuming the tax treatment of these two methods is the same, a share repurchase has the same impact on shareholder wealth as a cash dividend payment of an equal amount.

If a company repurchases shares from an individual shareholder at a negotiated price representing a premium over the market price, the remaining shareholders' wealth is reduced

Dividend vs. Share Repurchase

Share repurchase wins in aspects of

Potential tax advantages

Share price support/signaling that the company considers its shares a good investment

Added managerial flexibility Offsetting dilution from employee stock options Increasing financial leverage Increasing EPS

A company can use both special cash dividends and share repurchases as a supplement to regular cash dividends.

These means of distributing cash are often used in years when there are large and extraordinary increases in cash flow that are not expected to continue in future years.

A share repurchase is effectively an alternative to paying a special cash dividend

Analysis of Dividend Safety

Dividend payout ratio = dividends / net income

Dividend coverage ratio = net income / dividends

FCFE coverage ratio = FCFE / (dividends + share repurchases)

Warning signals for dividend cut:

Negative external stock market indicators

Extremely high dividend yields

ESG Considerations in Investment Analysis

Global Variations in Ownership Structures

Ownership Structures

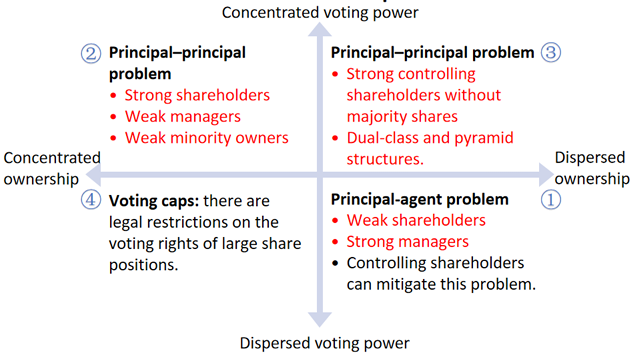

Dispersed vs. Concentrated Ownership

Dispersed ownership: none of shareholders have the ability to individually exercise control over the corporation.

Concentrated ownership: an individual shareholder or a group (called controlling shareholders) with the ability to exercise control over the corporation.

"Hybrid" corporate ownership

On a global basis, concentrated ownership structures are considerably more common than dispersed ownership structures.

Other Ownership Structures

Horizontal ownership: companies with mutual business interests (e.g., key customers or suppliers) that have cross-holding share arrangements with each other.

Vertical ownership(pyramid ownership): a company or group that has a controlling interest in two or more holding companies, which in turn have controlling interests in various operating companies.

Voting power

Dual-class shares: grant one share class superior or even sole voting rights, whereas the other share class has inferior or no voting rights.

Benefit: lower risks associated with principal-agent problems(concentrated ownership and management responsibility).

Drawbacks: poor transparency, lack of management accountability, modest consideration for minority shareholder rights, and difficulty in attracting quality talent for management positions.

State-owned enterprises (SOEs)

Institutional investors

Group companies

Private equity firms

Foreign investors

Managers and board directors (insiders)

Effects of Ownership Structure on Corporate Governance

Independent board directors(or independent board members 独立董事会)

No material relationship with the company with regard to employment, ownership, or remuneration.

United States requires audit, nomination, and compensation committees be composed entirely of independent directors.

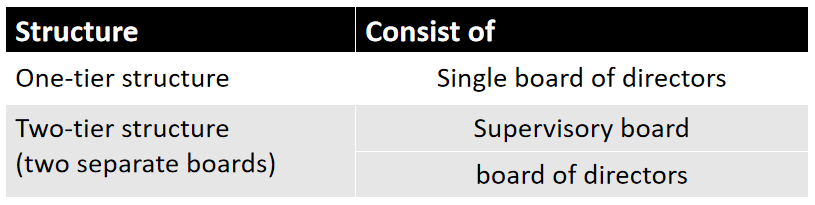

Board Structures

Special voting arrangements: improve the position of minority shareholders in board nomination and election processes.

Corporate governance codes, laws, and listing requirements

Stewardship codes投资人尽责条款: voluntary codes that encourage investors to exercise their legal rights and increase their level of engagement in corporate governance.

Corporate Governance Evaluation

Board Policies and Practices

Board of directors structure

CEO duality两职合一: CEO also serves as chairperson of the board.

Raise concerns that the monitoring and oversight role of the board may be compromised relative to independent chairperson and CEO roles.

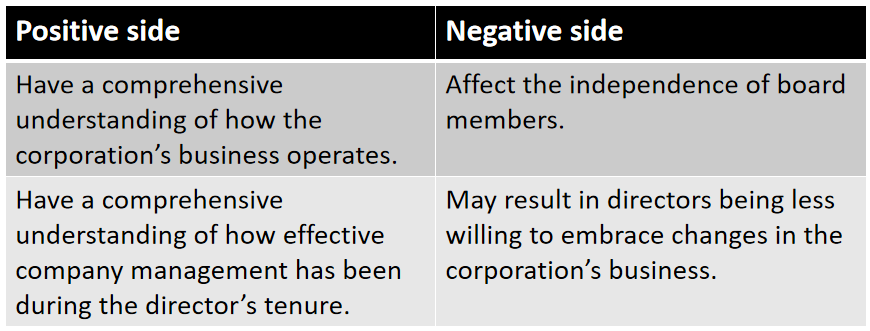

Board independence

A lack of independent directors on a board may increase investors' perception of the corporation's risk.

Board committees

Generally include audit, governance, remuneration (or compensation),nomination, and risk and compliance committees.

Assess whether there are sufficiently independent committees that focus on key governance concerns, such as audit, compensation, and the selection of directors.

Board skills and experience → board tenure

A board director's tenure is considered long if it exceeds 10years.

Board composition: reflects the number and diversity of directors.

Other considerations

Executive Remuneration

Involves such issues as transparency of compensation,performance criteria for incentive plans (both short term and long term), the linkage of remuneration with the company strategy, and the pay differential between the CEO and the average worker

"Say-on-pay" provision

Claw-back policy

"Excessive" remuneration → use KPI to analysis.

Shareholder Voting Rights

Straight voting share structure: one vote for each share owned.

Dual-class share structures: company founders and/or management typically have shares with more voting power than the class of shares available to the general public.

ESG-related Risks and Opportunities

Materiality and Investment Horizon

Materiality重要性 typically refers to ESG-related issues that are expected to affect a company's operations, its financial performance, and the valuation of its securities.

Positive ESG information ≠ material ESG information

Negative ESG information ≠ immaterial ESG information

Investment horizon

Short-term investment horizon considers short-term ESG issues, and vice versa.

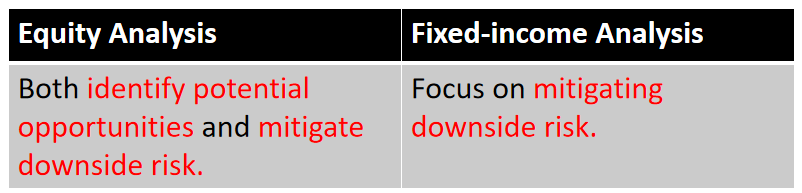

Equity vs. Fixed-Income Security Analysis

ESG integration: the implementation of qualitative and quantitative ESG factors in traditional security and industry analysis.

Green Bonds

The bonds in which the proceeds are designated by issuers to fund a specific project or portfolio of projects that have environmental or climate benefits.

Green bonds are typically the same credit ratings and valuation to an issuer's conventional bonds, with the exception that the bond proceeds are earmarked for green projects.

Some green bonds may command a premium, or tighter credit spread, versus comparable conventional bonds because of market demand.

Greenwashing risk: the risk that the bond's proceeds are not actually used for a beneficial environmental or climate-related project.

Liquidity risk: when the investors are often purchased by buy-and-hold purpose.

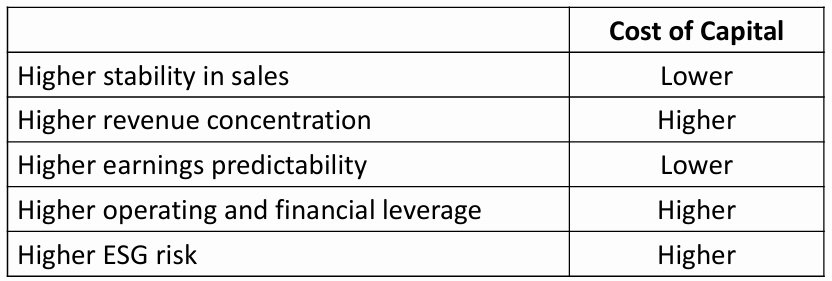

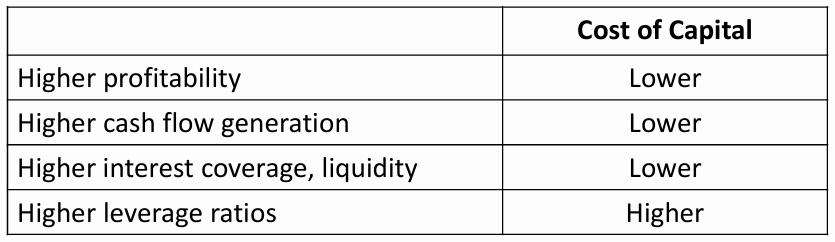

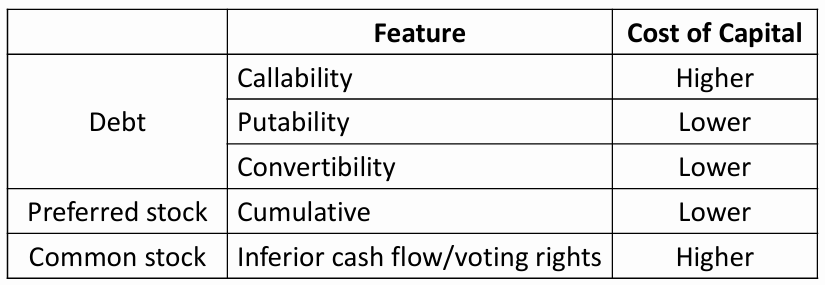

Cost of Capital: Advanced Topics

Cost of Capital

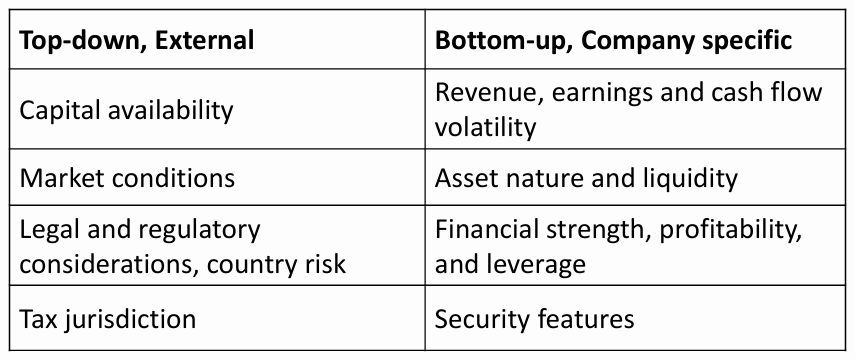

Cost of capital factors

Top-down external factors

Capital availability

Market conditions

Legal and regulatory considerations, country risk

Tax jurisdiction

Bottom-up company specific factors

Revenue, earnings, and cash flow volatility

Asset nature and liquidity

Financial strength

Securities features

Cost of Debt

Cost of debt estimation

Traded debt: YTM

Non-traded debt

With credit rating: similar bond yield or similar maturities

Without credit rating: synthetic credit ratings

Bank Loans

The interest rate on recently new bank loan could be a good estimate, if market conditions and the company's risk profile has not materially changed.

Generally, amortizing loans typically have a lower cost of debt than non-amortizing loans.

Leases

Rate implicit in the lease (RIIL):

Incremental borrowing rate (IBR):

The rate of a collateralized loan over the same term

If IBR is unknown, the non-traded debt estimation method might be used.

Country risk rating(CRR)

Economic conditions

Political risk

Exchange rate risk

Securities market development and regulation

Equity risk premium

Estimating the ERP

Historical approach

Forward-looking approach

Survey-based estimates

Dividend discount models

Macroeconomic modeling

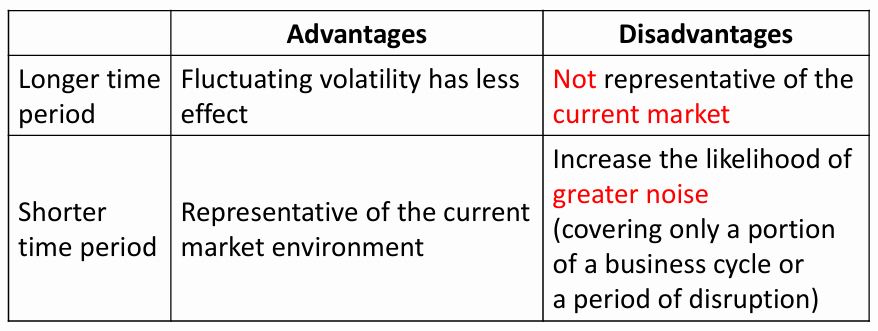

Historical Approach

Key assumption

Returns are stationary, and markets are relatively efficient, so over the long term, average returns should be an unbiased estimate of expected returns.

Key decisions

Selection of the equity index

Typically: broad-based, market-value-weighted indexes

Selection of the time period

Selection of the mean type

Selection of the risk-free rate proxy

Limitations of the historical approach

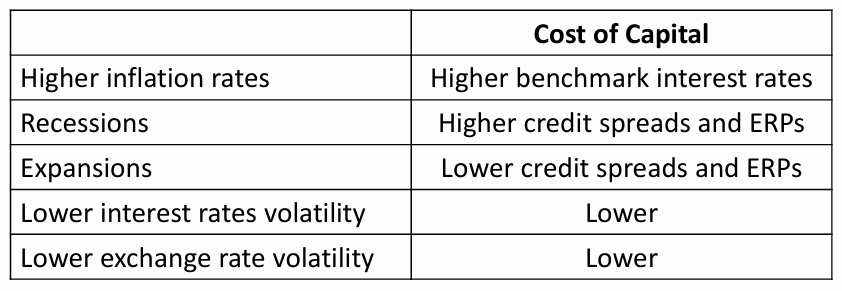

ERPs can vary over time.

Survivorship bias tends to inflate高估 historical estimates of the ERP

Forward-Looking Approach

The ERP depends strictly on future expectations, given that an investor's returns depend only on the investment's expected future cash flows.

Survey-based estimates

Dividend discount models

Macroeconomic modeling

Survey-based estimates

Assess expectations by asking people what they expect

Estimates tend to be sensitive to recent market returns

Dividend discount models (DDM)

Gordon growth model

ERP=E\left(\frac{D_1}{V_0}\right)+E\left(g\right)-r_f

Assumption: constant P/E.Earnings, dividends, and prices will grow at the same rate.

ERP estimates rely on forecasted economic variables.

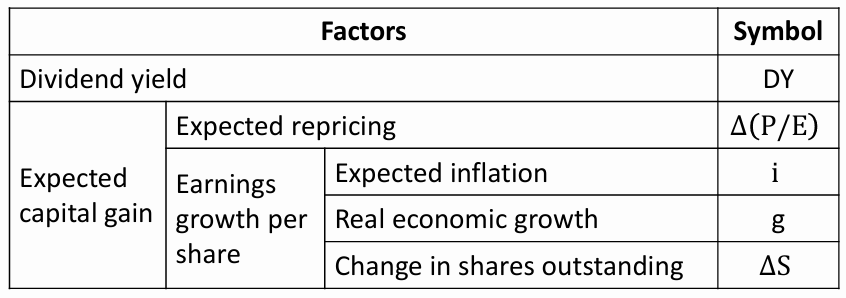

Grinold-Kroner model

ERP=\left[DY+\Delta\left(\frac{P}{E}\right)+i+g-\Delta S\right]-r_f

Expected inflation

Expected inflation can be estimated as the yield on a US Treasury bond and a similar maturity Treasury Inflation-Protected Security (TIPS):

YTM_{\text{Treasury bond}}-YTM_{\text{TIPS}}

More reliable when public equities represent a relatively large share of the economy, as in many developed markets.

Limitations of the forward-lookjng approach

Surveys

Sampling and response biases

Behavioral biases(eg. recency bias,confirmation bias)

DDM

Assumptions of constant P/E is unreasonable.

Macroeconomic models

Modeling errors

Behavioral biases in forecasting

Cost of Equity

Cost of Equity for Public Companies

Models

DDMs

Bond yield plus risk premium approach(BYPRP)

Risk-based models

Capital assets pricing model (CAPM)

Fama-French models

DDMs

Requirements:

Publicly traded shares, stable and predictable dividend.

Gordon growth model:

\mathrm{r}_{\mathrm{e}}=\frac{\mathrm{D}_1}{\mathrm{p}_0}+\mathrm{g}

BYPRP is another means of estimating the required return on equity for a company that has public debt.

r_e=r_d+RP

r_d: proxied by YTM on the company's long-term debt RP: can be estimated using historical mean difference in returns between an equity market index and a corporate bond index

Advantages

Estimating cost of debt provides a starting point estimate of the return demanded by debt investors.

Disadvantages

Determination of RP is relatively arbitrary.

Requires company to have traded debt.

If a company has multiple traded debts with different features, there is no prescription of which to select.

Risk-based models

Capital assets pricing model (CAPM)

r_e=r_f+\widehat{\beta} \mathrm{ERP}

\widehat{\beta}: Regressing the company's returns on the market index returns with their actual historic data

Fama-French Models

r_e=r_f+\beta_1\mathrm{ERP}+\beta_2\mathrm{SMB}+\beta_3\mathrm{HML}+\beta_4\mathrm{RMW}+\beta_5\mathrm{CMA}

SMB: small minus big, size premium

HML: high(book-to-market) minus low, value premium

RMW: robust minus weak, profitability premium

CMA: conservative minus aggressive, investment premium

Cost of Equity for Private Companies

Expanded CAPM

Adds a premium for small company size and other company-specific risks.

r_e=r_f+\beta_{\text {peer }}( ERP )+ SP + SCRP

\beta_{\text {peer }}: an industry beta, from a peer group of publicly traded companies in the same industry

SP: size premium

SCRP: specific-company risk premium

Build-up approach

Implied beta is 1.0

r_e=r_f+ ERP +IP+ SP + SCRP

r_f+ ERP: average risk large-cap public equity

IP: industry risk premium

SP: size premium

SCRP: specific-company risk premium

Country spread models

Country risk premium (CRP) is required by investors for the added risk of investing in emerging markets (local country).

\begin{align}

&ERP_{\text{emerging market}}=ERP_{\text{developed market}}+\lambda\times CRP

\\

&CRP=\text{Sovereign yield spread}\times\frac{\sigma_{Equity}}{\sigma_{Bond}}

\end{align}

CRP: country risk premium

\lambda: the level of exposure of the company to the local country

\text{Sovereign yield spread}: The yield on emerging market bonds minus the yield on developed market government bonds.

\sigma_{Equity}: volatility of the local country's equity market

\sigma_{Bond}: volatility of the local country's bond market

Global CAPM(GCAPM)

Single factor: a global market index

Assuming no significant risk differences across countries International CAPM(ICAPM)

International CAPM(ICAPM)

E\left(r_e\right)=r_f+\beta_G\left(E\left(r_{g m}\right)-r_f\right)+\beta_C\left(E\left(r_c\right)-r_f\right)

r_{g m}: global index

r_{c}: foreign currency index

Capital Restructuring

Corporate Actions and Motivations

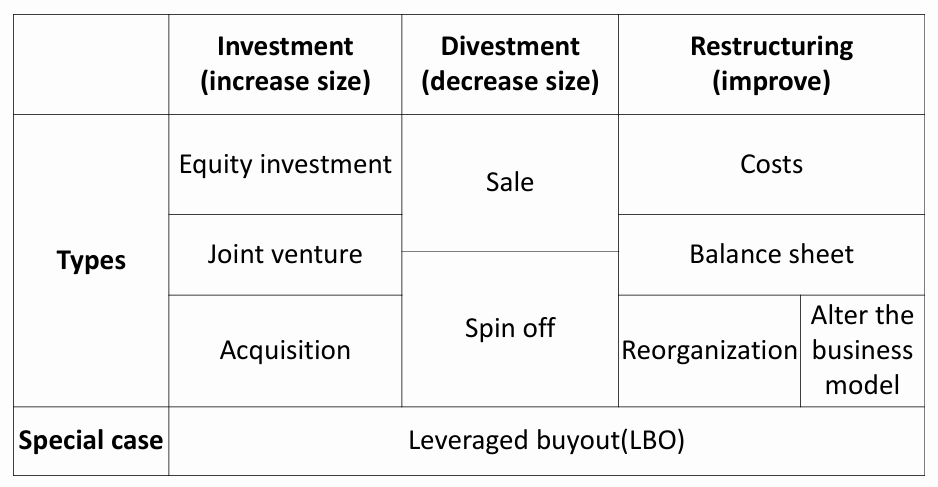

Types of corporate structural changes

Investment

Increase the size or scope of a company, thereby increasing the revenue and perhaps revenue growth.

Divestment

Reduce the size or scope of a company, through disposing of slower-growing, lower-profitability, or higher-risk operations to improve the overall financial performance.

Restructuring

Improve the cost and financing structure to increase growth,improve profitability, or reduce risks without altering the size or scope of a company.

Divestment action motivations

Focus operations and business lines

Valuation(Conglomerate discount多元化折价)

Liquidity needs

Regulatory requirements

Restructuring action motivations

Improve returns on capital(Opportunistic improvement主动, Forced improvement被迫)

Financial challenges, including bankruptcy and liquidation

Top-down

High asset prices

Greater CEO confidence

Lower cost of financing(Lower interest rates, Higher equity prices)

Overvalued stock prices

Industry shocks

Regulatory changes, technological changes, or changes in the growth rate of the industry

Types of corporate restructuring

Types of investment actions

Equity investment

Joint venture

Acquisition

Types of divestment actions

Sales/Divestiture

The seller sells a company, segment of a company, or group of assets to an acquirer.

Capital to be reallocated to a better use

The seller and acquirer both focus on their strengths.

Spin off分拆

A company separates a distinct part of its business into a new, independent company.

Remove incompatibilities, and to increase management and employee focus by

Separating distinct businesses

Awarding employees with stock-based compensation

Types of restructuring actions

Forced improvement

Cost restructuring成本重组: Reduce costs by improving operational efficiency and profitability.

Outsourcing外包 and offshoring离岸外包

Balance sheet restructuring: Shift the asset composition,change the capital structure, or both.

Sale leaseback售后回租

Dividend recapitalization借债回购股票

Reorganization重整: a court-supervised restructuring process

Opportunistic improvement

Alter the business model Franchising特许经营: An owner can divest its asset and license the intellectual property to a third-party operator

Cost restructuring

Balance sheet restructuring

Sale leaseback

Motivations

Unlock the value in the real estate assets which are a non-core business for a company with attractive valuations.

Improve a company's balance sheet by retiring debt and improving its credit rating.

Valuation

Cap rate: net operating income divided by property's value

Cap rate may be influenced by location and physical condition of the property.

Special case: leveraged buyout

An acquirer uses a significant amount of debt to finance the acquisition of a target and then pursues restructuring actions,with the goal of exiting the target with a sale or public listing.

A series of actions that include investment, divestment, and restructuring.

Evaluating Corporate Restructurings

Initial Evaluation

What and Why

Is it material: It is material if total transaction value of an acquisition exceeds 10% of the acquirer's enterprise value prior to the transaction.

When: There is a substantial time delay.

Preliminary Valuation

Definition: use relative valuation methods to judge whether management uses stakeholder resources optimally to meet investors' required rate of return on capital.

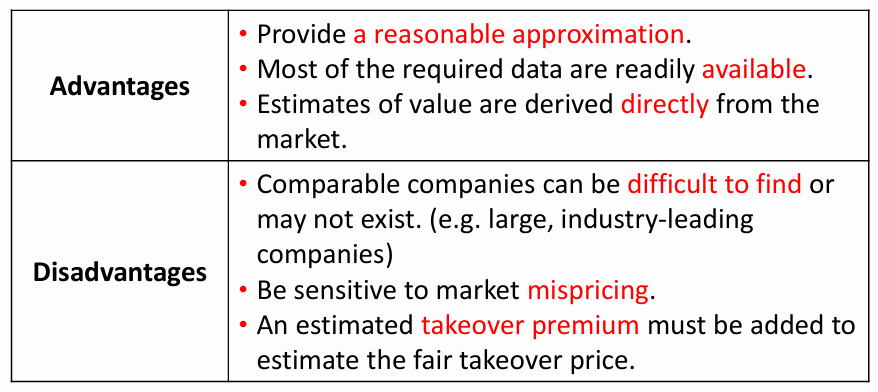

Comparable company analysis

Use the valuation multiples of similar listed companies to value a target company.

Enterprise multiples(e.g. EV/EBITDA or EV/sales) are less sensitive to differences in capital structure.

Earning multiplies: Price/Earnings,Price/sales

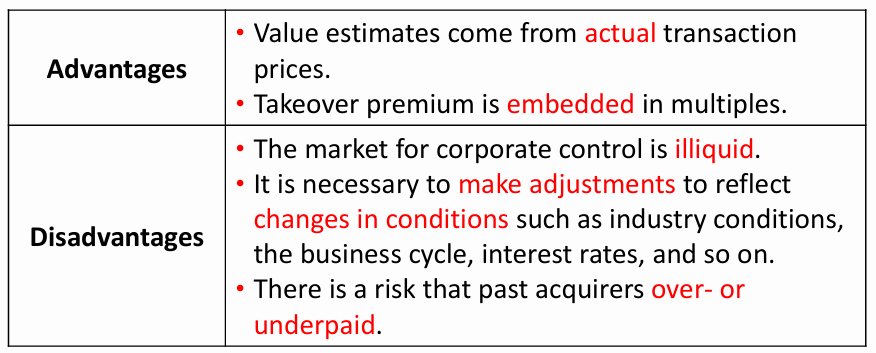

Comparable transaction analysis

Uses valuation multiples from historical acquisitions of similar companies to evaluate a target's value.

Valuation multiples include takeover premiums.

Premium paid analysis

Takeover premium收购溢价: The amount by which the per-share takeover price exceeds the unaffected price expressed as a percentage of the unaffected price.

PRM=\frac{DP-SP}{SP}

PRM: Takeover premium (as a percentage)

DP: Deal price per share

SP: Unaffected stock price per share

Modelling and Valuation

Issuer's motivations analysis

Pro forma WACC modeling

Capital structure

Issue new debt or equity

Repurchase stock or repay debt

Cost of capital: When issuing debt during restructuring, firms will try to keep its bond above investment grade.